The Stock Market is Eating The Economy

Author: Chris Wood

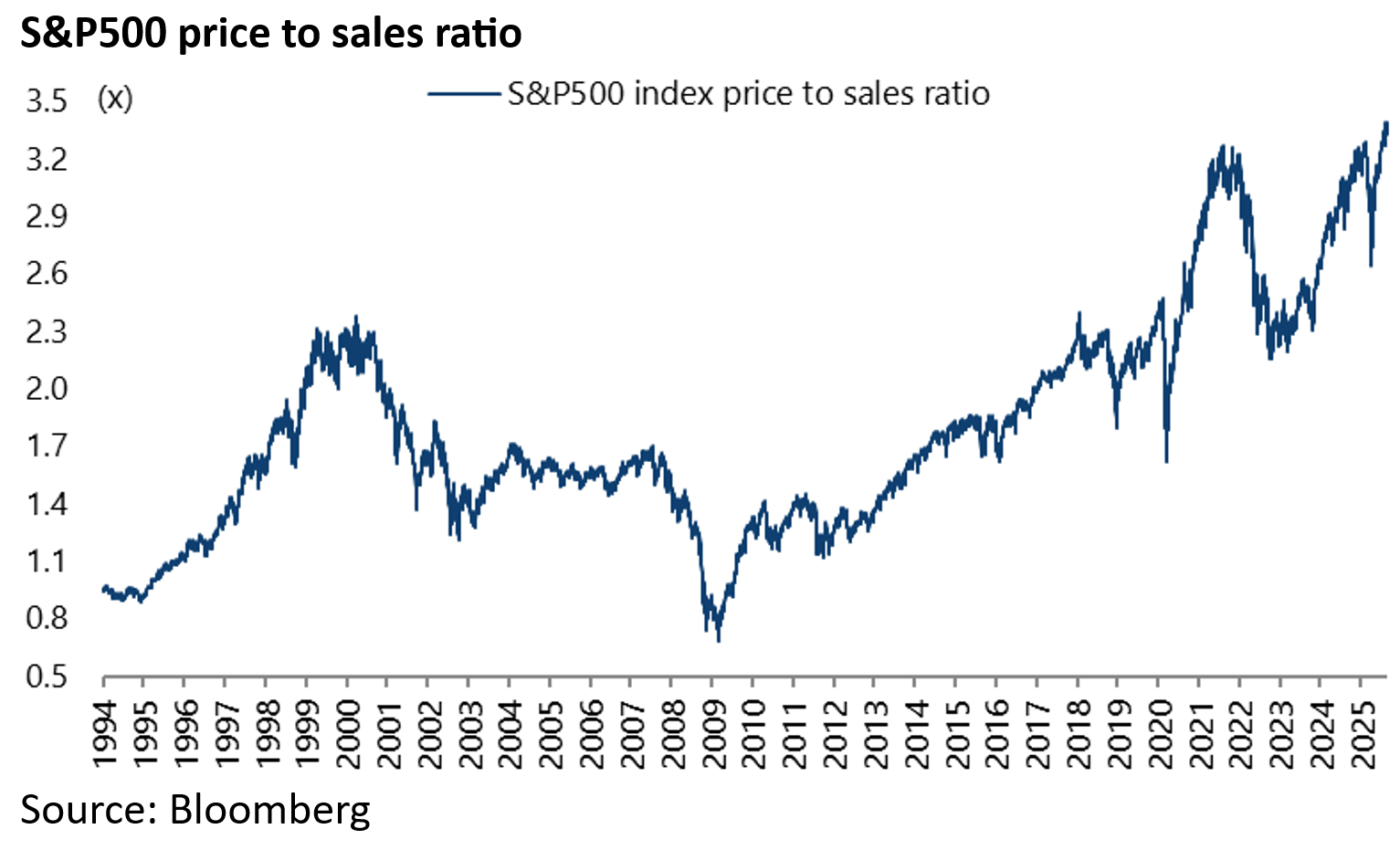

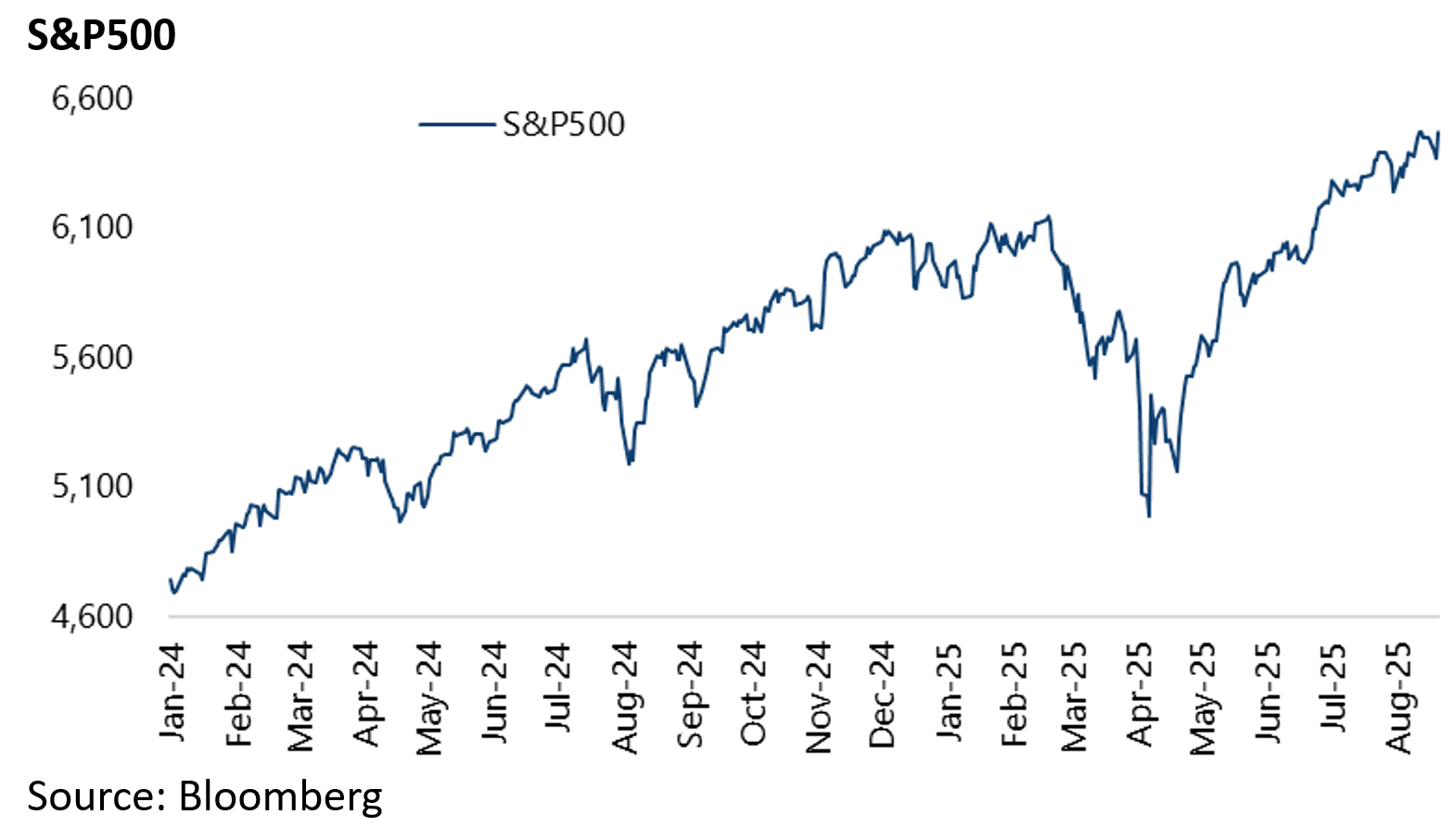

The US stock market remains extremely resilient in the face of the rise in tariffs.

Indeed, the S&P 500 is now trading at a record price to sales ratio of 3.39x.

