Why The AI Picks-and-Shovels Boom May Be Peaking

Author: Chris Wood

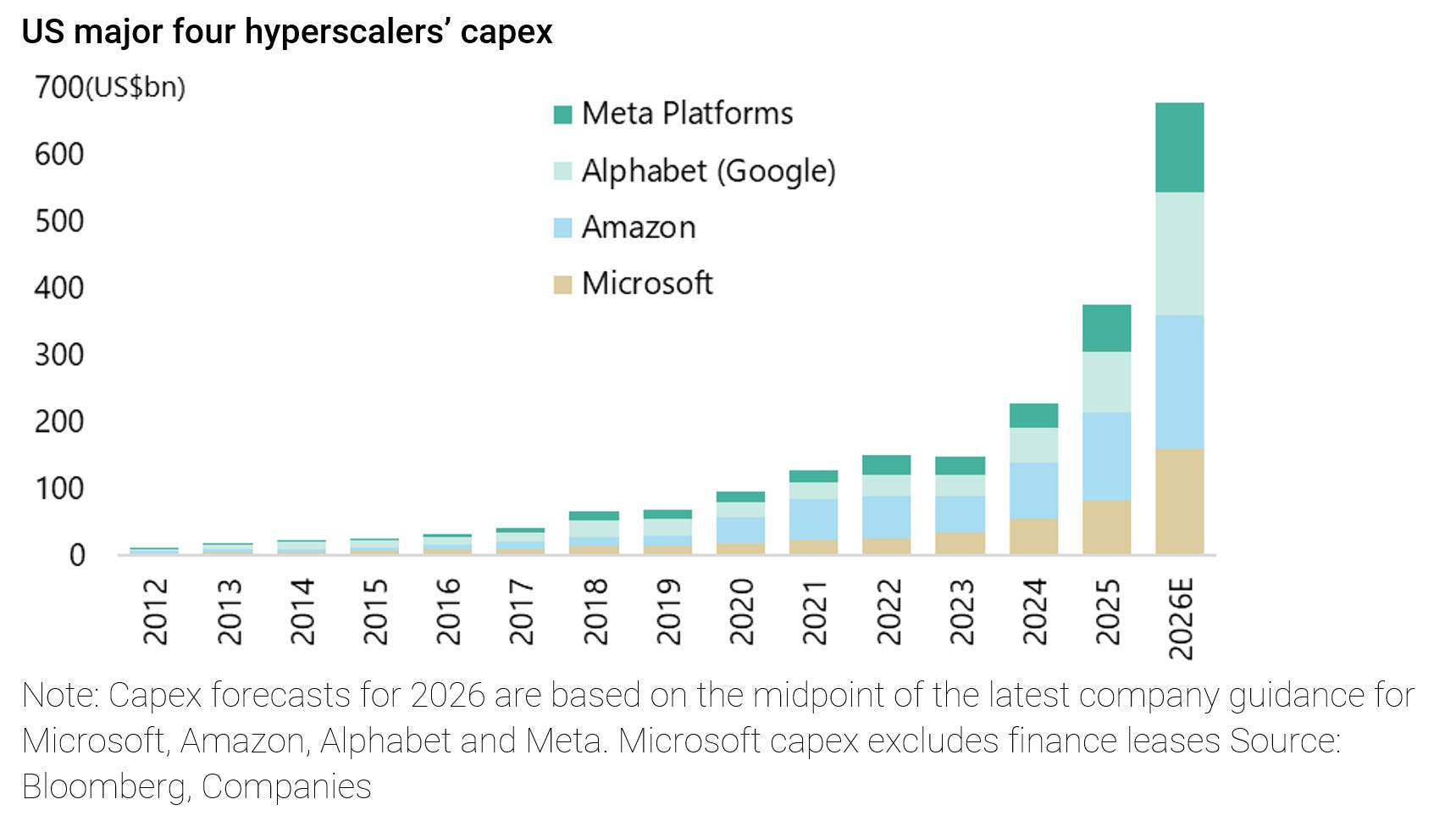

The key medium-term issue for the US stock market at the start of 2026 remains whether the hyperscalers will be able to monetise their AI capex, which this year is now forecast to reach a staggering US$680bn for the major four US hyperscalers following the latest earnings guidance.

