The Consumer is Almost Tapped Out, What Comes Next?

This year began with growing optimism that emerging markets can decouple in a year which may bring a US recession.

There is a related optimism that commodities can decouple from a forecast US downturn, a point highlighted by the rise in the copper price.

The copper price has risen by 11% since 4 January and is up 31% from the low reached last July.

Copper price

Source: Bloomberg

This optimism has been triggered at the margin by China’s dramatic U-turn on Covid which, as discussed here previously (Why 2% Inflation Is Right Around The Corner, 10 January 2023), creates the best chance in many years for sustained Asia and emerging market outperformance.

Indeed this writer remains strongly of the view that, if it were not for China’s aggressive enforcement of Covid suppression last year, Asia and emerging markets would have already outperformed significantly in 2022.

MSCI Emerging Markets and Asia ex-Japan relative to S&P500

Source: Bloomberg

Base Effect's Muting Effect on Inflation Now in Doubt

Meanwhile, the latest US CPI data point has somewhat undermined the positive base effect for CPI that investors were looking at the start of this year.

US headline CPI rose by 0.5% MoM in January, in line with consensus expectations.

Still the MoM increases in CPI in the last three months of 2022 have been revised up as a result of the recalculation of seasonal adjustment factors for the past five years.

Thus, US CPI was up 0.1% MoM in December rather than a 0.1% decline previously reported, while the increases in October and November have been revised up from 0.4% and 0.1% MoM respectively to 0.5% and 0.2%.

This has rather undermined the benign base effect dynamic investors have been focused on.

US CPI %MoM revision

Note: Seasonally adjusted. Source: Bureau of Labor Statistics

As for the year-on-year changes, headline and core CPI inflation slowed only from 6.5% YoY and 5.7% YoY respectively in December to 6.4% YoY and 5.6% YoY in January, compared with consensus expectations of 6.2% YoY and 5.5% YoY.

US headline and core CPI inflation

Source: Bureau of Labor Statistics

Core goods CPI declined further from 2.1% YoY in December to 1.4% YoY in January, the lowest level since February 2021. By contrast, core services inflation rose from 7.0% YoY in December to 7.2% YoY in January, the highest level since August 1982.

US core goods and core services inflation

Source: Bureau of Labor Statistics

While 15 of the 36 main categories of CPI saw YoY inflation accelerate in January compared with 18 in December.

The recent adjustments of the CPI weightings have also made the shelter component, which essentially measures rents, even more important.

The weighting for shelter in the CPI has been revised up from 33.273% to 34.413%.

On this point, the shelter component of the CPI rose by 7.9% YoY in January, up from 7.5% YoY in December.

US CPI shelter inflation

Source: Bureau of Labor Statistics

As for the Cleveland Fed’s trimmed-mean CPI inflation measure, it declined marginally from 6.58% YoY in December to 6.55% YoY in January.

Cleveland Fed trimmed-mean CPI and median CPI inflation

Source: Federal Reserve Bank of Cleveland

Remember that this measure excludes the CPI inflation components each month which have shown the most extreme moves in either an upward or downward direction.

While, perhaps more interestingly, Cleveland Fed’s median CPI inflation rose from 6.99% YoY in December to 7.08% YoY in January, the highest level since the data series began in December 1983.

Future Rate Expectations Moved Significantly in February

The above data, and the news that the Fed’s most articulate dove, Lael Brainard, will take up a new post as director of the National Economic Council, the top economic advisor to President Biden, has, combined with January’s strong employment data, caused a significant reassessment of tightening expectations.

The terminal rate is now projected by the money markets at 5.29% (against the current Fed funds effective rate of 4.58%), up from 4.89% on 1 February.

Fed funds futures implied rate for July 2023 FOMC meeting

Source: Bloomberg

Still it also should be noted that in the latest job report average hourly earnings growth continued to decline.

US average hourly earnings growth for private employees slowed from 4.8% YoY in December to 4.4% YoY in January, the lowest level since August 2021, while average hourly earnings growth for private production and nonsupervisory workers declined from 5.3% YoY to 5.1% YoY, the lowest level since July 2021.

