Why The Failure of DOGE is Our Base Case

Author: Chris Wood

One issue facing investors this year is the self-evident contradictory nature of President Donald Trump’s policy agenda and how those contradictions are resolved.

Still investors were not letting such issues bother them too much in the weeks following the presidential election.

The US stock market ended 2024 in a bullish frenzy.

The focus was on the deregulation drive likely to be initiated by the re-elected President Donald Trump as well as the anticipated extension of the Trump tax cuts of 2017.

There was also continuing focus on the predicted surge in productivity driven by the AI story, the thematic which continued to drive the “Big Tech” stocks with the biggest bulls even hailing America as a “start-up” economy.

Amidst much continuing talk of “American exceptionalism”, the American stock market on 24 December reached an all-time high as a percentage of the MSCI All Country World Index, accounting for 67.25% of that index.

It is now 66.2%.

While on a price to sales basis, a measure which takes out the distortions created by aggressive non-GAAP adjusted accounting, the S&P500 also traded at a record high.

The S&P500 price to sales ratio rose to a new record high of 3.28x on 23 January and is now 3.23x.

Trump's Policies are Inflationary and Negative for Growth

Returning to the issue of the Trump policy agenda, it is clearly the case that parts of that stated agenda, be it the threatened imposition of tariffs or cracking down on immigration, are negative from a growth standpoint and also fundamentally inflationary, a point the Fed will doubtless be aware of.

In this respect, there is a contradiction between the hopes for a disinflationary productivity-driven boom driven by the AI and deregulation themes, which the US stock market has been celebrating since the presidential election, and the threat of tariffs and curbs on immigration.

As regards the latter, even if mass deportations do not happen as has to be the base case, a significant decline in new arrivals will have a stagflationary impact.

There is also the related element of Trump’s essential unpredictability, in terms of policy being announced by tweet or his own social media platform Truth Social which, at a minimum, can cause short-term whipsaws in markets.

It is also the case that decisions can be swiftly reversed, most particularly if they are used as leverage in negotiation tactics, as was the case with the recent temporary imposition of 25% tariffs against both Canada and Mexico.

Can DOGE Reverse the Bear Market in Bonds?

Meanwhile, it is worth reiterating again that there has been one notable development since the presidential election in November which would cause a re-assessment of the long prevailing narrative argued here.

That is that Treasury bonds have entered a structural bear market since March 2020, a view which has so far been correct given that the 10-year Treasury bond has declined in value in three out of the past four years.

That development is the announcement that Elon Musk is the head a new government agency called the Department of Government Efficiency (DOGE) with the task of cutting US$2tn from the federal government budget by 4 July 2026.

It should be noted again that US$2tn represents 29% of total federal government spending in the 12 months to December.

This agenda was set out in an op-ed in the Wall Street Journal late last year (see Wall Street Journal article: “Elon Musk and Vivek Ramaswamy: The DOGE Plan to Reform Government”, 20 November 2024).

Clearly, if Elon Musk really cuts US$2tn from the federal budget that will reduce funding pressures considerably.

The initial market impact would likely be a big rally in Treasury bonds and a rally in the US dollar.

But there also would be a severe deflationary shock for the real economy which in the first instance would surely be negative for equities.

That negative impact would likely cause Trump to question such policies since the track record from his first administration is that he tends to view the stock market as the best indicator of whether his policies are working or not.

For such reasons the base case for now is that Musk will not succeed in such an ambitious undertaking, a view currently shared by most investors based on recent conversations.

Still the progress made by DOGE will need to be monitored carefully given the dramatic consequences of a successful execution of such a policy.

There is also no doubt that America’s fiscal predicament fully warrants such radical action which is why Musk has signed up “to drain the swamp”, to use a phrase made famous by the 47th president.

