The US Economy is Strong...But for How Much Longer?

Author: Chris Wood

The base case remains that the US is heading into a downturn in 2024 as signaled by the collapse in M2 growth.

Still there is no doubt that the Federal Reserve’s perceived pivot at the December FOMC meeting has further increased investors’ confidence that any US downturn will be met by aggressive interest rate cuts and, most probably, renewed Fed balance sheet expansion.

From an equity standpoint, it is only natural that stock markets should have celebrated the perceived end of monetary tightening and the seeming pending commencement of easing after 525bp of Fed tightening, the most aggressive monetary tightening cycle since 1981.

But stocks will not react positively if the US economy still succumbs to a recession, which most economists have now given up forecasting in contrast to what was the state of play last year.

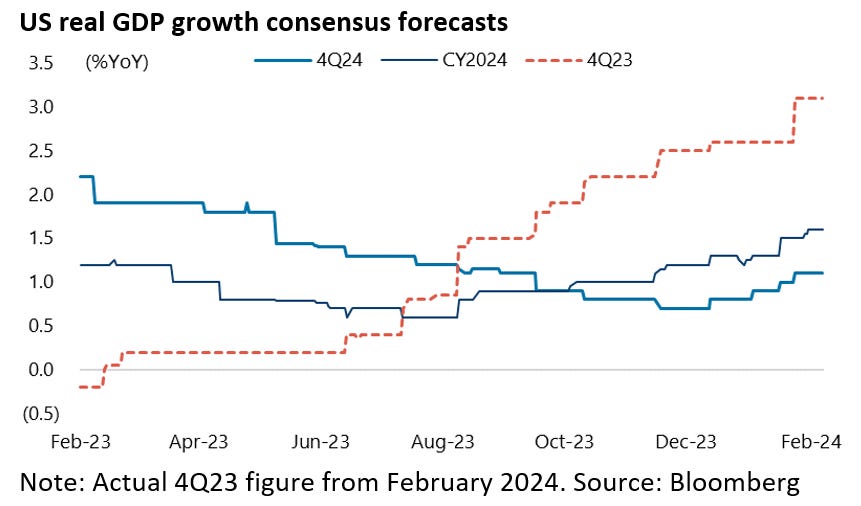

At the start of 2023 the consensus expected US real GDP to grow by only 0.3% YoY in 2023 and decline by 0.1% YoY in both 3Q23 and 4Q23.

By contrast, the consensus now expects real GDP to grow by 1.6% YoY in 2024 and by 1.1% YoY in 4Q24, after rising by 2.5% YoY in 2023 and by 3.1% YoY in 4Q23.

The Labor Market is Not as Resilient as Payrolls Suggest

As regards the state of the American economy, investors have understandably remained acutely focused on labour market data.

This has been weakening in recent months, albeit in a not dramatic way, which has fed the soft-landing narrative at least until last month’s surprising strong number.

US nonfarm payrolls increased by 353,000 in January while the increase for the previous two months was revised up by 126,000 (117,000 for December and 9,000 for November).

This compares with consensus expectations of 185,000 job gains in January.

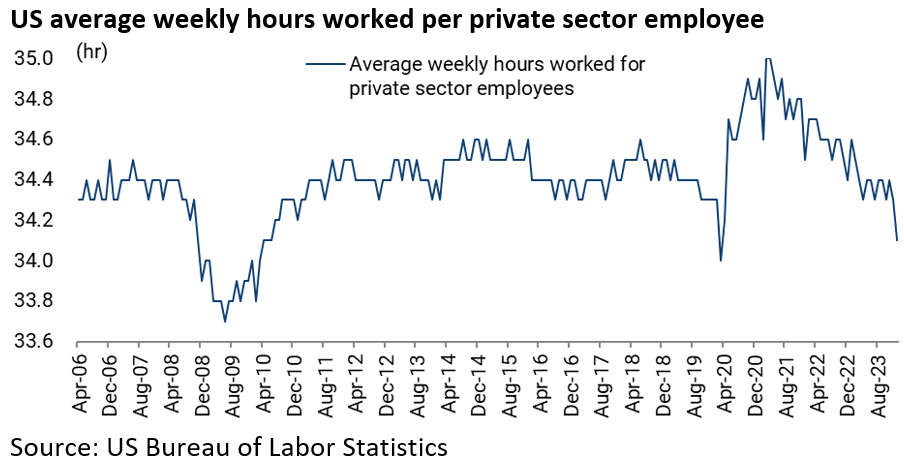

Still a closer look at the data suggests the labour market is not quite so resilient.

Average weekly hours worked per private sector employee declined from 34.3 hours in December to 34.1 hours in January, the lowest level since March 2020.

While the number of Americans quitting their jobs, a sign that they are confident to find a better job elsewhere, has declined from a peak of 4.5m in November 2021 to 3.39m in December 2023, the lowest level since January 2021.

Without Small Business Weakness, There is No Recession

That said, real labour market weakness will only come if SMEs start retrenching since small businesses employing less than 250 people account for 73% of US private sector employment.

The National Federation of Independent Business’ (NFIB) small business survey shows that the average interest rate paid on small business loans was 9.0% in January, up from 5.0% at the start of 2022.

