The Current State of the US Economy: Lower Rates and AI Angst

Author: Chris Wood

The Federal Reserve has remained on pause at last week’s FOMC meeting as regards interest rates which is only to be expected.

That said, the base case is that Fed easing resumes this year, most likely from the June meeting if not earlier.

Money markets are now expecting 70bp of Fed easing this year.

The American central bank has already responded to growing political pressure by announcing a slowdown in the pace of quantitative tightening at the FOMC meeting last week.

The pace of decline of its Treasury holdings will be slowed from US$25bn to US$5bn a month starting from April, while the monthly decline of its mortgage agency debt holdings will be maintained for now at US$35bn.

This move comes against the backdrop of tightening liquidity and slowing data even before the impact of the DOGE cuts kick in.

The latest monthly Challenger report shows that US companies announced 172,017 job cuts in February, the highest level since July 2020 and the highest job cuts for the month of February since 2009.

While, as noted here before on several occasions, the US M2 to nominal GDP ratio has broken below a 23-year trend line in the past six quarters having been 25.7% above that trend at the peak of the Covid triggered Fed monetary expansion in the second quarter of 2020.

Thus, the M2 to nominal GDP ratio fell to 0.722 or 4.9% below trend in 4Q24, based on the latest 4Q24 data released in late February.

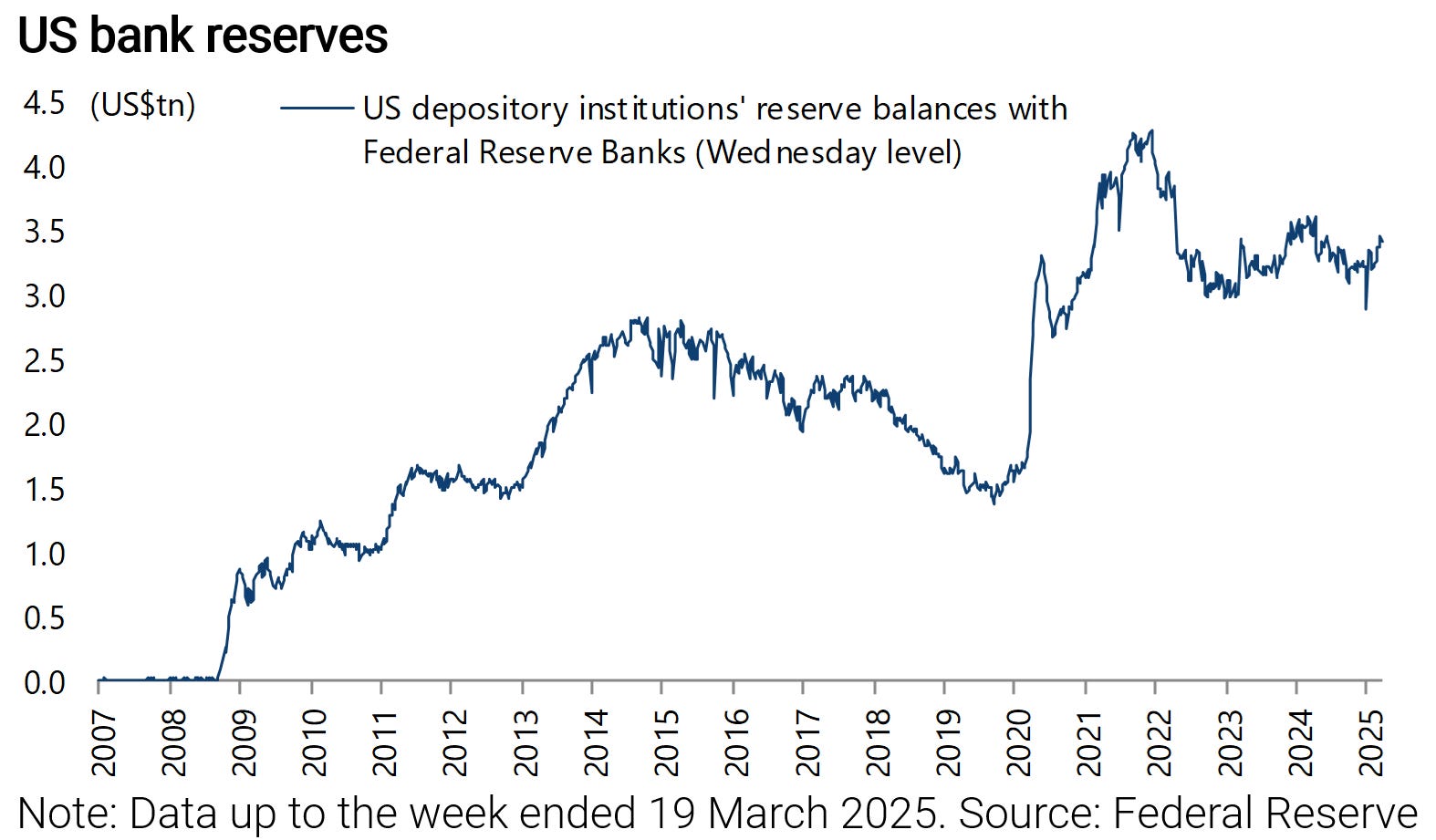

Meanwhile US bank reserves have declined from US$3.62tn in early March 2024 to US$3.43tn in the week ended 19 March 2025 and are down from a peak of US$4.27tn reached in December 2021.

Until the change of policy announced last week, the Fed has been reducing its balance sheet at a pace of US$60bn a month.

That has become more relevant given that Janet Yellen is no longer at the Treasury and the Fed’s repo facility has declined from US$2.375tn at the end of March 2023 to a recent low of only US$58.8bn on 14 February and is now US$201bn.

Bessent Will Likely Increase LT Treasury Issuance...Someday

As noted here before (see The Growing Risk of The Treasury’s Addiction to Short Term Debt, 11 September 2024), Yellen’s “activist Treasury bill issuance” probably had the practical effect of sterilizing the impact of quanto tightening last year.

With new Treasury Secretary Scott Bessent on record as having criticised Yellen’s increased reliance on short-term issuance of Treasuries, investors will have been on the lookout for any increase in longer-term Treasury issuance.

But so far that is not happening.

Indeed, Bessent has continued Yellen’s policy in terms of the reliance on short-term issuance.