America's Worsening Fiscal Predicament

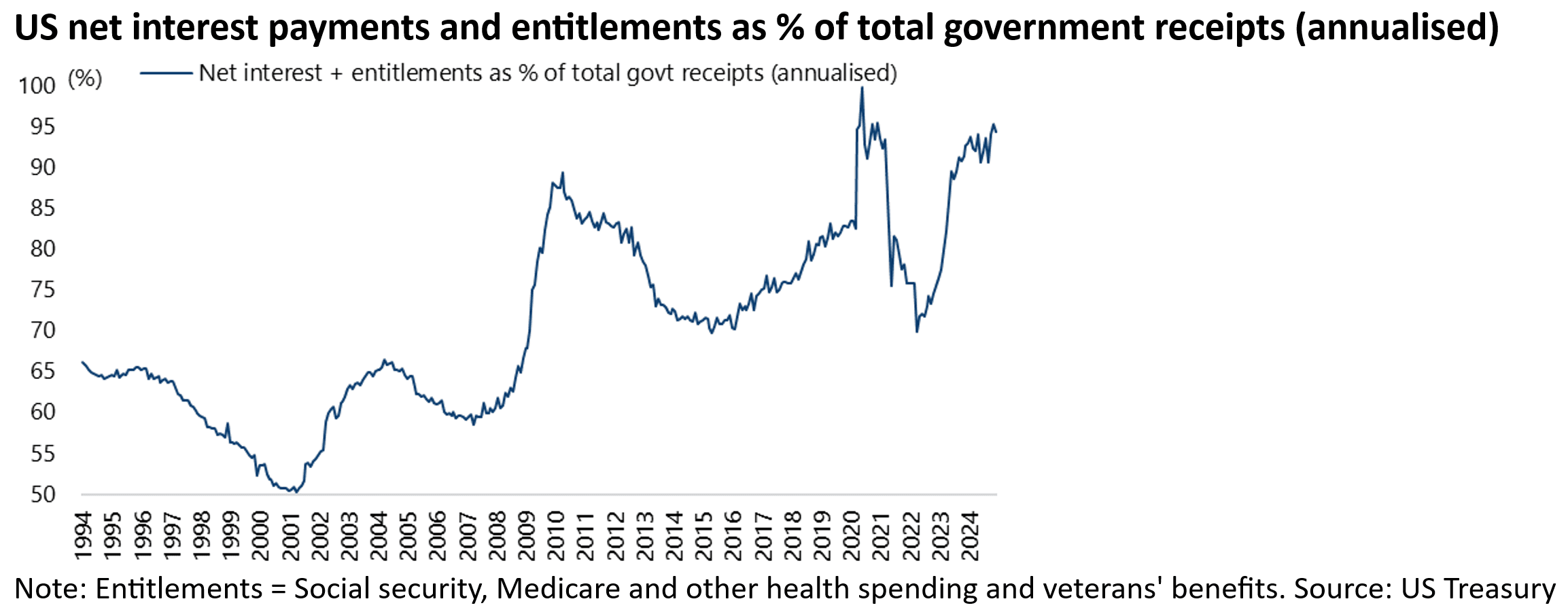

As for those fiscal stresses, they remain best captured by the following statistic.

Net interest payments and entitlements accounted for 94% of total government receipts in the 12 months to December.

This is at a time when the growth in tax revenue remains relatively healthy, rising by 9.6% YoY in 2024, reflecting a growing economy.

Such data means that in any downturn the fiscal situation would soon become unviable based on the Washington conventional wisdom, not necessarily shared by Musk, that the major entitlements programs such as Medicare and Social Security cannot be cut.

At that point the pressure will come on the Fed to resume purchases of Treasury bonds.

Meanwhile, as regards the issue of the duration of government debt, 53% of Treasury debt outstanding matures before the end of 2027 exposing the Treasury market to ongoing refinancing risk.

Private Construction Spending is Surging

All of the above suggests a difficult balancing act for the new Treasury Secretary Scott Bessent and others dealing with the economy under Trump given that, as already noted, part of the stated policy agenda is inflationary.

Still the base case remains that the tariff threat is primarily a negotiating tactic and that the best way for China to counter it is to offer to set up production in America, thereby presenting Trump with a “win”.

This is because for Trump the threat of tariffs seems primarily to be a means to an end.

And the end goal is that production should be moved to America for those who want access to the American domestic market.

On that latter point, construction of factories is already up almost threefold in America since the start of 2022 prior to the enactment of both the Inflation Reduction Act and the CHIPS and Science Act in August 2022, both of which created big financial incentives to move production to the US.