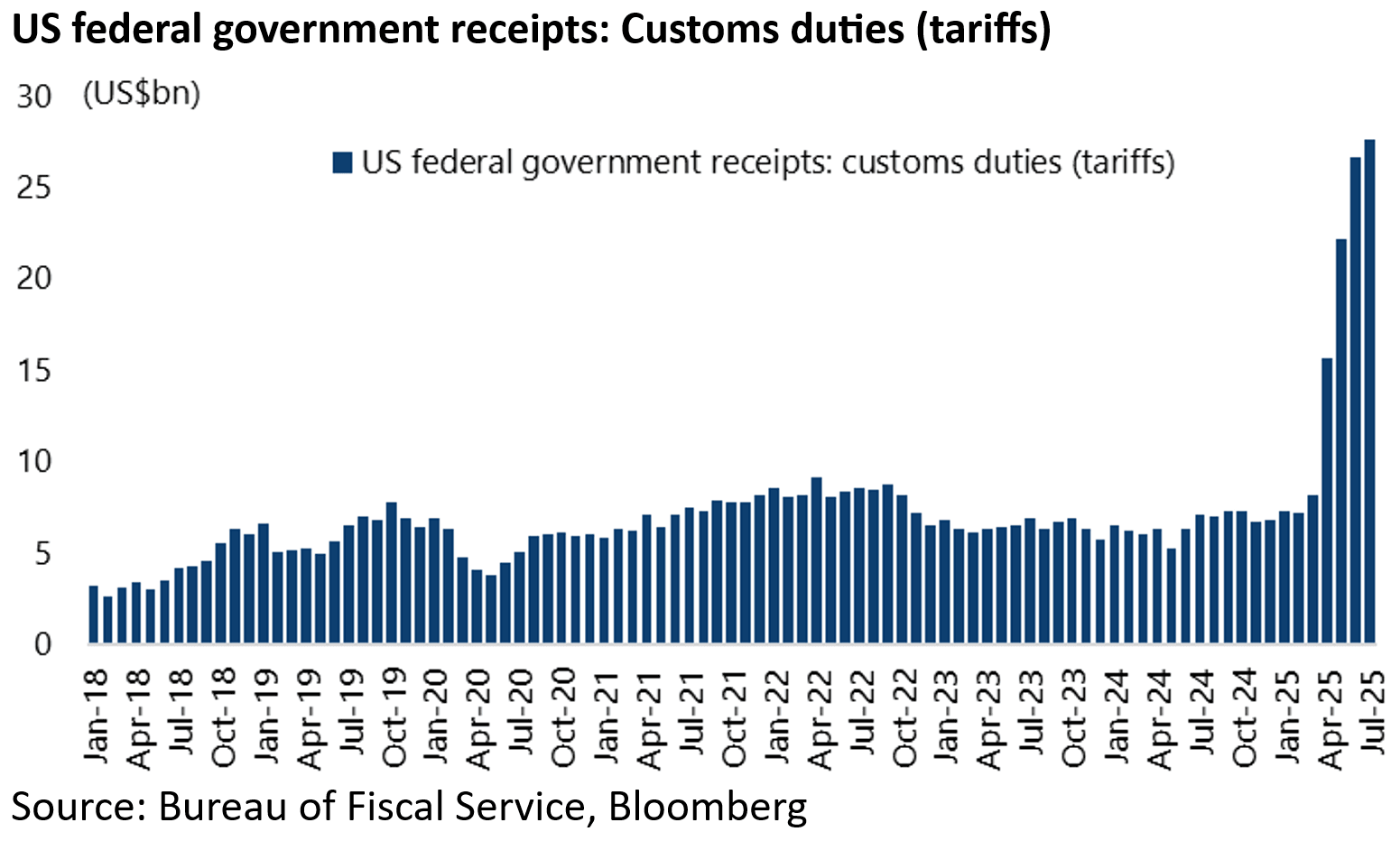

Meanwhile, the federal government is estimated to be receiving an annualised more than US$300bn from the tariffs.

The monthly tariff-related federal government receipts have risen from US$7.2bn in February to a record US$27.7bn in July or an annualised rate of US$332bn.

That is money somebody is paying, which will increasingly mean US consumers.