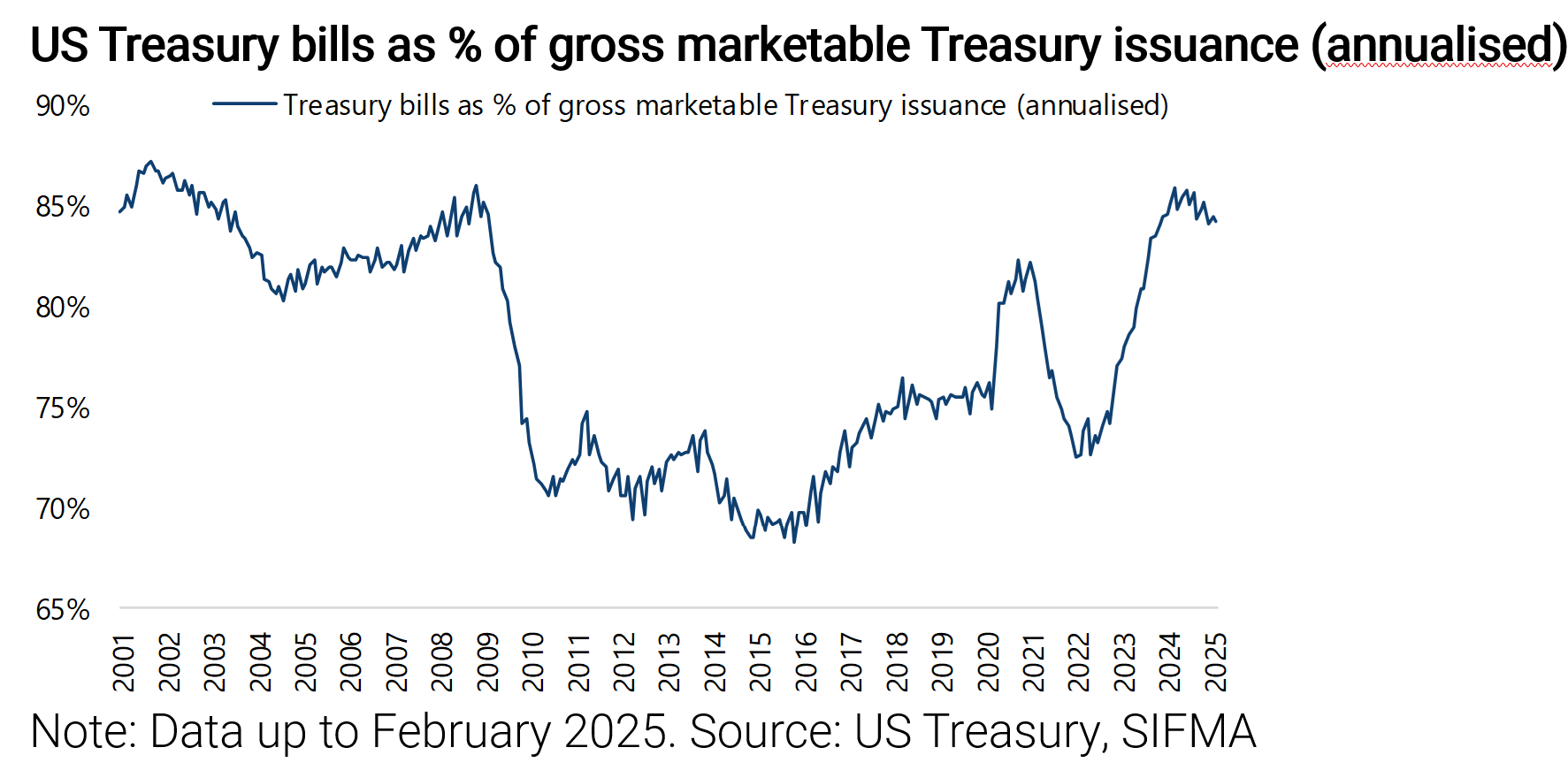

The Treasury announced in its quarterly refunding plan in early February no change in coupon auction sizes for the current quarter, and repeated its guidance that it intends to maintain the same auction size of notes and bonds for “at least the next several quarters”.

Treasury bills accounted for 82.6% of the total gross marketable Treasury issuances in February and an annualised 84.2% in the 12 months to February.

This is one, among several reasons, why the base case remains that long-term Treasuries are in a structural bear market as investors demand a term premium for lending money long-term to the federal government even if the consequence of the delayed impact of monetary tightening would normally be slower growth and falling inflation.

The biggest risk to this view is if Elon Musk succeeds in implementing his planned savings at DOGE since that will in the short-term trigger a deflationary shock for the American economy, however positive the longer-term impact.

The AI Narrative Will Continue to Drive the Stock Market

Returning to the stock market, the base case of this writer remains that the DeepSeek affair will prove to be the most important event in the US stock market since the announcement of Microsoft’s investment in ChatGPT-maker OpenAI in January 2023, which was the catalyst for the AI thematic to drive the most important sector, namely technology, in the world’s largest stock market in terms of the commencement of the AI capex arms.

The base case is also that the US effort to restrict China’s access to advance semiconductors will turn out to be completely counterproductive.

The DeepSeek news, combined with talk that a significant amount of Nivida’s banned HBM-based chips ended up in China last year via the second-hand market, is of the sort that will cause the national security types in Washington to want to come up with even tighter restrictions targeting China.

But Donald Trump will probably take a different view since from a “common sense” standpoint, a phrase beloved by the 47th president, he will understand that such controls are extremely difficult, if not impossible, to enforce.

Meanwhile it is undoubtedly the case that the cheaper the access to AI becomes, the more the demand for compute will grow.

But that does not mean that semiconductor stocks can immediately return to nirvana because of the little issue of pricing power, or the lack of it.

For now the four big hyperscalers are maintaining their capex based on what was guided in their latest earnings announcements in late January.

In fact they are increasing it.

In total the four are projecting capex at an enormous US$320bn this.

That is a huge amount of money by any standards and clearly has negative implications for their free cashflow generation.