The Chinese Property Crash Rolls On. When Will the Bounce Come?

Too little too late...

Author: Chris Wood

The pace of property easing in China accelerated last quarter to its most intense level yet, with the central government announcing in May details of a previously floated scheme to encourage local governments to buy unsold properties from developers to convert into affordable housing.

Still there remains, crucially, a lack of clarity on exactly how this process will work in terms of the prices to be paid by local governments, via local state-owned enterprises.

For the record, Vice Premier He Lifeng said on 17 May in the formal announcement of the policy that local governments can purchase some of the unsold housing inventory “at a reasonable price” and turn it into affordable housing.

They can also buy back “idle stockpiles of residential land” to ease the financial burden on distressed developers.

He also acknowledged that real estate is related to “the vital interests of the people and the overall situation of economic and social development”.

The other notable feature of the PBOC announcement was that the national minimum downpayment ratio was reduced to 15% for first-time buyers and 25% for second homes, down from 20% and 30% respectively.

The minimum mortgage rate was also effectively scrapped. It was previously set at 20bp below the five-year loan prime rate (LPR, currently 3.95%) for first homes and 20bp above the LPR for second homes.

It is also the case that many cities have abolished anti-speculation measures.

For example, Beijing ended a curb on multiple home purchases in the city’s non-core areas at the end of April.

Shenzhen announced in May that it will allow local families with two or more young children to buy another home in some non-core districts.

It has also loosened personal income tax and social insurance payment requirements for non-local home buyers in certain districts.

In view of all of the above, it can be said that policy towards the residential property market is now at its most stimulatory yet in China.

This is a clear signal that the central government wants to stimulate demand, amounting to an almost full-scale retreat from the previously favoured slogan that “housing is for living in, not for speculation” (房子是用来住的,不是用来炒的).

That slogan was removed from the official statement following the Politburo meeting last July.

It is also the case that the focus on asking local governments to buy unsold units does for the first time address the excess supply issue.

This is good from a signalling standpoint even if the key point as regards how the properties will be valued remains opaque.

That signalling effect, and growing anticipation of accelerating easing, triggered a rally in China property stocks, albeit in the case of the private sector developers from extremely bombed out levels.

Still that rally has now almost completely unwound in terms of a renewed decline in share prices.

The MSCI China Real Estate Index and the MSCI China were up 46% and 20% respectively from their mid-April low to their mid-May high and have since declined by 20% and 7%.

Easing Measures Too Little Too Late So Far...

The reality remains that these easing measures would have had a far greater impact if they had been announced one year ago.

Remember the recovery in residential property in China stalled in April last year after a surprisingly strong upturn in the first quarter of 2023, driven by pent-up upgrading demand coming out of the pandemic and related lockdown.

