The Financial Assets Most at Risk From Trump's "Bull in a China Shop" Strategy

Author: Chris Wood

The 47th president has continued to behave like the proverbial bull in a China shop.

This is fundamentally bad for all US financial assets, particularly Treasury bonds and the US dollar.

Meanwhile, the equity rebound in recent weeks is the direct result of Donald Trump’s seeming U-turn on his stance on China tariffs, thereby confirming that the US does not have the cards in this particular poker game as discussed here previously (see In Tariff Negotiations, Trump Has No Ace Up His Sleeve, 29 May 2025).

Meanwhile, the US dollar index has broken below the 100 level with remarkable ease.

The index has declined by 11% from a recent high of 110.2 on 13 January to a recent low of 97.9 on 21 April and is now 99.3.

Long-term Treasury bond yields have also resumed rising of late even as the short-end discounts more Fed easing.

The 30-year yield is now 4.95% or 105bp above the two-year yield, after reaching 114bp on 21 April, the widest spread since January 2022.

Indeed the 30-year yield rose to an intraday high of 5.15% on 22 May, the highest level since 23 October 2023. The bond market action in the face of recent legitimate concerns about a tariff-triggered US recession is clear evidence not only that risk parity as a strategy no longer works but also that investors no longer view long-term Treasury bonds as “risk free”.

This is a very big deal, as discussed here on numerous occasions in the past.

If increased tariffs, or the lack of them, have been the main driver of market sentiment of late, there has also been the issue of Donald Trump’s recent verbal attacks on Federal Reserve Chairman Jerome Powell.

This is clearly much less important than the on-again-off-again noise regarding the tariffs.

Still, Trump’s attacks are gratuitous in the extreme and serve no purpose save to conjure up a scapegoat for any recession that might eventuate.

Indeed, in some respects, Trump’s attacks have turned Powell into the perceived Volcker figure he never really was, given his well-established track record is to pivot at the first sign of any risk-off pressure in the markets.

It also should be noted that the Fed has already sharply scaled back, as from the start of April, the pace of Fed balance sheet contraction.

Thus, the Fed announced in the March meeting that it will slow the pace of decline of its Treasury holdings from US$25bn to US$5bn a month beginning in April, though the monthly decline of its mortgage agency debt holdings will be maintained at US$35bn.

What Will Trigger an acceleration in Central Bank Bond Buying?

Meanwhile, if long-term bond yields keep rising again, it will not be long before the Fed resumes quanto easing to support the Treasury market, even though any such action will only accelerate US dollar weakness.

The pressure point here seems to be the 10-year Treasury bond yield rising materially above 4.5% toward the 5% level.

In this respect, what is remarkable about the dollar’s current weakness is that the currency has depreciated by 8.9% against the euro so far this year.

Even as the ECB has cut the deposit facility rate by 75bp to 2.25% while the Fed has remained on hold.

How Adjusting the SLR Could Relieve Selling Pressure on Treasuries

Still, before the Fed adopts renewed quantitative easing, there is one obvious stopgap to reduce selling pressure in the Treasury bond market, and it could be approved at any time.

That is easing the so-called Supplementary Leverage Ratio (SLR).

This would have the practical effect of allowing major US commercial banks to buy more Treasury bonds.

The SLR, a non-risk weighted capital requirement established in 2014, requires the largest US commercial banks to hold Tier-1 capital equivalent to at least 5% of their total assets, regardless of the assets’ risk weightings (and 3% for other banks).

This includes Treasuries and reserve deposits at the Fed.

Exempting Treasuries from the calculation could reportedly allow banks to increase their holdings of Treasury securities by potentially up to US$1tn.

On this point, both Treasury Secretary Scott Bessent and Fed governor Michelle Bowman, Trump’s nominee and Vice Chair for Supervision at the Fed, have been calling for adjusting the SLR by taking Treasuries out of the SLR calculation.

It is also the case that the Fed’s banking supervision responsibility is now under Treasury oversight.

Such stopgap measures will support Treasury bond prices in the short-term - just as the rule allowing US commercial banks not to mark their Treasury bond holdings to market, if they have stated they will hold them to maturity, has been a support in the recent past.

Still, this writer remains firmly of the view that long-term Treasury bonds are in a structural bear market, the end game of which is not only likely to be yield curve control but also potentially foreign exchange controls.

The Fed Stands Ready to Cut Rates in a Recession, But Will Private Debt be Able to Flash a Warning Sign the Fed Can See?

Meanwhile, if Donald Trump has caused a renewed focus on the issue of “Fed independence” beloved by talking heads on TV, the reality is that no central bank, be it G7 or otherwise, is truly independent of its political masters. To think otherwise is to be monumentally naïve.

The reality is also that the Fed will likely start easing at the first sign of wealth destruction turning into credit revulsion, which is what would happen in a recession.

In this respect, there is a lot of potential for credit spreads to widen further.

But this cycle will be somewhat different from prior ones because of the important role played by the booming private credit asset class where there are no credit spreads to flash warning signals.

