What You Should Own if The Fed Cares More About Jobs Than Inflation

Author: Chris Wood

There is no doubt that the pain trade in recent months got ever more painful for those equity investors still defensively positioned as confidence has grown that AI provides the next productivity-enhancing growth narrative for the coming decade.

It is also conveniently, giving continuing inflationary concerns, deflationary in nature.

AI, so the thinking goes, is in the foothills of the next bubble.

This is indeed a powerful narrative which the cautiously inclined have needed to treat with respect.

Still that does not necessarily mean that the six Big Tech stocks, defined as FAANGM, will be the dominant thematic for the next ten years as they were for the last ten.

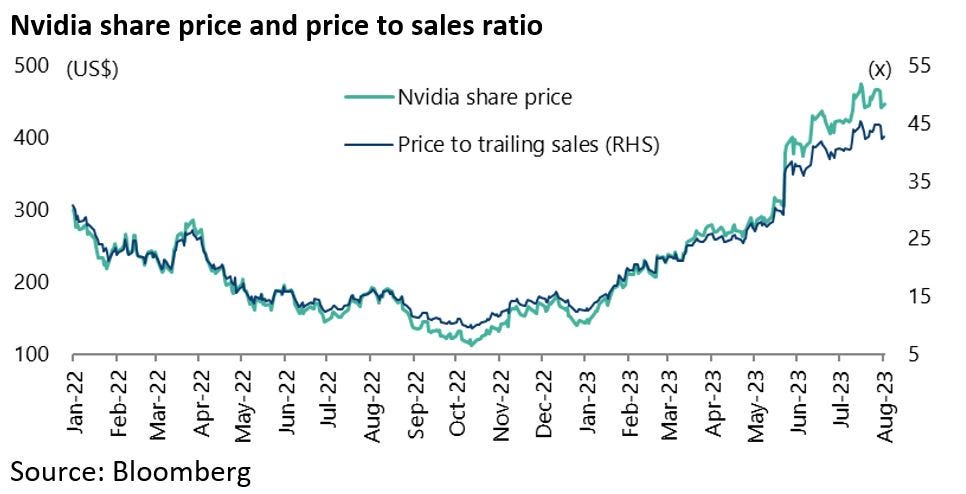

This writer is most convinced that the “picks and shovels” theme for AI remains the most compelling story for now, which is why Nvidia remains the core holding despite its current valuation of 43 times sales.

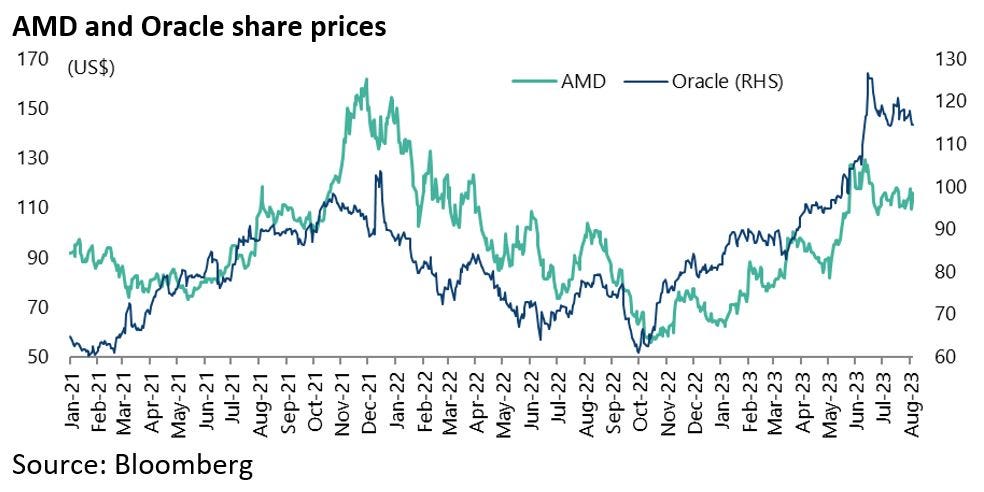

Meanwhile it is no surprise to see the likes of AMD and Oracle rally of late as investors look for theoretical catch-up plays on the AI theme.

AMD’s and Oracle’s share prices have risen by 30% and 21% respectively since the beginning of May and are up 112% and 88% from their low reached in September/October 2022.

By contrast, Nvidia is up 313% since bottoming in October 2022.

Still it is also the case that, by the end of last quarter, there was growing evidence of investor capitulation on the return of Big Tech theme.