Private construction spending for manufacturing facilities has surged from US$7.6bn in January 2022 to US$20.3bn in December 2024, with construction spending for computer, electronic and electrical manufacturing up more than fivefold from US$2.1bn to US$10.9bn over the same period.

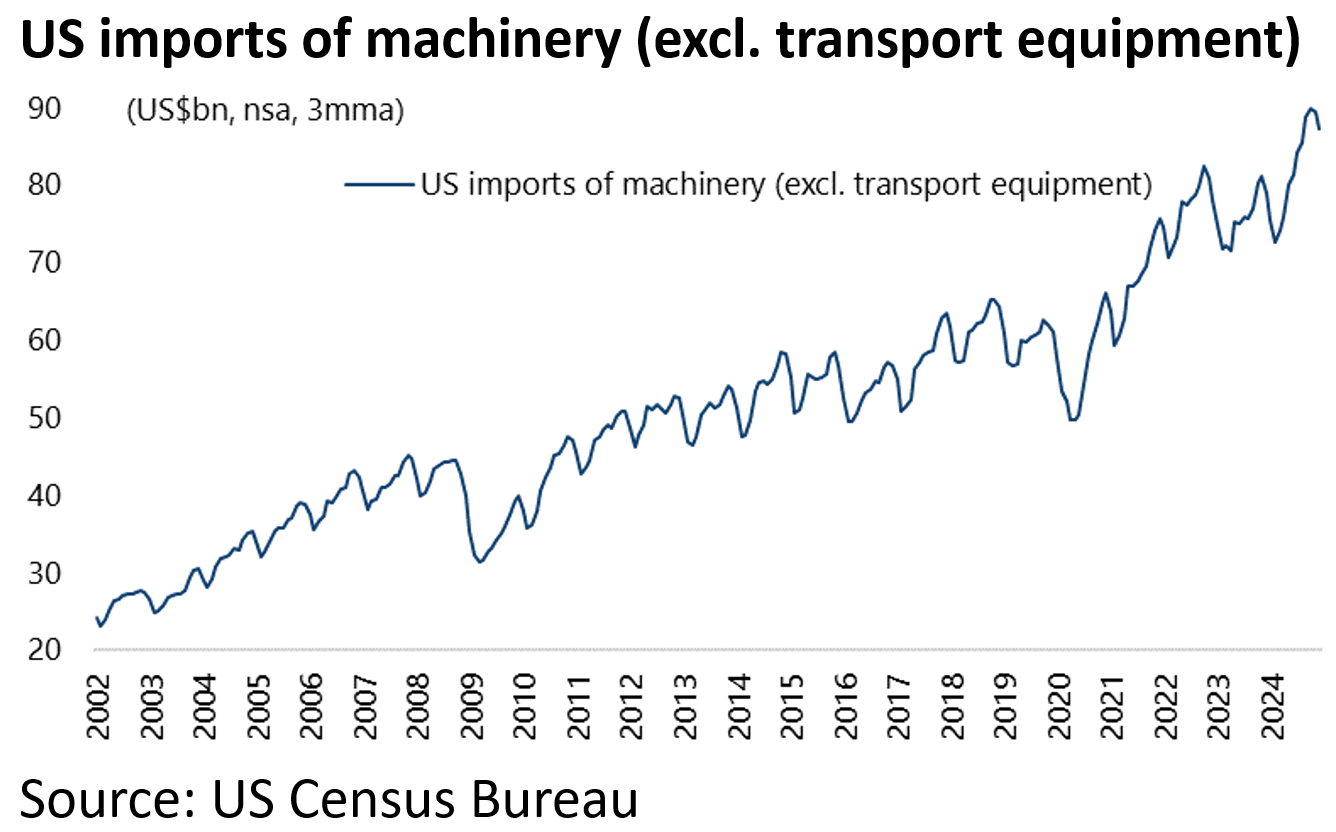

But there has yet to be a corresponding pickup in the import of industrial machinery.

US imports of machinery, excluding transport equipment, have risen by only 20% from US$71bn in January 2022 to US$85bn in December 2024.