On this point, Bloomberg reported recently that Moody’s Ratings has warned of late that private equity sponsors will face difficulties supporting and exiting their investments if trade tensions erode business confidence and delay investment.

Many of these investee companies are facing cash flow pressure because their leverage buyouts took place in 2021 and 2022 when interest rates were much lower and valuations higher (see Bloomberg article: “Private Equity Backed Firms Face Cash Struggles, Moody’s Says”, 8 April 2025).

The same article also noted that around 15% of total rated corporate debt in North America is B3 negative or lower, with private equity firms owning half of that, according to Moody’s.

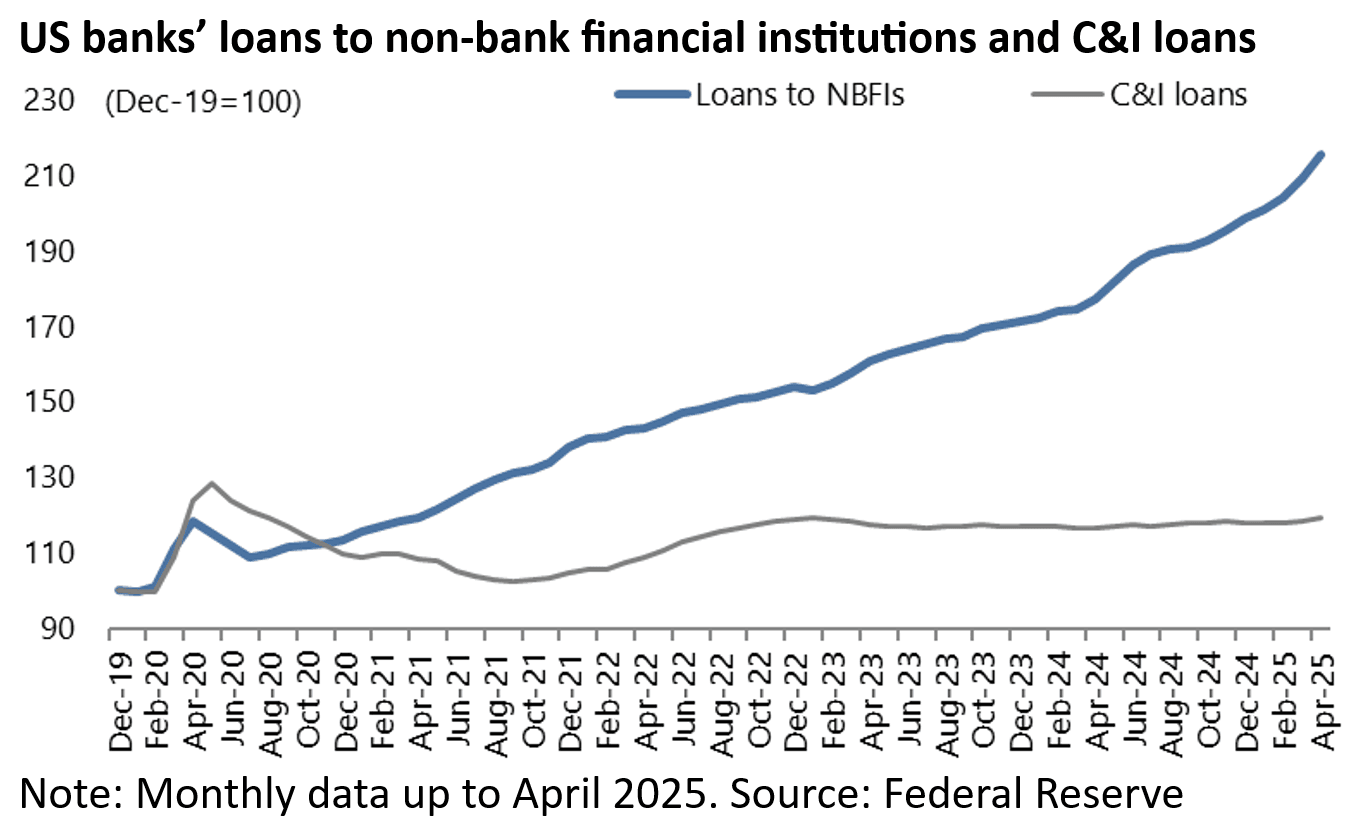

Moody’s has also reported that private credit and private equity now represent nearly 40% of total US banks’ loans to those non-depository financial institutions (NDFI), a category of borrowers that is far outpacing all others.

Thus, US commercial banks’ loans to non-bank financial institutions (NBFIs) rose by 21.4% YoY to US$1.25tn in April, while commercial and industrial (C&I) bank loans rose by only 2.4% YoY to US$2.8tn.

Interestingly, Moody’s 2024 global survey of 32 banks involved in private credit showed that the 18% average annual growth in lending to these firms in 2021-23 nearly matched the rapid 19% increase in capital raising by private credit funds over the same period (see Moody’s report: “Private credit, a refuge in turbulent times, set to take share again”, 17 April 2025).

