Will February 23rd Mark the Day Europe Becomes Investable?

Author: Chris Wood

All the evidence is that Donald Trump is much more prepared for his second term in the White House than was the case following his 2016 victory, which, by all accounts, he did not expect to win.

This means it has been no surprise that the US stock market rallied into year-end on the anticipation of pro-growth policies, most particularly tax cuts extended and deregulation.

The risk to equities, beyond sky high valuations, remains rising bond yields.

The 10-year Treasury bond yield is now 97bp higher than when the Federal Reserve commenced easing in September.

This is not what the central bank would have expected.

Some of Trump’s stated policies, be they tariffs, reshoring of production, or a clampdown on illegal immigration, are all fundamentally inflationary, though Elon Musk’s stated willingness to cut US$2tn from the federal budget would clearly be the opposite.

Trump May Negotiate A Deal With China

Meanwhile, Trump’s decision not to include Mike Pompeo or Nikki Haley in his new administration is a positive from a Beijing perspective.

Pompeo, as Secretary of State from April 2018 to January 2021, was the chief China hawk in Trump’s last administration and was primarily responsible for the major escalation as regards Taiwan in the final months of the Trump presidency.

This is why this writer continues to believe that the return of the Donald to the White House offers an opportunity at least for Beijing to negotiate a new deal with Washington, which would probably include China indicating a willingness to move some production to America.

And Move Quickly to End Russia-Ukraine War

Meanwhile, there remains the potential for Trump to move quickly on the Ukraine issue.

His comments in recent months that Ukrainian President Volodymyr Zelenskyy was the world’s “greatest salesman” shows his focus is primarily on the US$183bn of funding that Washington has so far extended or committed to Ukraine.

Beyond the issue of what has actually happened to all that money, scepticism is warranted that the Eurozone will keep funding Ukraine in the way currently being discussed if American financial support is cut off.

As far as this writer is concerned, a deal could have been done at any time in the past two years and ten months on a simple commitment that Ukraine will not join NATO, though clearly Russia will now want to negotiate on the basis of the territory it now occupies.

Any expectation of a deal on Ukraine will certainly help the risk-on move, in terms of lower oil prices, unless escalation resumes in the Middle East.

On that issue, Trump’s approach seems less clear-cut than on Ukraine.

Political Change in Germany Would Open up the Potential for Stock Outperformance in Europe

Meanwhile, Trump’s re-election coincided almost to the day with the unravelling of the German government as the FDP, in the form of former Finance Minister Christian Lindner, decided to cut and run from the three-party coalition by proposing corporate tax cuts to be funded by reductions in social spending and green subsidies.

The next federal election will be held on 23 February 2025.

This opens up the possibility, at least, of a new pro-cyclical trade in the Eurozone if CDU leader Friedrich Merz really decides to implement economic policies fundamentally different from the current coalition government, which this writer views as the most disastrous in terms of economic policy not only in the Eurozone but also in the developed world.

That would involve a conscious move away from Angela Merkel’s penchant for tracking towards the middle ground and back in the direction of policies advocated by the rising AfD.

Not to do so would mean creating a bigger political vacuum for the AfD to move into.

The “far-right” party is currently polling at an average 19% compared with the CDU’s 32% and the SPD’s 15%.

The stance of Germany’s political establishment towards the AfD has thus far been to have nothing to do with them, as they have been labelled as Nazis.

But with the AfD now the political party commanding the second largest support nationally, it is becoming ever riskier to maintain the stance that all the party’s supporters are Nazis, just as Kamala Harris’s effort to label Trump as the reincarnation of Adolf Hitler backfired badly given that 75m Americans voted for him.

Returning to the CDU, the policy which would most excite the German stock market and give a boost to the highly cyclical Eurozone equities asset class in general would be a formal commitment to abolish, or at least revise dramatically, German’s self-imposed fiscal constraint known as the “debt brake”.

The rule, first introduced in 2009 by the CDU under Merkel, limited the federal government’s structural budget deficits to 0.35% of GDP from 2016 and prohibited German states from taking on debt after 2020.

It was then suspended for four years between 2020 and 2023 as a result of the pandemic and the energy crisis following Russia’s invasion of Ukraine and reimposed last year.

A formal commitment to abolish the “debt brake” could potentially open the way for a surge in fiscal spending not focused on transfer payments and yet more welfarism but rather on a long overdue upgrade of German’s physical infrastructure and a related focus on the country’s shocking lack of digital infrastructure.

But clearly Merz would have to try to ensure that the extra spending did not just go on more benefits.

That is easier said than done.

There is certainly room for fiscal maneuvering, given German’s gross government debt to GDP ratio is “only” 62.4%.

Germany's Auto Sector is in Crisis

The existential crisis facing Germany’s auto sector is another reason urgent government action is needed.

Indeed it is not an exaggeration to say that Germany is facing the spectre of deindustrialization at a time when it seems singularly ill-prepared for the digital era.

The potential social fallout from deindustrialization is massive, as symbolised by Volkswagen’s recent decision to close at least three factories in Germany for the first time ever in the company’s 87-year history, according to the head of Volkswagen’s Works Council; though the automaker reportedly reached a deal with the trade union on 20 December to avoid plant closures.

In this respect, the number of jobs in Europe’s automotive sector is estimated to be 14m (directly and indirectly), with about 2.6m of them in Germany.

The European auto industry produced a record 14.9m passenger cars in 2017 compared with current production of only 12.2m.