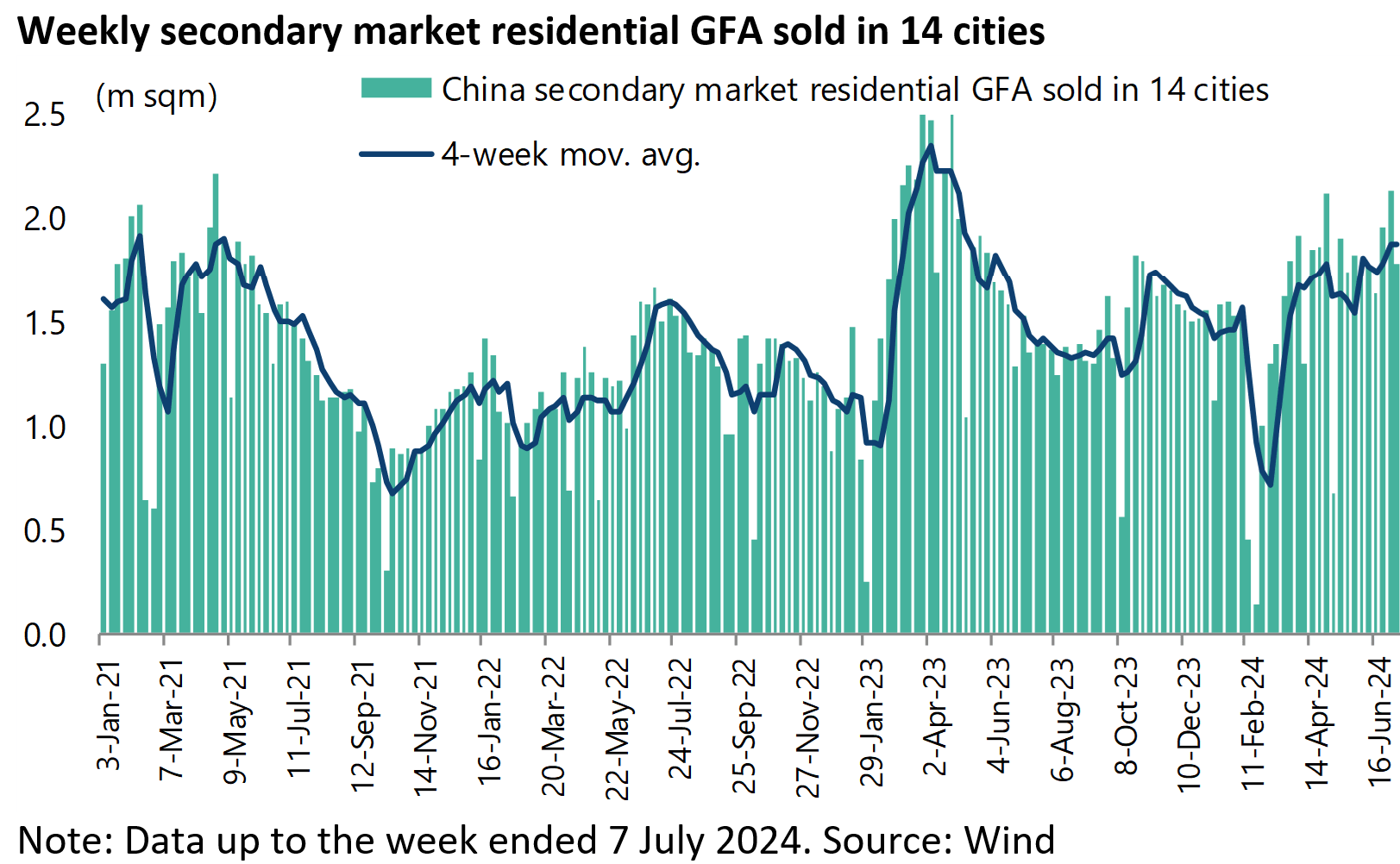

It also remains the case that activity has continued to move from the primary market to the secondary market, reflecting the continuing failure of the central government to restore confidence on the issue of uncompleted projects of financially extended developers.

Meanwhile, the timing of the latest property announcement was explained by the continuing negative property data.

Activity remains depressed, particularly in the primary market.

National residential property sales have declined by 21.9% YoY in floor space terms, and by 26.9% YoY in value terms in the first six months of 2024, implying an estimated decline of 15.7% YoY in volume terms and 13% YoY in value terms in June alone.

Meanwhile, weekly primary residential floor space sales in 30 major cities still declined by 13% YoY in the four weeks to 7 July.

As for the increasingly active secondary market, secondary residential floor space sales in 14 major cities rose by 31% YoY in the four weeks to 7 July and are down 10% year-to-date, though they are up 31% from the same period in 2022.

Deflation Forces Continue to Weigh on the Economy

Meanwhile, the overall macro deflationary trend remains intact in terms of nominal GDP growth in China remaining below real GDP growth.

China nominal GDP rose by 4.0% YoY in 2Q24 while real GDP increased by 4.7% YoY, though down from 4.2% YoY and 5.3% YoY, respectively, in 1Q24.

Nominal GDP growth has been below real GDP growth for five consecutive quarters for the first time since 1999.

This also continues to be reflected in market action in terms of dividend stocks continuing to outperform and the 10-year government bond yield trading at near all-time lows.

The CSI 300 Dividend Index has outperformed the CSI 300 by 11.5% year-to-date on a total-return basis and by 26.5% since the start of 2023.

Meanwhile, the China 10-year government bond yield declined to 2.206% at the end of June, the lowest level since April 2002, and is now 2.26%.

Exports and Trade Surplus the Only Silver Lining

If domestic demand remains in the doldrums, the positive side of China’s economy remains its exports and a resulting trading surplus.

China exports increased by 3.6% YoY in US dollar terms to US$1.71tn in the first six months of 2024 and were up 8.6% YoY in June.

China’s trade surplus in manufactured goods is currently running at US$1.75tn a year, compared with an average of US$925bn a year in the five years to 2019 prior to the pandemic, while its overall trade surplus reached an all-time high of US$838bn in 2022 and is currently running at an annualised US$858bn, up from an average of US$459bn a year in the five years to 2019.