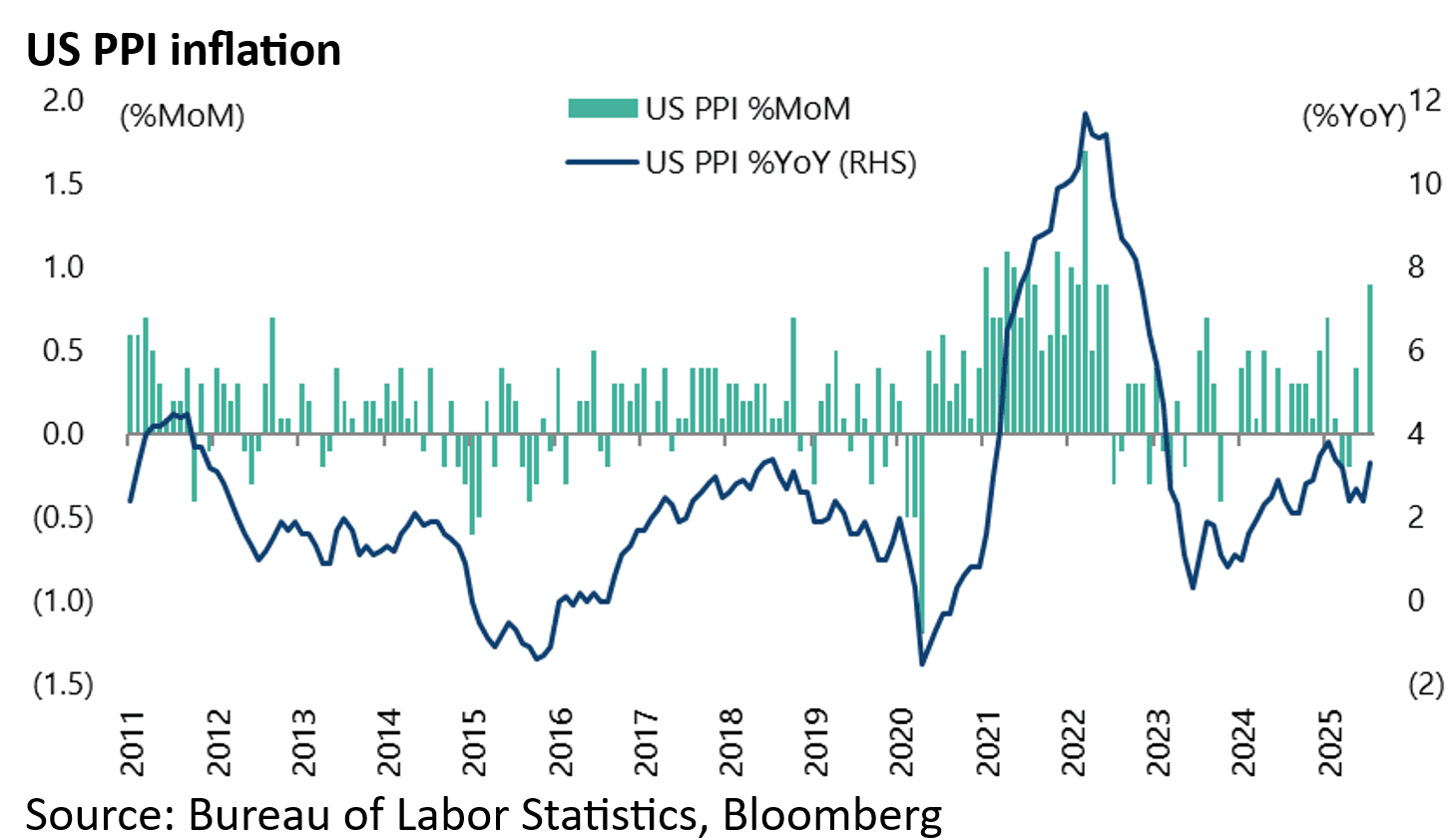

On this point, the first clear sign of the impact of tariffs in the “hard” data came with the latest PPI data.

US PPI rose by 0.9% MoM and 3.3% YoY in July, compared with consensus estimates of 0.2% MoM and 2.5% YoY.

This is the biggest MoM increase in more than three years since June 2022.

Another reason the stock market has been rallying has been the renewed focus on the bullish tax cutting part of Trump’s agenda, and the lack of any negative Treasury bond market reaction thus far as regards the anticipated US$3.4tn increase in federal debt by 2034 as a consequence of the “One Big Beautiful Bill” passed by Congress in early July.

This is the estimate of the Congressional Budget Office (CBO).

Still it should be noted that the CBO’s forecast is based on only 1.8-1.9% projected real GDP growth during that period.

