So You Think Globalization is Over? China Has Other Ideas

Author: Chris Wood

Donald Trump’s agenda may be all about attacking globalization.

But China has continued to take the opposite line.

Xi Jinping’s public comments continue to emphasise the case for multilateralism and for the need to enhance the authority and effectiveness of the multilateral trading system with the World Trade Organization at its core.

The contrast with the American president’s continuing penchant for bilateral trade deals could not be more stark.

In this respect, the meeting between Xi and Trump in South Korea last October on the sidelines of the Asia-Pacific Economic Cooperation (APEC) Forum also saw the first-ever leaders’ meeting of the Regional Comprehensive Economic Partnership (RCEP), a grouping which has ASEAN at its core but also includes China, Japan, South Korea, Australia and New Zealand.

This is the world’s largest free trade agreement but the US is not part of it.

Indeed, reflecting Trump’s lack of interest in multilateral affairs, the American president left Korea following his meeting with Xi before other leaders of the 21-member APEC forum began discussions on the core issue of the meeting, namely trade and investment across the Asia Pacific.

If Xi continues to emphasise the case for multilateralism and globalisation, Trump’s “America First” agenda is all about unilateralism.

Indeed the American president ordered in February last year a comprehensive review of US engagement in all multilateral organisations, the findings of which were meant to be delivered in August but nothing has been announced until of late.

Thus, Trump signed a presidential memorandum on 7 January ordering the withdrawal of the US from 66 international organisations that “no longer serve American interests” based on findings from the review, including 31 United Nations (UN) entities and 35 non-UN organisations. While a review of additional international organizations remains ongoing.

How the US is Dealing with Transshipments From China

Meanwhile, tariff discussions also remain ongoing with many Asian countries, including the issue of how the US is going to address “transshipments”, namely Chinese goods shipped via third-party countries.

Washington has previously threatened a 40% tariff on “transshipped” goods.

But so far nothing has happened on this point with most of Asia hoping the American president has forgotten about it.