A recent famous monthly survey of global fund managers by a US bank released in mid-June showed that investors were “exclusively long” tech stocks with 55% of the participants saying “Long Big Tech” is currently the most crowded trade.

The survey also found that 40% of the participants expect that if widespread adoption of AI in the next two years will drive corporate profits higher (see Bloomberg article: “BofA Poll Shows Investors Speeding Exclusively Toward Tech”, 13 June 2023).

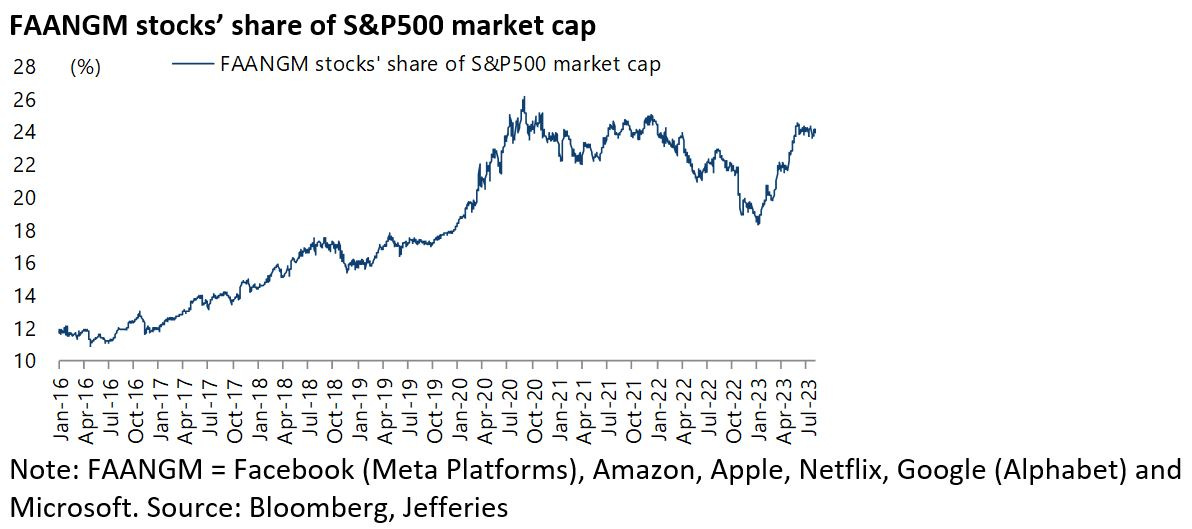

Meanwhile FAANGM as a percentage of S&P500 market cap is almost back at its September 2020 all-time high. The six stocks’ share of S&P500 market cap has risen from a recent low of 18.3% on 5 January to a recent high of 24.6% on 1 June and is now 23.9%, compared with the peak of 26.2% reached on 1 September 2020.

This writer had been assuming, until the AI theme entered the markets with Microsoft’s announcement on 23 January of a “multiyear, multibillion dollar” investment in ChatGPT-maker OpenAI, that the 1 September 2020 high marked the long-term high.

But that conviction was abandoned at that point given the likely temptation for investors to regard the Big Tech index heavyweight names as AI plays.

Still to this writer who is no tech expert, Microsoft and Alphabet (in that order) seem much more legitimate AI plays than the likes of Apple, Amazon and Meta.

For the latter stocks the key bullish theme in recent months has been cost cutting in the context of flat or negative revenue growth.

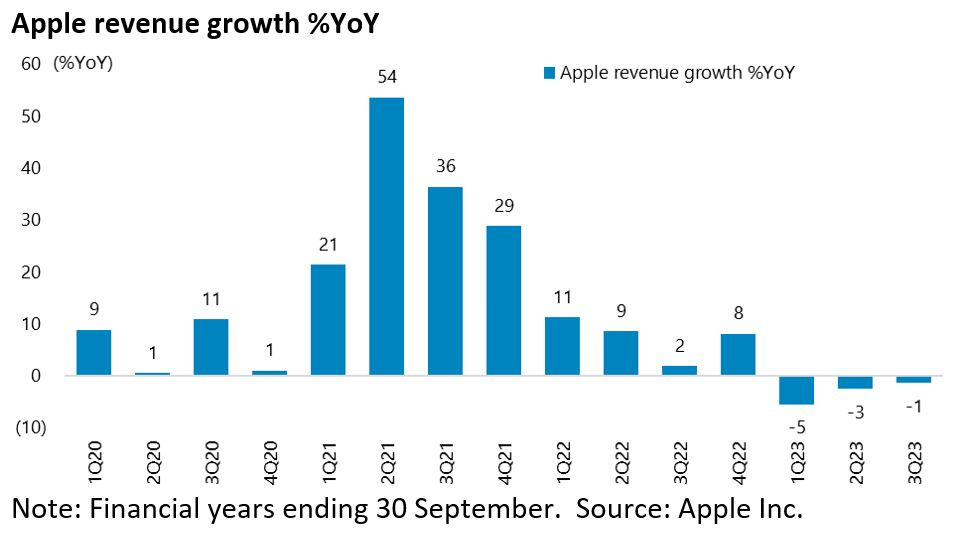

For example, Apple’s revenue for its 3QFY23 ended 1 July declined by 1% YoY, the third quarter of declining YoY revenue.