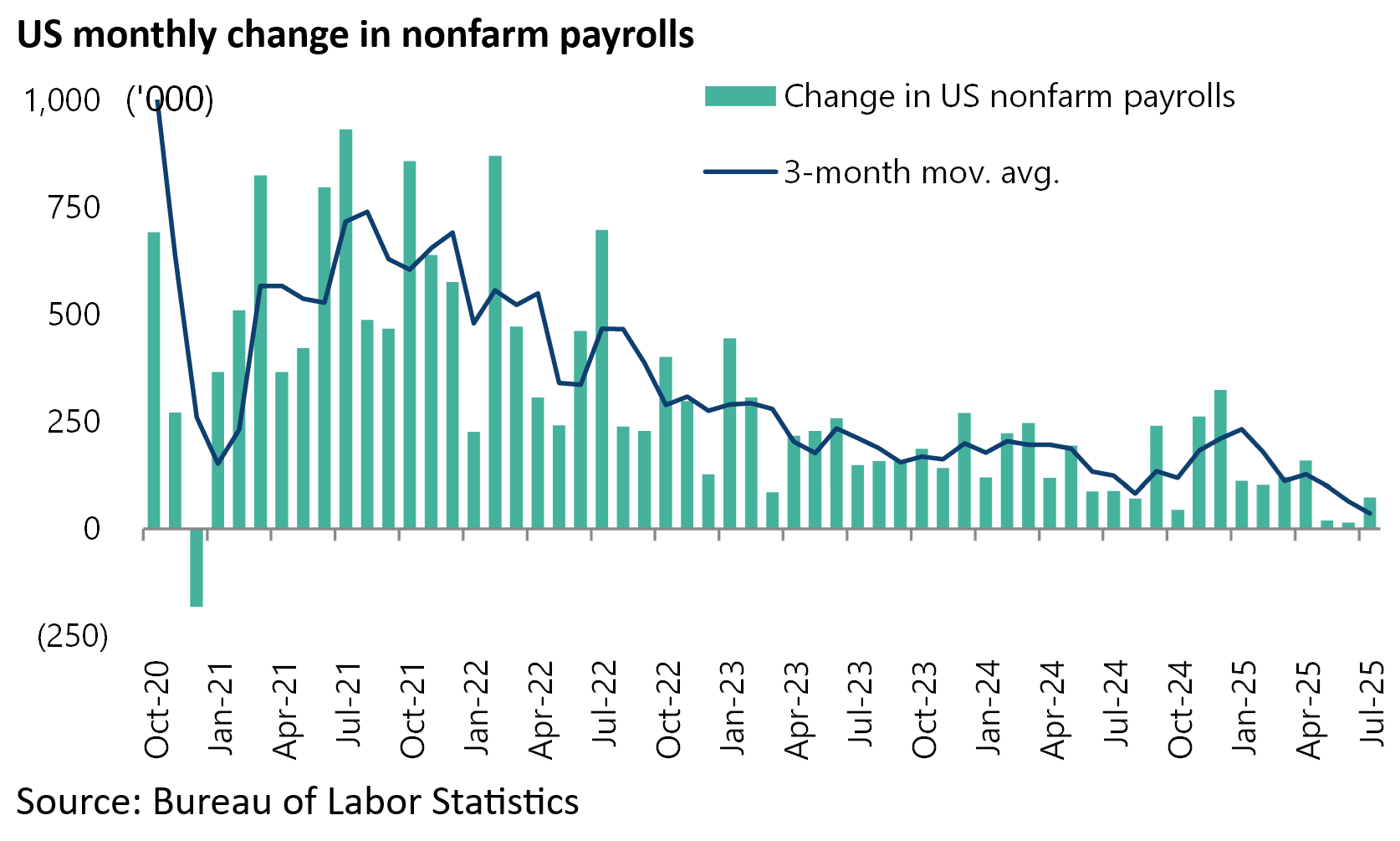

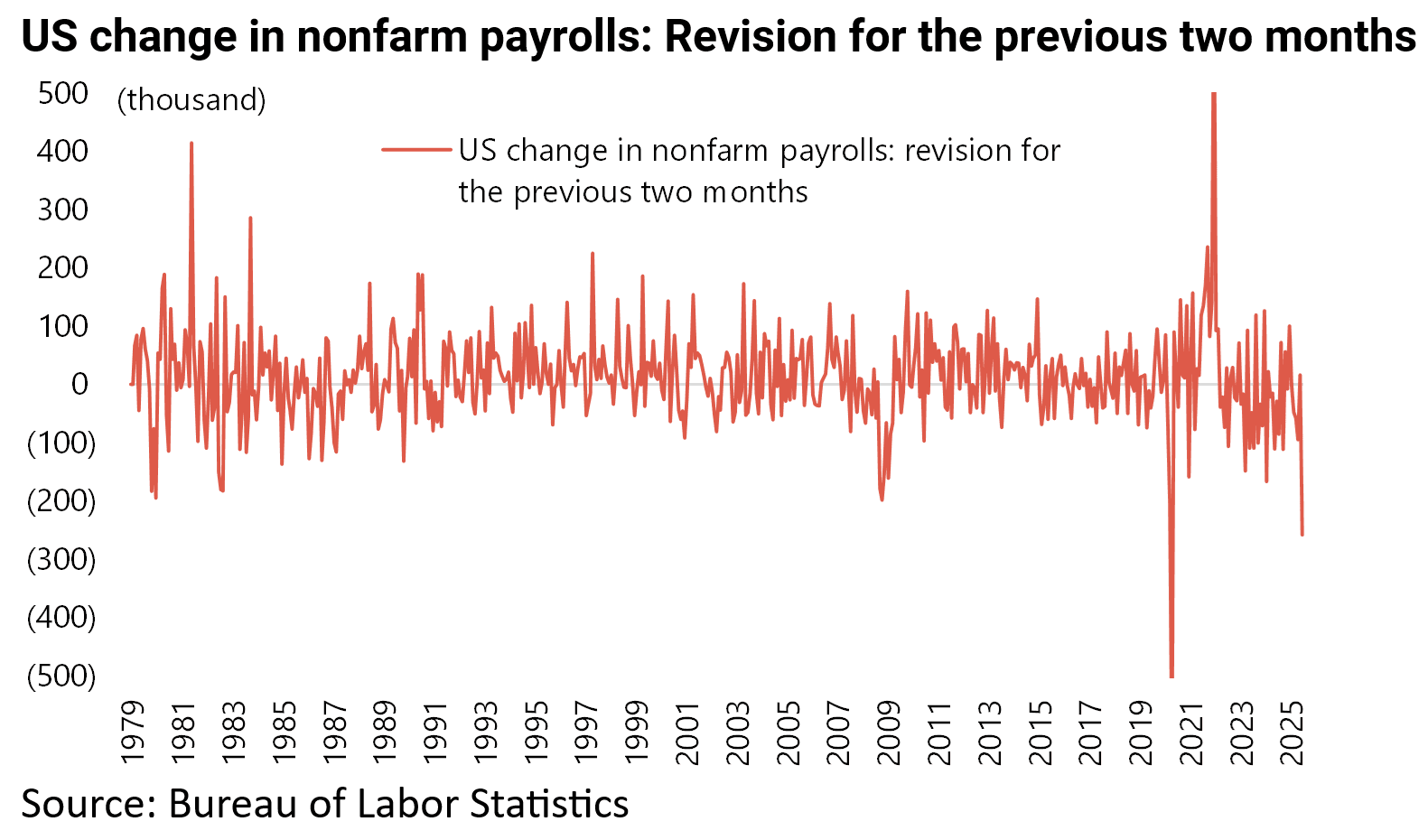

A further positive for the US stock market has been increased expectations of Fed easing coming sooner rather than later, based on last month’s weak employment report and dramatic downward reversions.

US nonfarm payrolls increased by only 73,000 in July, compared with consensus estimates of 105,000.

While the increase in the previous two months was revised down by 258,000, the biggest two-month downward revision since at least 1979 if the Covid period is excluded.

This is despite CPI inflation still running at 2.7% YoY in July and the looming impact of tariffs on prices. Still any short-term inflation effect from higher tariffs will likely not be sustainable given the longer term effect is deflationary, in the sense of the negative impact on consumers of what is effectively a tax hike.

How Important is Stablecoin Buying to Short Term Treasury Performance?

Meanwhile, the mounting political pressure on Fed Chairman Jerome Powell to cut rates is primarily explained by the Trump administration’s desire to get the cost of servicing the federal government debt down.

On this point, there is also the projected bid for short-term Treasury bills prompted by the stablecoin legislation passed in mid-July as recently discussed here (see Stablecoins, Bonds & Hyperscalers Oh My!, 24 July 2025).

Indeed Treasury Secretary Scott Bessent has openly referenced the demand for Treasuries that should be derived from this source.

Thus, he wrote in a social media post in mid-June that “a thriving stablecoin ecosystem will drive demand from the private sector for US Treasuries, which back stablecoins.”

On this point, it is worth noting the pushback that has come from some economists.