US average hourly earnings growth

Source: Bureau of Labor Statistics

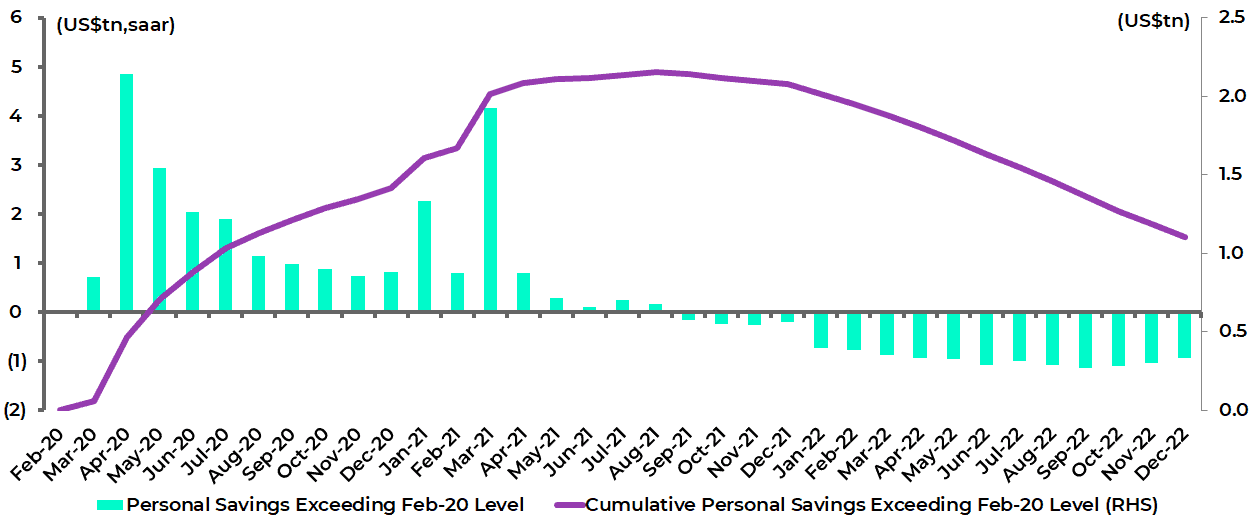

When Will COVID Payments Run Out?

Meanwhile, while expectations of a US recession this year are now being questioned, one risk to the American economy remains the ongoing trend where US consumers are incrementally spending the transfer payments they received during the pandemic.

There are different ways to calculate the so-called excess personal savings.

This writer’s methodology has been simply to calculate the gap between actual monthly personal savings during the pandemic and the pre-pandemic level of annualised US$1.581tn in February 2020.

Based on this measure, cumulative excess savings since March 2020 at the onset of the pandemic peaked at US$2.152tn in August 2021 and have since declined by US$1.046tn or 49% to US$1.106tn in December.

US cumulative excess savings

Source: Bureau of Economic Analysis

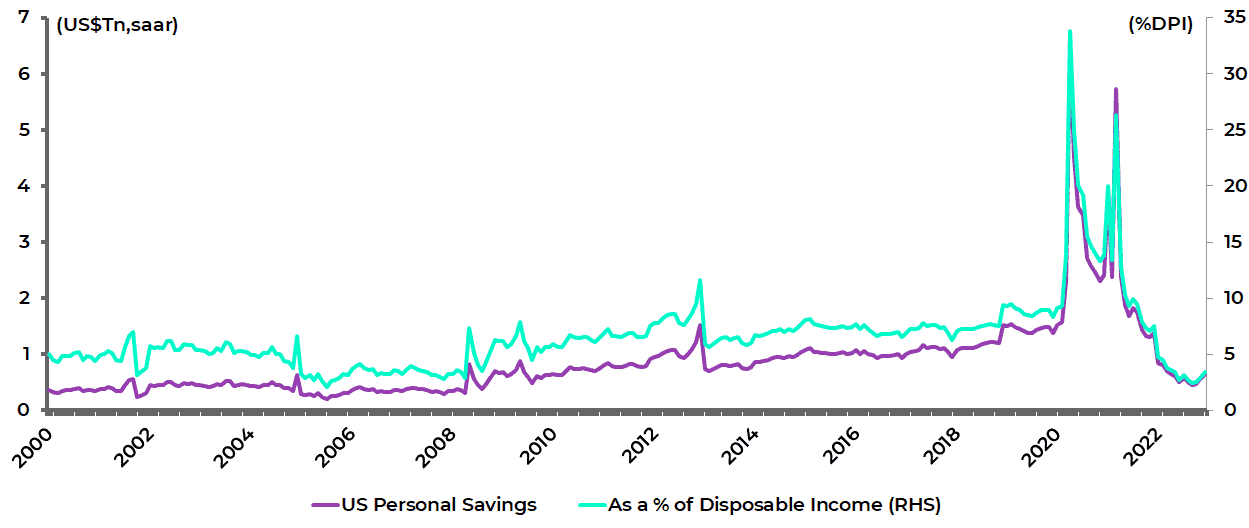

As for the monthly personal savings rate, it fell from 9.5% of disposable income in August 2021 to 2.4% in September 2022, the lowest level since July 2005, though it has since risen to 3.4% in December.

US personal savings

Source: Bureau of Economic Analysis[/caption]

If the savings rate stays at its 4Q22 level of an average 2.9%, the stock of excess savings will continue to decline at a rate of roughly US$85bn a month, which means that the “excess savings” will be completely depleted by January 2024.

At that point, the risk becomes that the savings rate returns to its historical pre-pandemic trend, which is in the 7-8% range.

The annual savings rate ranged from 7.0-8.8% in the period between 2014 and 2019.

Another point is that, while 49% of the excess savings American consumers accumulated during the pandemic has been spent, much of the remaining US$1.106tn is offset by the rise in auto loans and unpaid credit card balances.

Households’ credit card balances have risen by US$216bn or 28% from the recent low of US$770bn in 1Q21 to US$986bn in 4Q22, while auto loan balances have risen by US$170bn or 12% to US$1.552tn over the same period, according to the New York Fed’s quarterly Household Debt and Credit report.

US households’ auto loans and credit card balances

Source: Federal Reserve Bank of New York – Household Debt and Credit report

All this is why the risks in America as regards consumption patterns would seem to be to the downside, just as they are massively to the upside in China as Chinese savers build savings during last year’s lockdowns.

China household deposits surged by 17.3% YoY in January and are up an enormous Rmb41tn (US$6tn) or 48% since January 2020.

China household bank deposits

Source: PBOC