Big Tech has also made savings by stretching out depreciation schedules.

Thus, Meta confirmed in February that it has raised the estimated useful life cycle of its servers and network equipment from four years to five resulting in a reduction in depreciation expenses of US$860m in 2022. Similarly, Alphabet also announced in February it will increase the lifespan of its servers from four years to six reducing depreciation by about US$3.4bn for this fiscal year.

These followed moves by Microsoft and Amazon last year when they raised the expected life cycle of their servers from four to six years and five years, respectively.

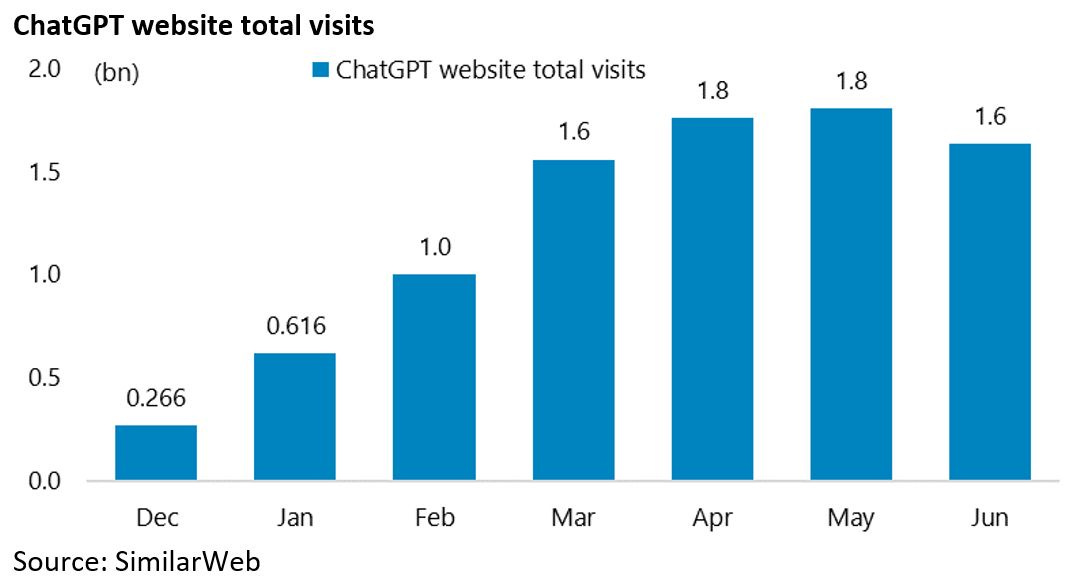

Meanwhile the latest numbers on ChatGPT usage remain as dramatic as ever.

The ChatGPT website’s estimated monthly visits have surged from 266m in December to 1.8bn in May and 1.6bn in June, according to web-traffic tracker SimilarWeb.

Will the Fed Prioritize Employment or Inflation?

Still it is clear that more near-term macroeconomic issues cannot be ignored completely even in the context of an emerging AI bubble.

