Why India Will Be The Best Emerging Market Over the Next 10 Years

India has everything going for it...

Author: Chris Wood

With everybody focused on the US presidential election, this is a good time to look again at India which this writer continues to view as the best long-term opportunity for growth orientated equity investors globally, both on a five-year view and a ten-year view, as previously discussed here (see The Best Global Equity Story is India, 4 October 2022).

While valuations remain a near term issue in the small-cap and mid-cap space, the remarkable resilience of the stock market in the context of the hikes in the capital gains tax in July is proof of the extent to which Indian households now believe in the long-term equity story also.

In this respect, India remains in the early days of building an equity culture in the sense that households still have only 5.8% of their assets in equities, compared with 13.3% in bank deposits and these bank deposits are still growing at a rate of 10% a year.

Mutual fund assets now total Rs67tn and are growing at a rate of 44% YoY, driven by a 60% YoY rise in equity fund assets to Rs39tn in September.

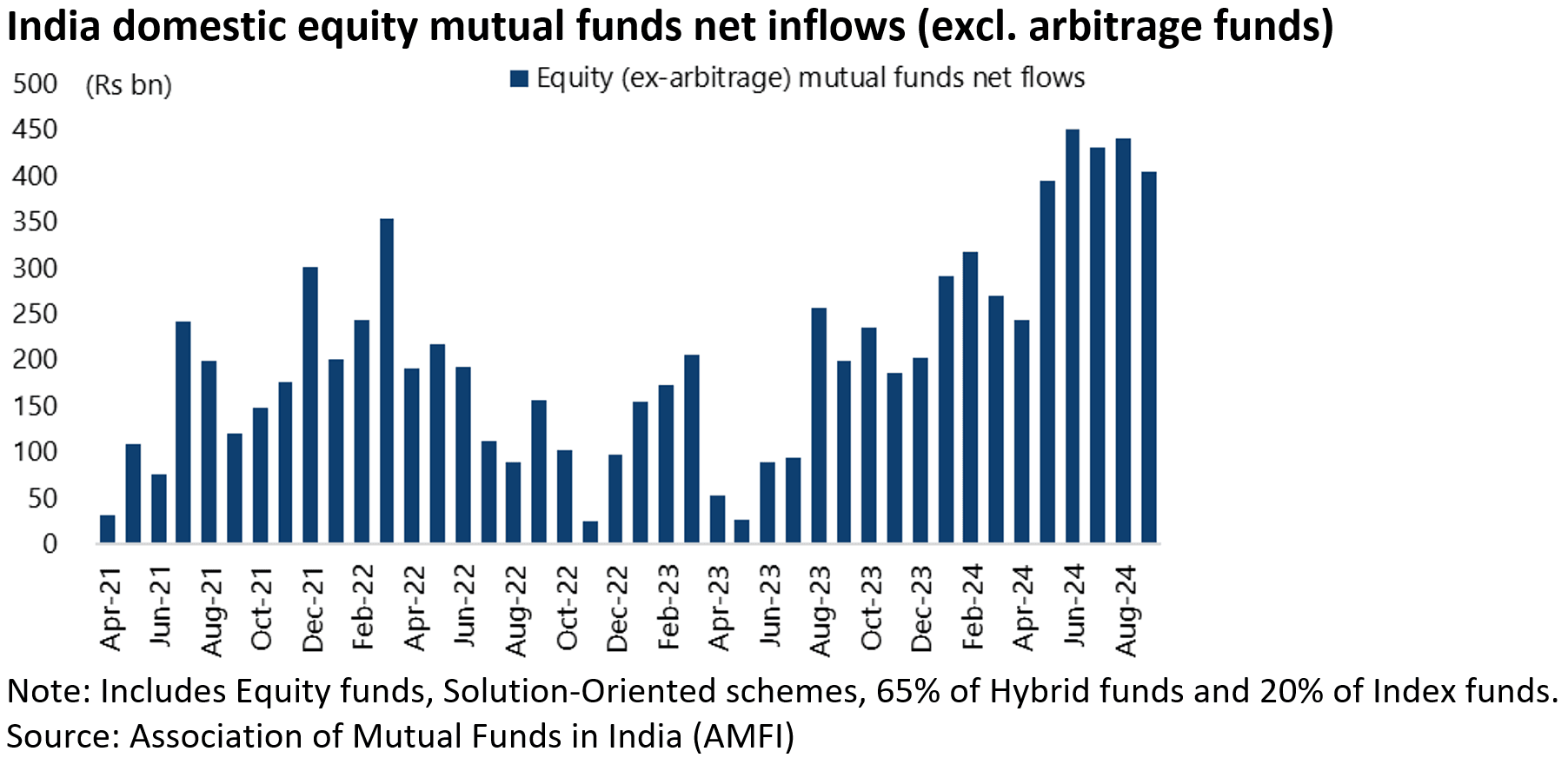

The latest data shows continuing strong inflows into equity funds. Net inflows into equity mutual funds (excl. arbitrage funds) rose to a recent high of Rs450bn in June and were still Rs405bn in September.

Out of this total the most stable inflow comes from the retail Systematic Investment Plan (SIP) where ordinary people invest a fixed portion of their monthly salary into equities.