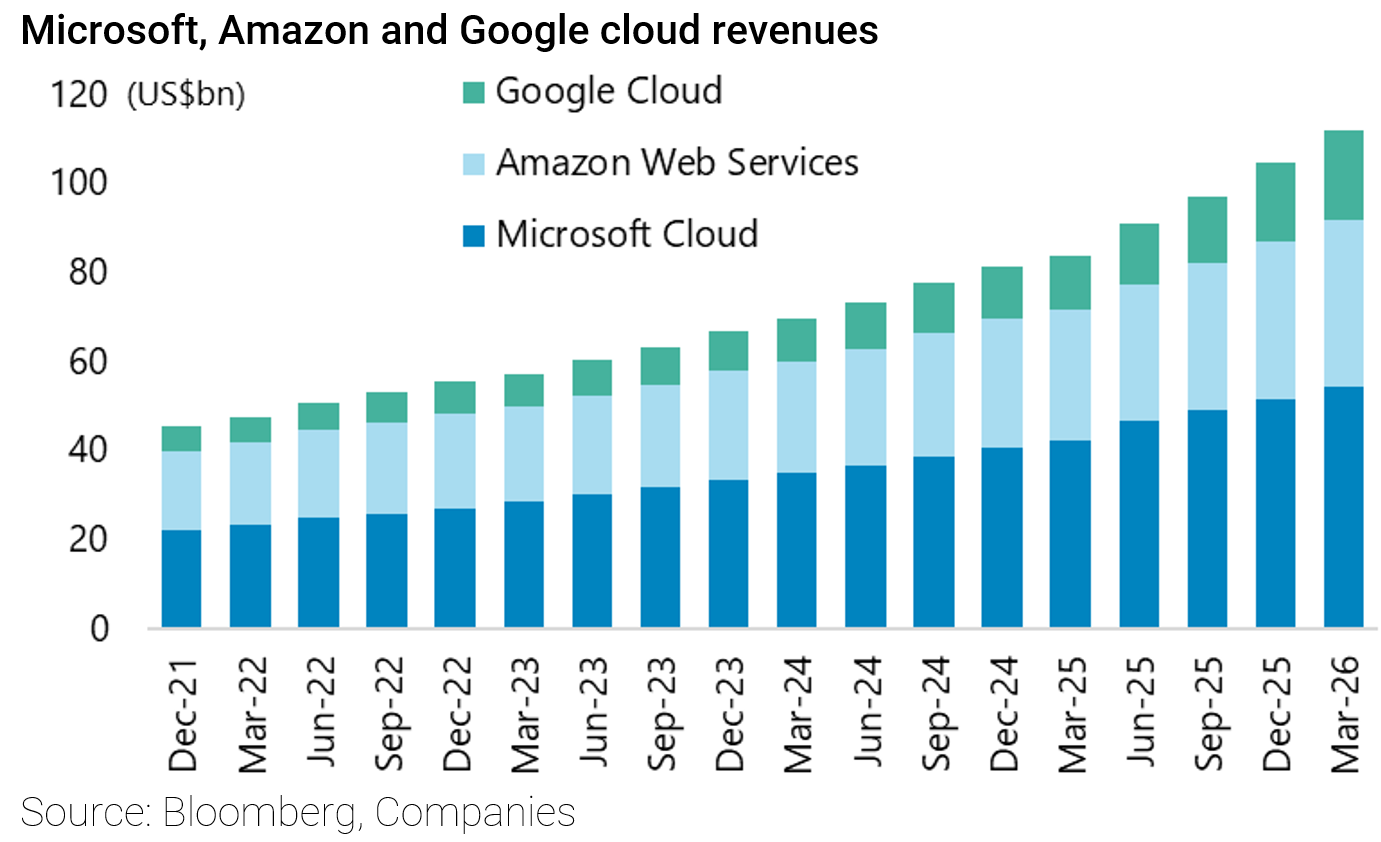

The market has viewed the increased capex for Alphabet, Microsoft and Amazon as positive because it has seen growing revenues in their cloud businesses.

Google Cloud’s revenues rose by 63% YoY last quarter, while Amazon Web Services (AWS) and Microsoft Cloud increased revenues by 28% and 29% YoY respectively.

Still there is an element of circularity here since cloud is benefitting from the pickup in demand from the likes of OpenAI and Anthropic.