This is that any increase in demand due to shifts into stablecoins could be “offset almost 1:1 by a shift out of bank deposits, money market funds and currency”, to quote one monetarist economist this writer queried on this issue.

Or in other words the global demand for short-term Treasuries would not be changed, only the instruments by which people or firms hold the Treasuries.

Still this writer is not so sure about this since, in a situation where a new stablecoin is purchased, it is not bought from a commercial bank or another existing holder.

In which case there is no contraction of a balance sheet. On this point it is interesting to note that the minutes of the previous meeting of the Treasury Borrowing Advisory Committee (TBAC) held in late April revealed that there was a debate on precisely this issue. And the discussion continued in the latest meeting in late July as reflected in a TBAC letter to Bessent on 30 July.

To quote from the relevant section of the letter: “Increased stablecoin issuance could create a new source of demand for short-maturity Treasury securities.

While this might be offset by a reduction in demand from traditional Treasury investors if stablecoins act as a substitute for deposits, money market funds, or other cash-like instruments, much of the Committee seemed more optimistic about this as a source of new demand for T-bills.

"Potential impact to bank deposits bears close monitoring.”

That point about monitoring bank deposits clearly makes sense given this issue could well become of macro importance given the forecast growth in stablecoins.

Thus, one of the TBAC members in the April meeting projected that stablecoins could increase 8.3-fold by the end of 2028, rising from US$234bn to nearly US$2tn.

There is currently more than US$120bn of Treasury securities backing stablecoins.