Clearly, this is a dire situation not just for the carmakers but also for the industry’s network of suppliers.

The fundamental problem is that the German auto sector’s expertise, is in engineering and EVs are essentially computers on wheels.

So, investors should be thinking about what to buy in Europe the event of such a change in German policy, which is likely to be in the context of not only aggressive fiscal easing but also continuing monetary easing in the Eurozone where macro conditions in Germany argue for more aggressive rate cuts than in the case in America where the main argument for cutting rates further, albeit one still unacknowledged by the Fed, is to cut the federal government’s cost of debt servicing.

European Stocks Remain at a Massive Discount to the US

The ECB has so far cut rates by 100bp to 3.0% while the Fed has cut by 100bp to 4.25-4.5%.

Money markets are now discounting only 39bp of Fed rate cuts this year and 97bp of ECB rate cuts.

The other point about European equities is that they are trading at a massive discount to their US counterparts.

The MSCI Europe traded at the end of 2024 on 13.2x 12-month forward earnings, or a 40% discount to the MSCI USA 12-month forward PE of 21.9x.

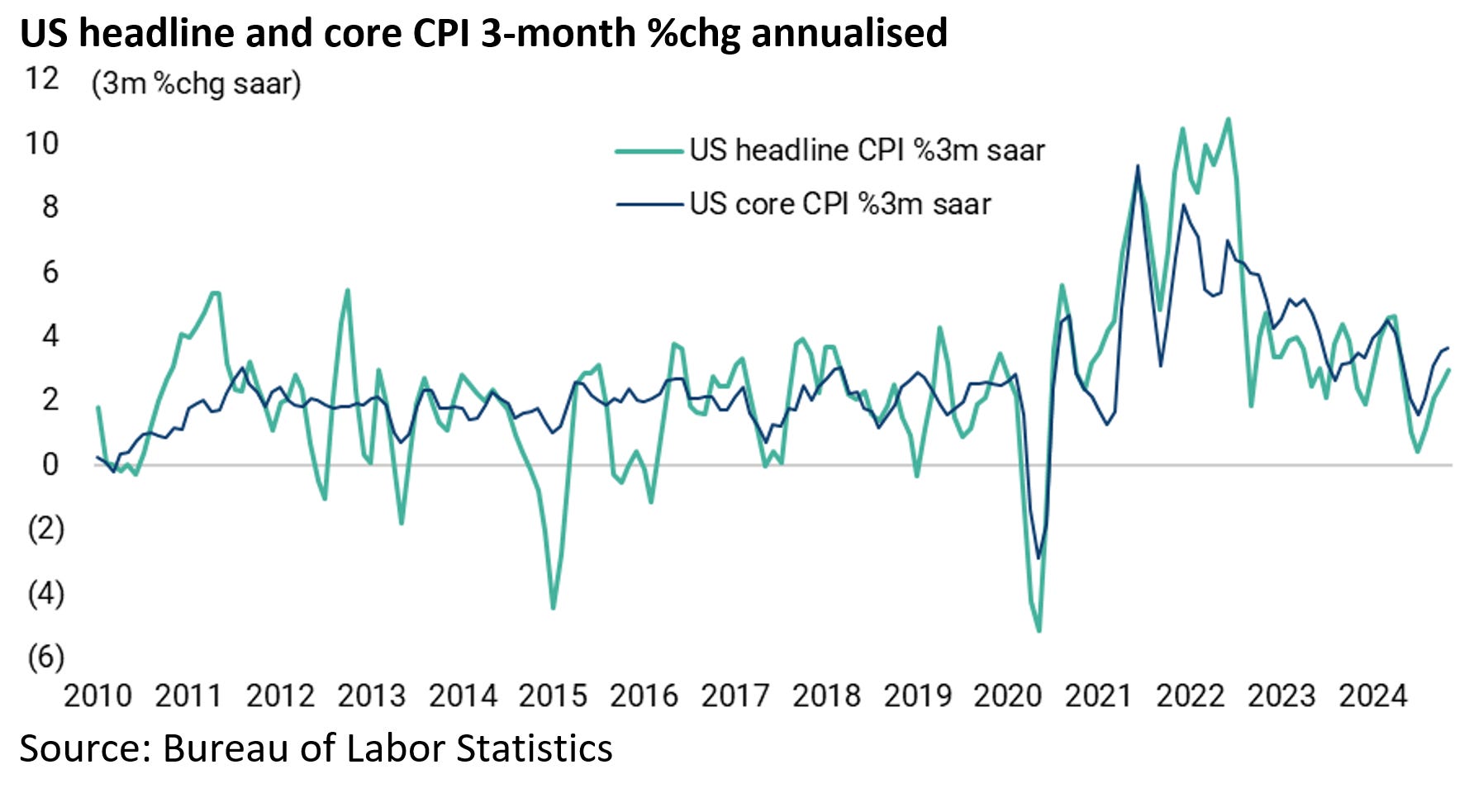

Beware the Return of Inflation

Meanwhile the latest US inflation data has served as a reminder that it is far from certain that inflation will keep falling.

Both US headline and core CPI rose by 0.3% MoM in November, up from -0.1% and 0.1% MoM respectively in June.

As a result, the three-month annualised rates of headline and core CPI have risen from 0.4% and 1.6%, respectively, in July to 3.0% and 3.7% in November.

On a year-on-year basis, headline CPI inflation rose from 2.4% YoY in September to 2.7% YoY in November, while core CPI inflation rose from 3.2% YoY in August to 3.3% YoY in November.