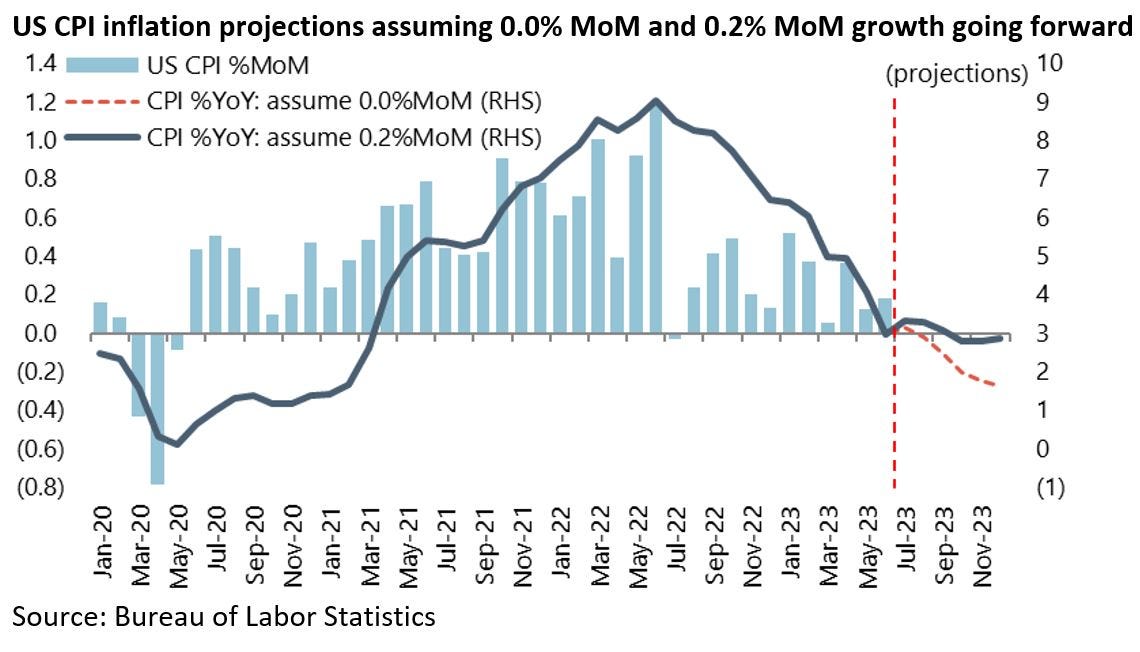

It is worth noting that the base effect stops being positive, from a US CPI standpoint, from the July data point which will be announced on 10 August.

For the record, the monthly increase in CPI peaked at 1.2% MoM in June 2022 and declined to 0.0% in July 2022.

As a consequence, if CPI increases by 0.0% MoM going forward, the CPI inflation rate will rise from 3.0% YoY in June to 3.1% YoY in July and then decline to 2.9% YoY in August.

While if CPI increases by 0.2% MoM going forward, the inflation rate will rise to 3.3% YoY in both July and August and then slow to 2.8% YoY in October-December.

This raises the core issue in coming months of which part of its dual mandate the Fed will prioritise if there starts to be more evidence of labour market weakness in the absence of any sign of inflation nearing the Fed’s 2% target.

This writer’s base case remains that in the event of real evidence of labour market weakness the Fed will quickly prioritise employment over the 2% inflation target in the context of the approaching presidential election.

If this is right, the logical market consequence will be a further sell-off in Treasury bonds and a renewed preference for cyclical stocks over growth stocks given the combination of renewed monetary easing and higher Treasury bond yields.

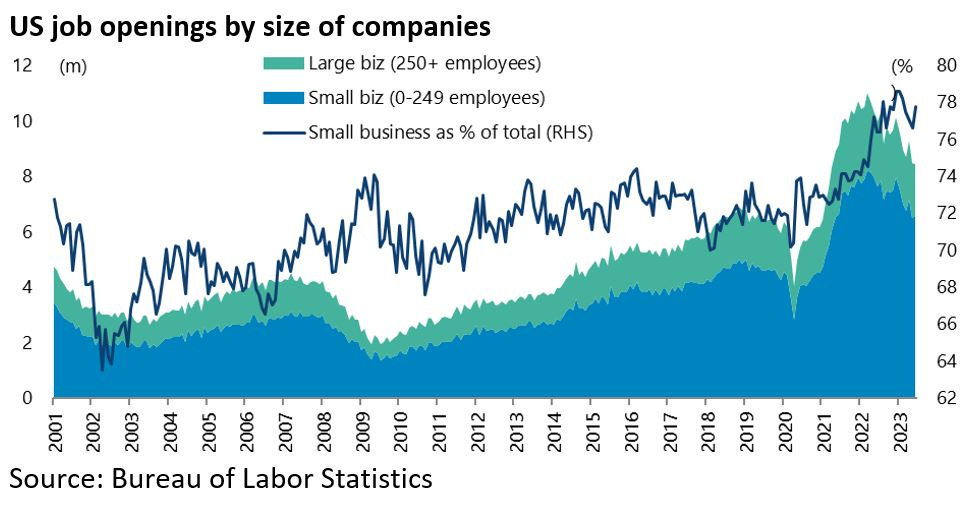

Still there will be no pronounced labour market weakness unless the small business sector starts shedding labour since small businesses with less than 250 employees account for 75% of US private sector employment.

They also accounted for 77.8% of the private sector job openings in June, though down from a peak of 78.6% in December.