Evaluating the Impact of the US-Chinese Tariff Battle

This is one reason why the private equity industry, along with many others, will have been lobbying of late for a real U-turn on tariffs, as opposed to just a temporary one, to reduce the recession risk.

There has of late been growing anecdotal evidence of a massive cancellation of orders from China.

Container booking data from Vizion’s TradeView Platform shows that total US import bookings plunged by 35% from 353,896 TEUs (twenty-foot equivalent units) in the week ended 24 March to 230,223 TEUs in the week ended 28 April, while US import bookings from China declined by 61% from 134,911 TEUs to 52,073 TEUs over the same period.

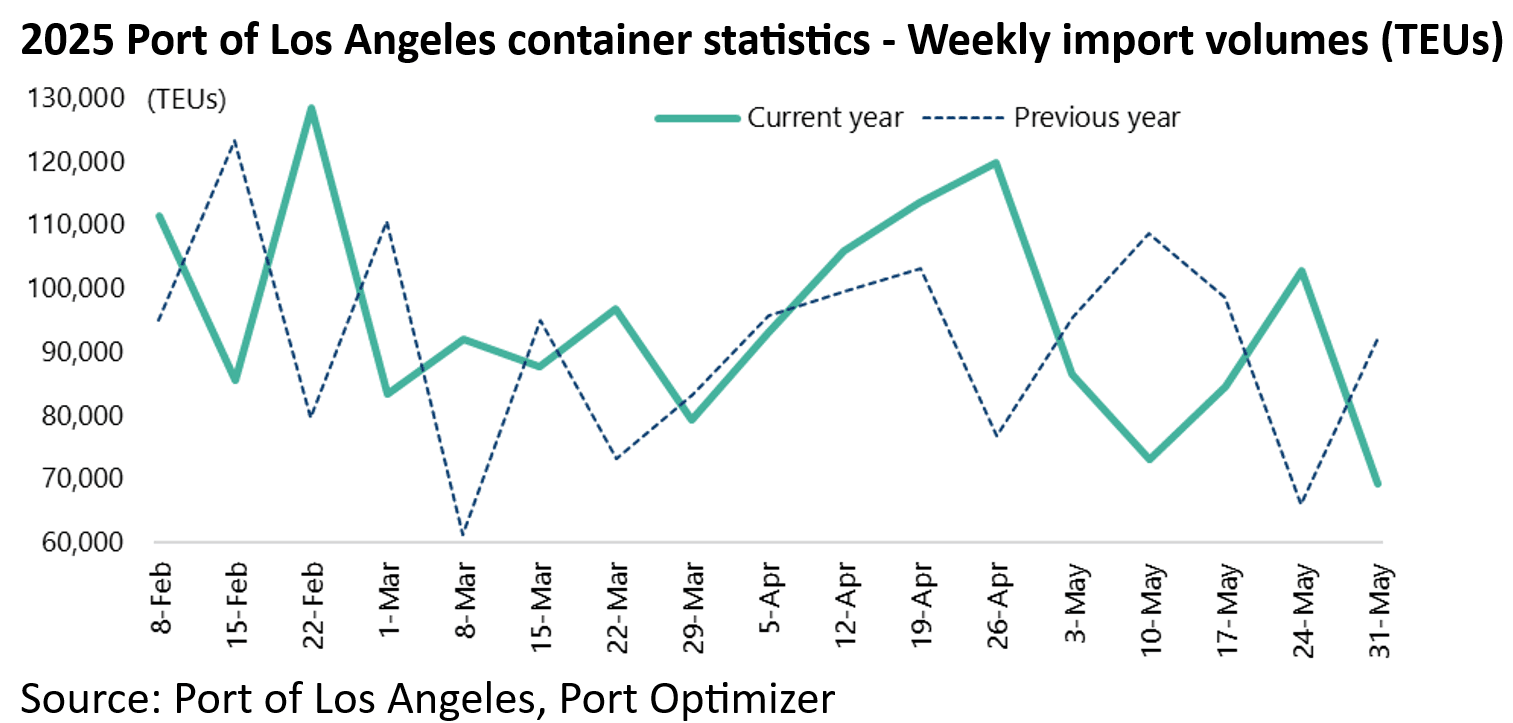

Data from the Port of Los Angeles also shows that import volumes to the port declined by 25% YoY to 69,260 TEUs in the week ended 31 May and were down 42% from 119,793 TEUs in the week ended 26 April.

Meanwhile, China continues to convey the message that it believes in free trade and globalisation.

This writer remains of the view that Beijing is unlikely to be panicked into aggressive stimulus which could destabilise its macro.

Rather, easing measures will remain only incremental.

In this respect, China has much more willingness to take pain than the US as regards the tariff issues and related trade war.

Still, the pressure would be much greater on Beijing if the US dollar was surging, whereas the opposite has been the case.

This means that the renminbi has depreciated against most of its trading partners.

Thus, the renminbi has appreciated by 1.4% against the US dollar year-to-date but has depreciated by 7.8% against the euro.

While the trade-weighted Renminbi index, which tracks the renminbi’s performance against a basket of 25 currencies, has declined by 5.4% year-to-date.