Since SMEs cannot access the bond market, and therefore lock in previously ultra-low bond yields as most US corporates have successfully done, it would seem only a matter of time before there is more tangible evidence of labour market weakness as a result of the higher cost of borrowing.

Still it is hard to get concrete data on how much SMEs are borrowing in aggregate.

The other point is that, if and when labour weakness does come, it is likely to be quite sudden.

This is because there has been a marked tendency to hoard labour given the peculiarities of this cycle as a result of the difficulties experienced hiring people coming out of the pandemic.

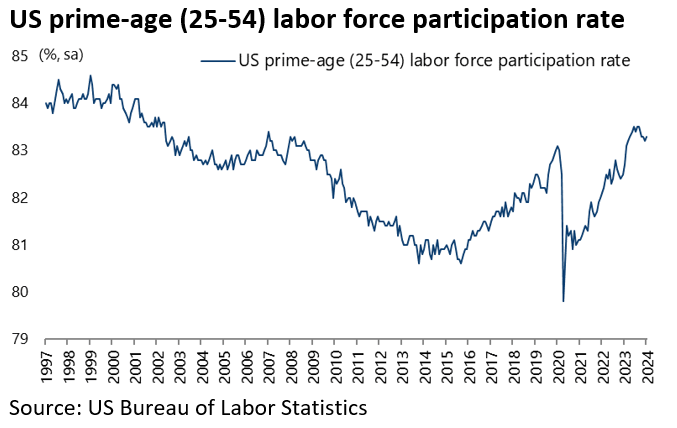

But with the so-called cumulative “excess savings” stemming from Covid-triggered transfer payments down to US$200bn in December, according to an interesting study by the San Francisco Fed, compared with a peak of US$2.14tn in August 2021 (see following chart and San Francisco Fed Blog article: “Data Revisions and Pandemic-Era Excess Savings” by Hamza Abdelrahman and Luiz E. Oliveira, 8 November 2023), the labour participation rate has been rising.

Indeed the participation rate of people in the key 25-54 prime working age category now exceeds the pre-pandemic level.

Thus, the prime-age labor participation rate was 83.3% in January, compared with the pre-pandemic high of 83.1% in January 2020.

Meanwhile, it should be noted that the San Francisco Fed measures excess savings as the amount of monthly personal savings above/below the pre-pandemic trend line over the 48 months prior to March 2020, the onset of the pandemic recession.

It is also worth noting again that the NFIB small business survey shows that small businesses have been reducing hiring plans.

The NFIB small business hiring plan index has declined from 32% in August 2021 to 14% in January 2024, the lowest level since May 2020.

If companies are getting more cautious about hiring, the key decision to cut employees will only likely occur if top-line revenue growth comes under downward pressure.

The US Economy Remains Resilient...But for How Long

If most of the above indicates growing pressures on the economy, the reality for now is that the US economy remained extraordinarily resilient in 2023, and the resilience of the US stock market should be seen in the context of nominal GDP growth running at an average of 6.3% YoY during those four quarters of 2023.

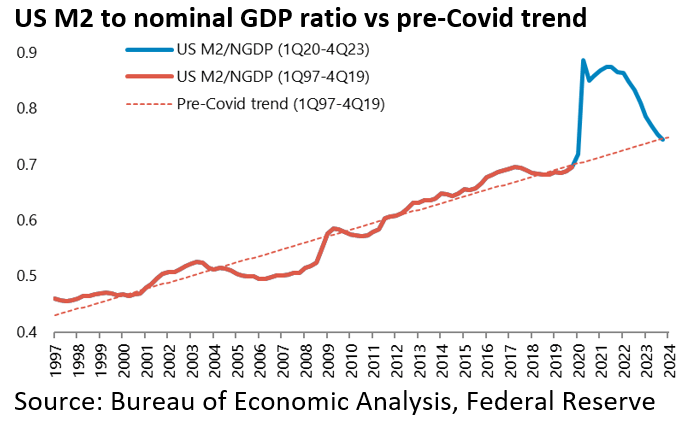

If a fiscal deficit running at an extraordinarily high annualised 6.5% of GDP in December has been one reason for this resilience, another explanation remains the equally extraordinary base effect from the historic expansion in M2 in 2020, as reflected in the chart below of the US M2 to nominal GDP ratio, updated for the latest revised data.

This has only finally come back to trend.

The ratio, at 0.744 in 4Q23, was just 0.2% below the pre-Covid trend between 1997 and 2019, though way down from the 25.9% above trend reached in 2Q20 when the Fed’s monetary expansion peaked.

Or, to put it another way, the liquidity contraction is only now beginning to bite.

Does a "No Landing" Benefit Stocks, Bonds or Both?

Finally, it also should be noted that recent weeks have started to see the soft-landing consensus questioned by what could be termed the “no landing” narrative as a result of more strong data following the payroll report.

The ISM services price paid index, for example, rose by 7.3 percentage points to 64% in January, the biggest increase since August 2012.

While the Atlanta Fed GDPNow model is projecting a US economy growing at 3.3% YoY in the current quarter, up from 3.1% YoY in 4Q23.

Any such “no landing”” outcome would be equity bullish and bond bearish since it would imply higher nominal GDP growth.

Meanwhile, this writer continues to believe that Treasury bonds entered a structural bear market in March 2020 when the 10-year yield bottomed at 0.31%.