Meanwhile, US bank deposits currently total US$18.4tn, while US money market funds total US$7.2tn.

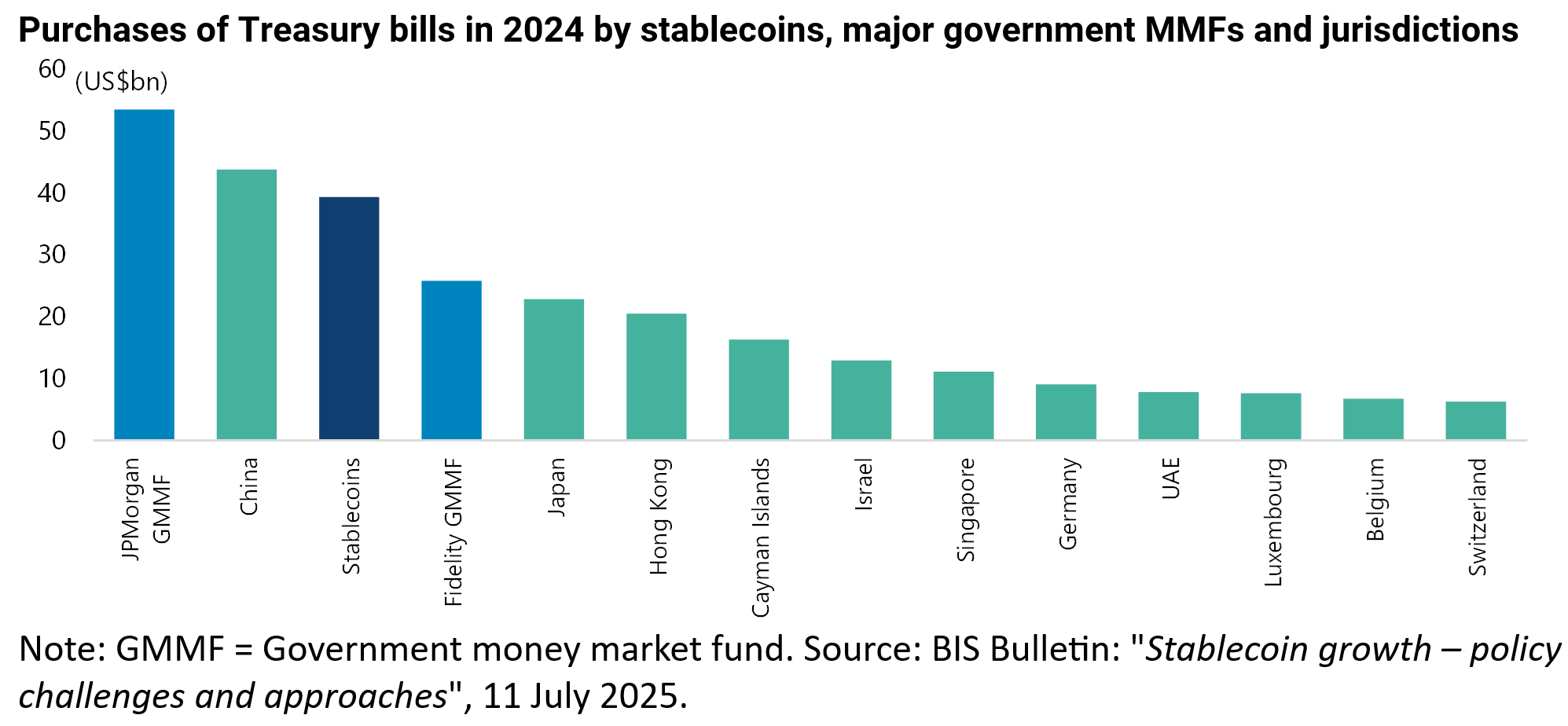

Meanwhile, it is also worth recording that the BIS estimated last month that stablecoins bought nearly US$40bn of Treasury bills in 2024, the third largest net buyer after JPMorgan Government Money Market Fund (US$53bn) and China (US$43.7bn) (See BIS Bulletin: "Stablecoin growth – policy challenges and approaches", 11 July 2025).

The BIS report also estimates that stablecoins’ current market capitalization has doubled from US$125bn less than two years ago to US$255bn with the two biggest issuers, Tether and Circle, accounting for 90% of the market capitalisation.

While the number of stablecoins in active use has soared from around 60 in mid-2024 to over 170.

The Stock Market has Become the Economy

Meanwhile the primarily retail-driven 33.8% rally in the S&P500 off the tariff-triggered 7 April low makes it clearer than ever that the stock market has become almost more important for the consumption-driven US economy than the economy itself.