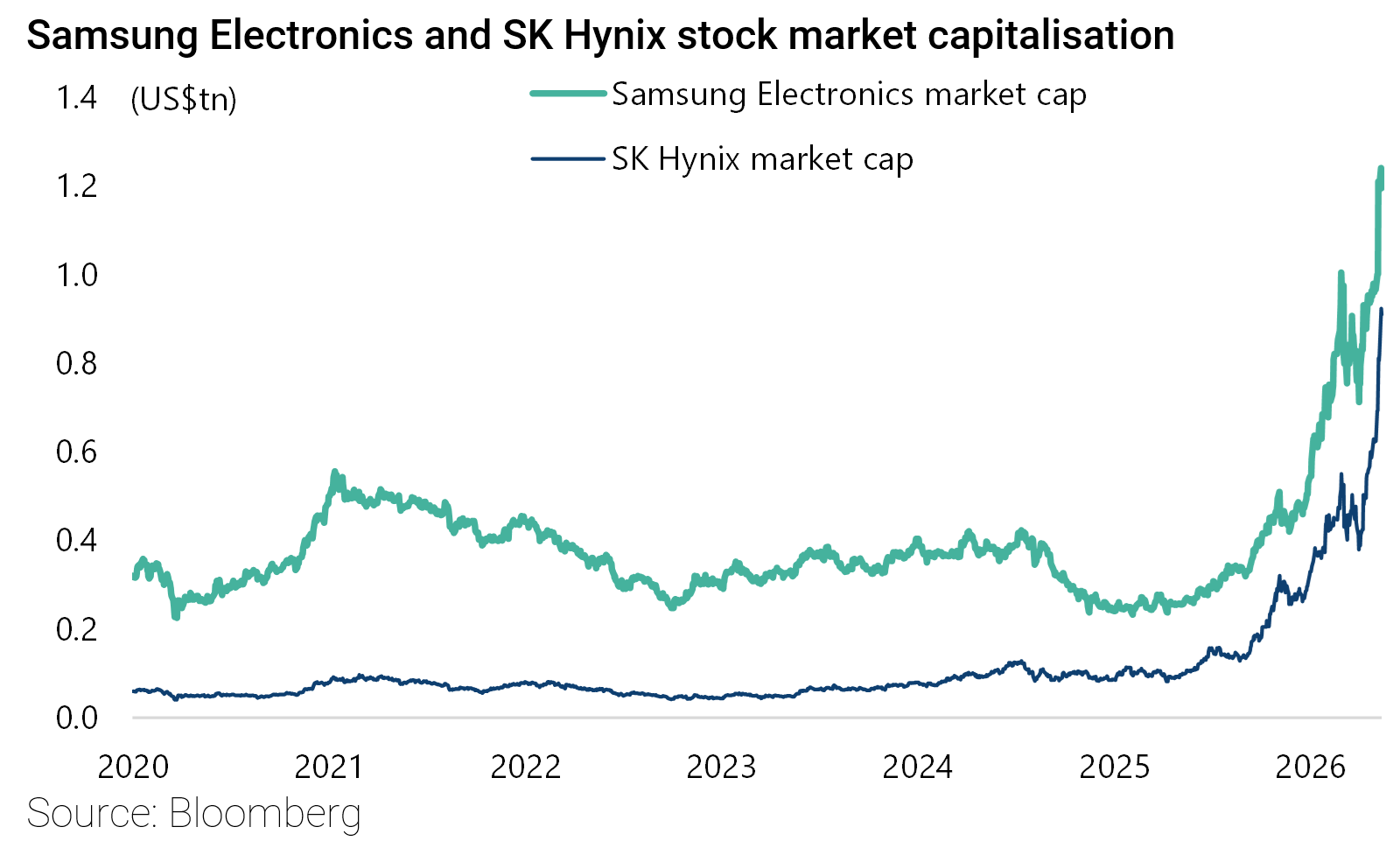

The real winner from the AI capex thematic in stock market terms remains the picks-and-shovels trade with the huge gains in the three global suppliers of DRAMs, two of which are quoted in the Korean market.

This has been the main driver of very positive earnings revisions in both the US and Asian equity universes.