Monthly SIP contributions rose by 53% YoY to a record Rs245bn in September with 98.7m outstanding SIP accounts.

The average monthly payment on a SIP is only Rs2,482 (US$29.6).

If the domestic inflows into equities have remained strong, the supply of equity is now catching up as corporates, for entirely logical reasons given the higher valuations, look to raise equity.

Still, for now at least, the inflows into equities continue to outpace the supply of new equity.

Thus, last month more than US$10bn of domestic inflows went into the stock market while the new supply was US$7bn.

In the first ten months of 2024 new supply was about US$60bn or an average US$6bn per month.

Part of this supply is private equity groups selling down investments.

PE exits accounted for 23% of the total equity supply of US$60bn in the first 10 months of calendar year 2024.

There is also a booming IPO market.

The number of IPOs in India rose by 65% YoY from 165 in FY23 to 272 in FY24 ended 31 March and is up 69% YoY to 184 in the first six months of this fiscal year (April-September 2024).

Ernst & Young also reported in February that the Indian stock exchanges were global leaders in IPOs for the calendar year 2023 with 220 deals, accounting for 17% of global IPO volume, up from 6% in 2021 and 11% in 2022.

All of the above may be viewed as classic signs of a market top, with mid-caps trading at 31x forward earnings, though down from a recent peak of 36x in September, compared with 21.9x for the Nifty benchmark.

Clearly, corrections can happen at any time.

Still India looks set to enjoy a long runway of healthy real GDP growth running between 6-8% which should translate into nominal GDP growth averaging between 10-12%.

The other point is that any meaningful correction, say of more than 10%, is likely to result in increased foreign buying given that the data now suggest that global emerging market investors are barely overweight.

This is the result of both India’s neutral weighting rising as a result of its outperformance and foreigners’ ongoing reluctance to buy aggressively because of the prevailing high valuations.

India’s neutral weighting in MSCI Emerging Markets is now 18.9%, up from 7.7% in March 2020.

MSCI India has outperformed MSCI Emerging Markets by 113% since the relative low reached in early April 2020.

CAPEX Cycle is a Major Tailwind for India

Meanwhile, the macro case to view any correction in India as a buying opportunity is the growing evidence of a private sector capex cycle.

Reserve Bank of India data published in August showed the highest fund raising for new projects in ten years.

Thus, private project funding approvals have risen by an annualised 20% from Rs2.71tn in FY20 to Rs5.66tn in FY24 ended 31 March.

The relevant point for equity investors is that the last time India had a private sector capex cycle, in the FY02-FY08 period, the country’s stock market enjoyed massive outperformance in Asia.

The macro evidence of a new private sector capex cycle is again best reflected in the rising share of gross fixed capital formation as a percentage of nominal GDP.

This has risen from a recent low of 27.3% in FY21 to 30.8% in FY24.

Meanwhile, the big increase in government capex on infrastructure in the past ten years under the BJP government has served as the enabling factor to give a deleveraged private sector the confidence to invest, which was always the original intention.

Central government capital expenditure has risen from Rs1.9tn in FY14 to Rs9.5tn in FY24 and is budgeted to rise to Rs11.1tn this fiscal year.

Still if this was always the intention, it is reassuring to see the growing evidence that the private sector is indeed now taking up the baton, to use the analogy of a relay race.

Housing Market is Healthy and Ready for a Boom

Meanwhile the new capex cycle was preceded by an upturn in the residential property market which is now into its fourth year of rising sales and prices following an eight-year downturn between 2012 and 2020.

There are good reasons why the current property cycle could run for another four to five years with sales growth running at 15-20%.

With unsold inventory in the seven major cities running near a 13-year low (see following chart), it is also the case that developers have so far remained disciplined on price hikes, which are running at “only” 8-10% YoY to maintain affordability.

With the average age of homebuyers declining in recent years from 44 to 33, banks have been extending longer duration mortgages up to 25 years.

This eases the monthly debt servicing burden though the tendency for Indian homeowners remains to prepay as soon as they can afford to.

Meanwhile with mortgage rates, by historical standards in India, at a relatively low 8.5-9%, the property market can probably look forward to RBI rate cuts following the now commenced Fed easing cycle.

Interest Rate Outlook More Hawkish than in the US, But Still Room to Cut

But no one is expecting aggressive rate cuts by the RBI which remains restrictive.

Still there is undoubtedly room to cut in terms of the level of real rates, most particularly if looking at core CPI.

The RBI policy repo rate, deflated by core CPI, is now 3.0% and 1.0% if deflated by headline CPI.

While the formal inflation target is headline CPI, the reality is that it is influenced heavily by food prices which is out of the control of any central bank.

The RBI is now projecting 4.5% CPI inflation in FY25 ending 31 March 2025.

This compares with the official inflation target of 4% with a tolerance band of +/- 2 percentage points.

What about the priorities of the Modi government in its recently commenced third five-year term?

Discussions recently in the Indian capital reveal less focus on passing new laws and much more focus on deregulation, in terms of fully dismantling the legacy of the so-called Licence Raj in terms of a bonfire of, or at least a simplification of, unnecessary permits, rules and regulations.