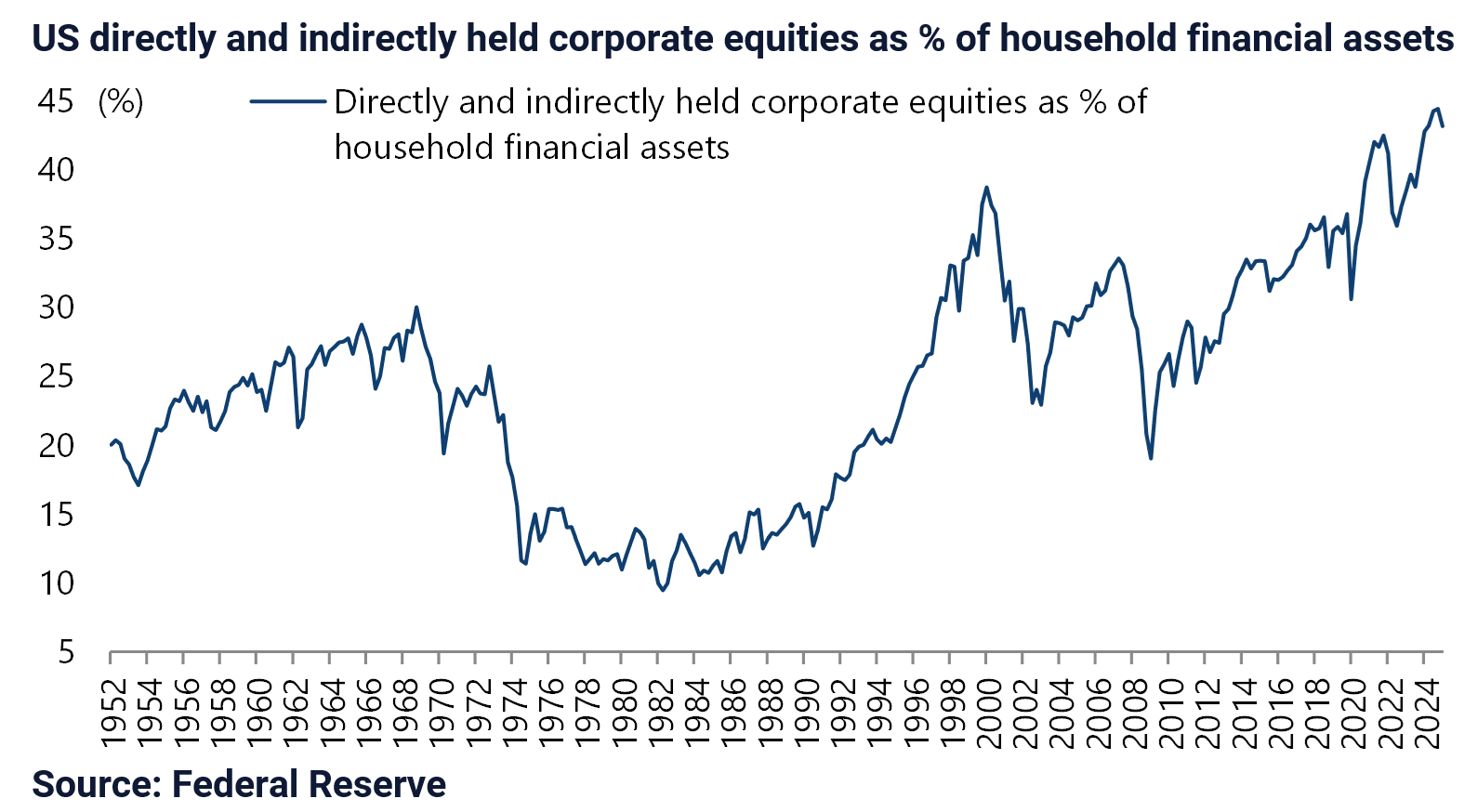

This is because of the high exposure of American households to the stock market.

Thus, the Fed’s latest flow of funds data shows that households’ directly and indirectly held corporate equities accounted for a record 44.4% of their financial assets at the end of 2024 and was still 43.1% at the end of 1Q25.

This is why it remains extremely important whether or not US Big Tech will be able to monetise AI capex as the relevant companies pursue the holy grail of so-called AGI.

This writer remains highly sceptical about this issue.

Meanwhile, Meta’s increasingly aggressive efforts to hire the best AI talent, which has been the subject of numerous articles in recent months (see, for example, Wall Street Journal article: “Zuckerberg Offers Big Bucks for AI Recruitment”, 23 June 2025), makes it clear that AGI is still a concept to be pursued, not a reality.