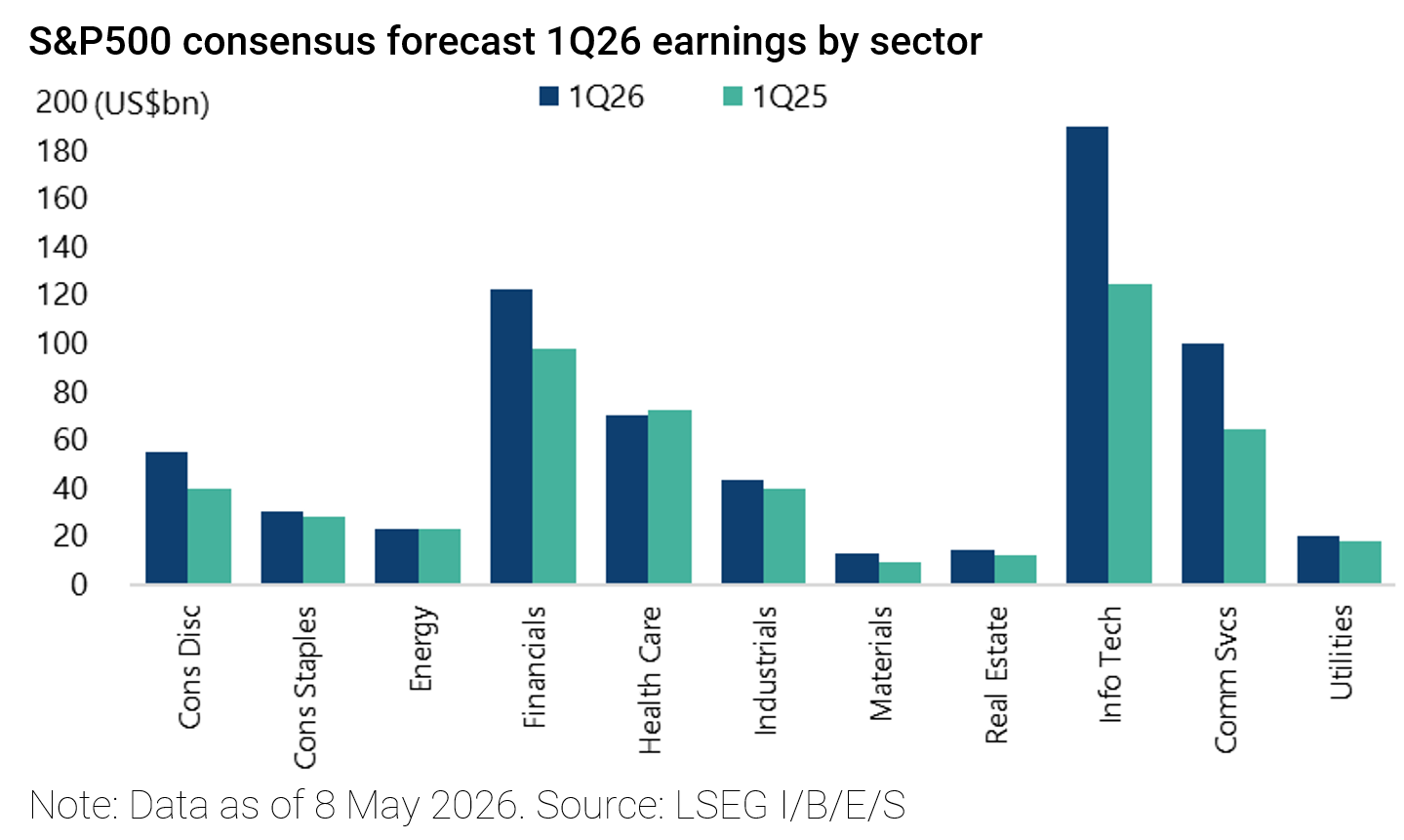

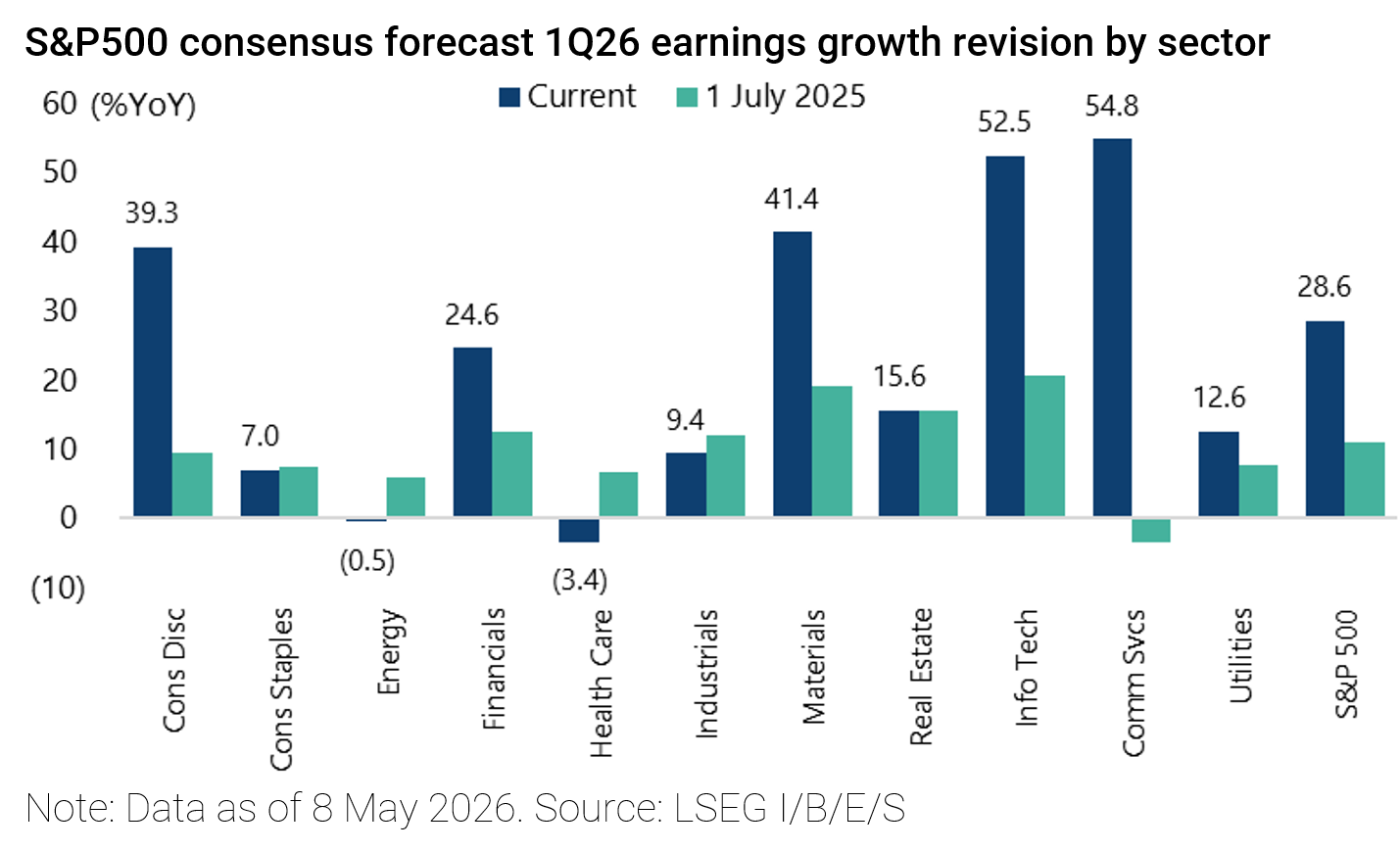

The LSEG I/B/E/S consensus data as of 8 May shows that S&P500 1Q26 earnings are expected to rise by 28.6% YoY, up from 10.9% growth expected last July.

The IT sector now has the second-highest forecast 1Q26 earnings growth of 52.5%, up from 20.7% last July.

Thus, the IT sector is expected to earn US$190.1bn in 1Q26, up from US$124.6bn in 1Q25, with all 12 sub-industries in the sector having higher earnings than a year ago.

Earnings for the IT sector account for 27.9% of the I/B/E/S forecast 1Q26 earnings for the S&P500, up from 23.5% in 1Q25. Unsurprisingly, the semiconductors and electronic components sub-industries have the highest earning growth (110.2% and 54.7%, respectively).

If these two sub-industries are excluded, the forecast growth rate for the IT sector declines to 27.1%.

Meanwhile, the Communication Services sector, which includes Alphabet and Meta, has the highest forecast 1Q26 earnings growth rate of 54.8%.

As for Asian equities, consensus 2026 earnings growth for the MSCI Asia Pacific ex-Japan universe is now 37%, but “only” 13% if Korea and Taiwan are excluded.

Consensus 2026 forecast EPS for the MSCI Asia ex-Japan universe has been revised up by 17% over the past three months, with the IT sector earnings being revised up by a massive 54%.

The result has been a dramatic rise in the stock market capitalisation of the likes of Samsung and Hynix.

Their profits this year are now forecast, for example, to be more than three times the total forecast profits of the benchmark Nifty 50 Index in India.

Samsung and Hynix are forecast by consensus to earn profits totalling W452tn (US$307bn) this year, compared with the total forecast profits of US$102bn for India’s Nifty 50 universe.

Still, it should be noted that the DRAM makers book their revenues up front, highlighting the front-end loading of profits.

By contrast, the hyperscalers are delaying the payment of the AI capex via extended depreciation schedules.

Still, the deprecation bill is rising…

Below we look at the extent to which the US and global economies are being propped up by AI CAPEX. Also do Hyperscalers have the financial capacity and do investors have the appetite to fund continued record levels of AI CAPEX spending?

Keep reading with a 7-day free trial

Subscribe to Grizzle Research & Quant to keep reading this post and get 7 days of free access to the full post archives.