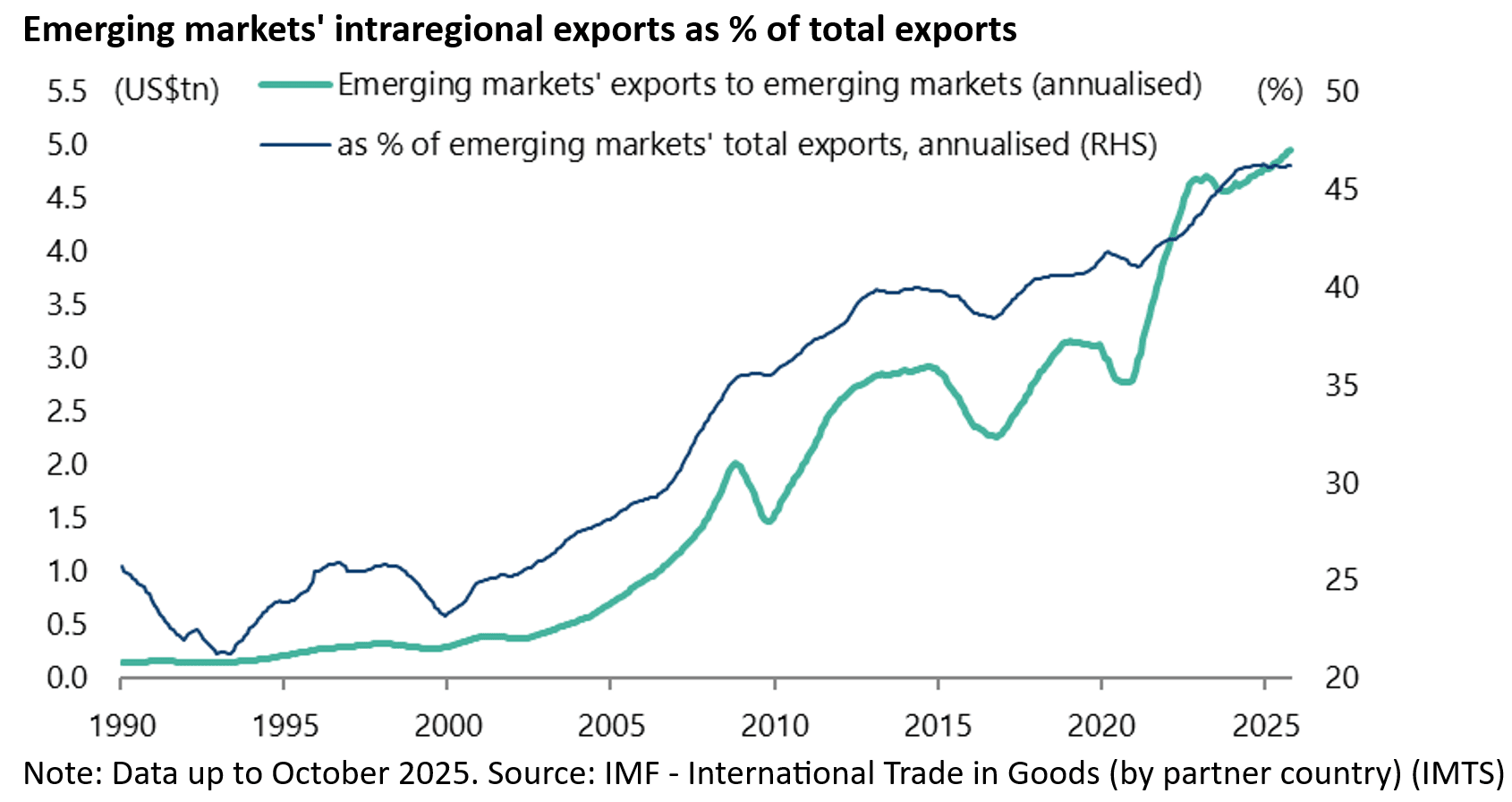

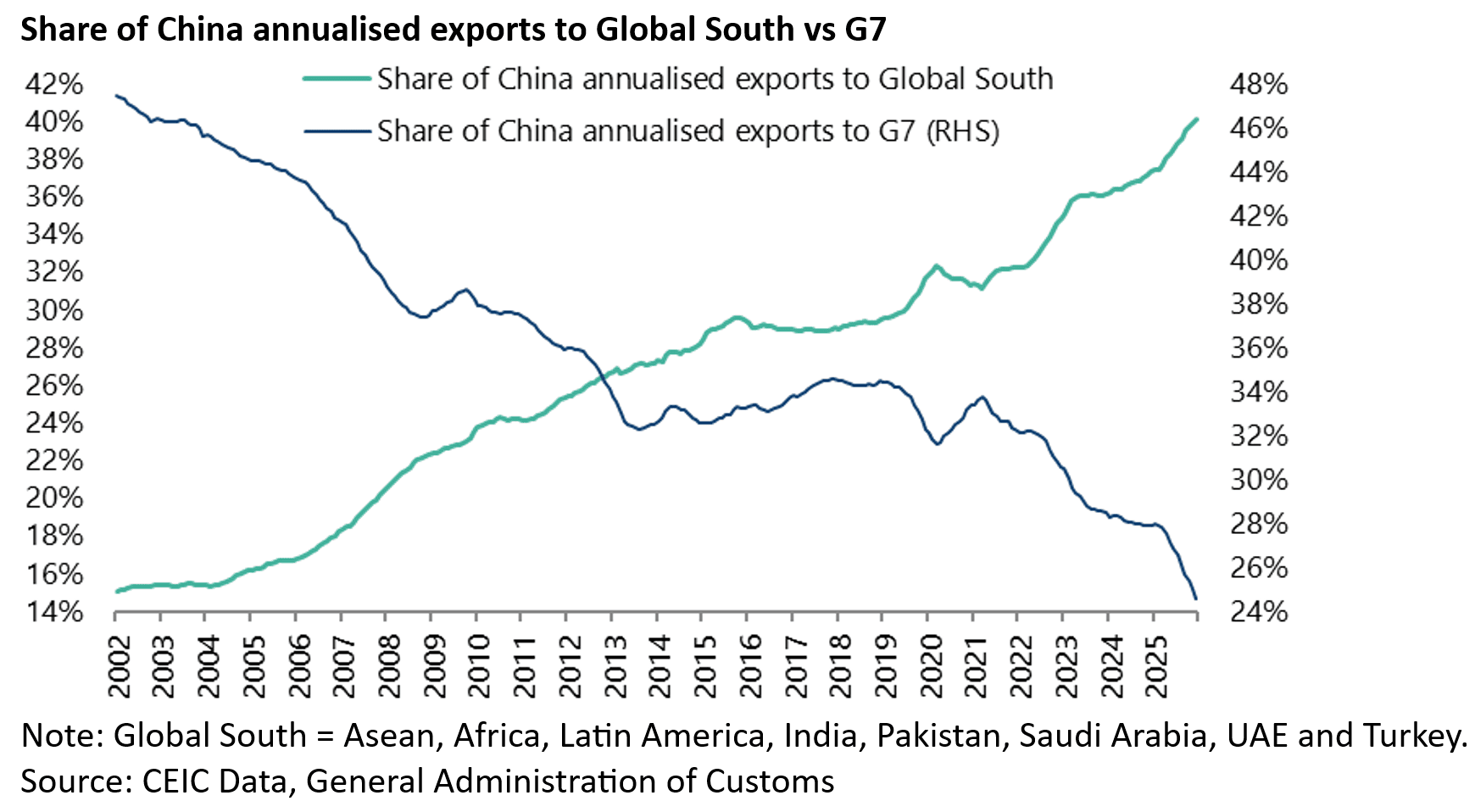

If this is the negative backdrop in terms of the Washington retreat from globalisation in the context of the highest tariffs imposed since 1934, the reality is also that intra-emerging markets trade continues to rise while China’s exports to the Global South also continue to grow relative to its exports to the G7.

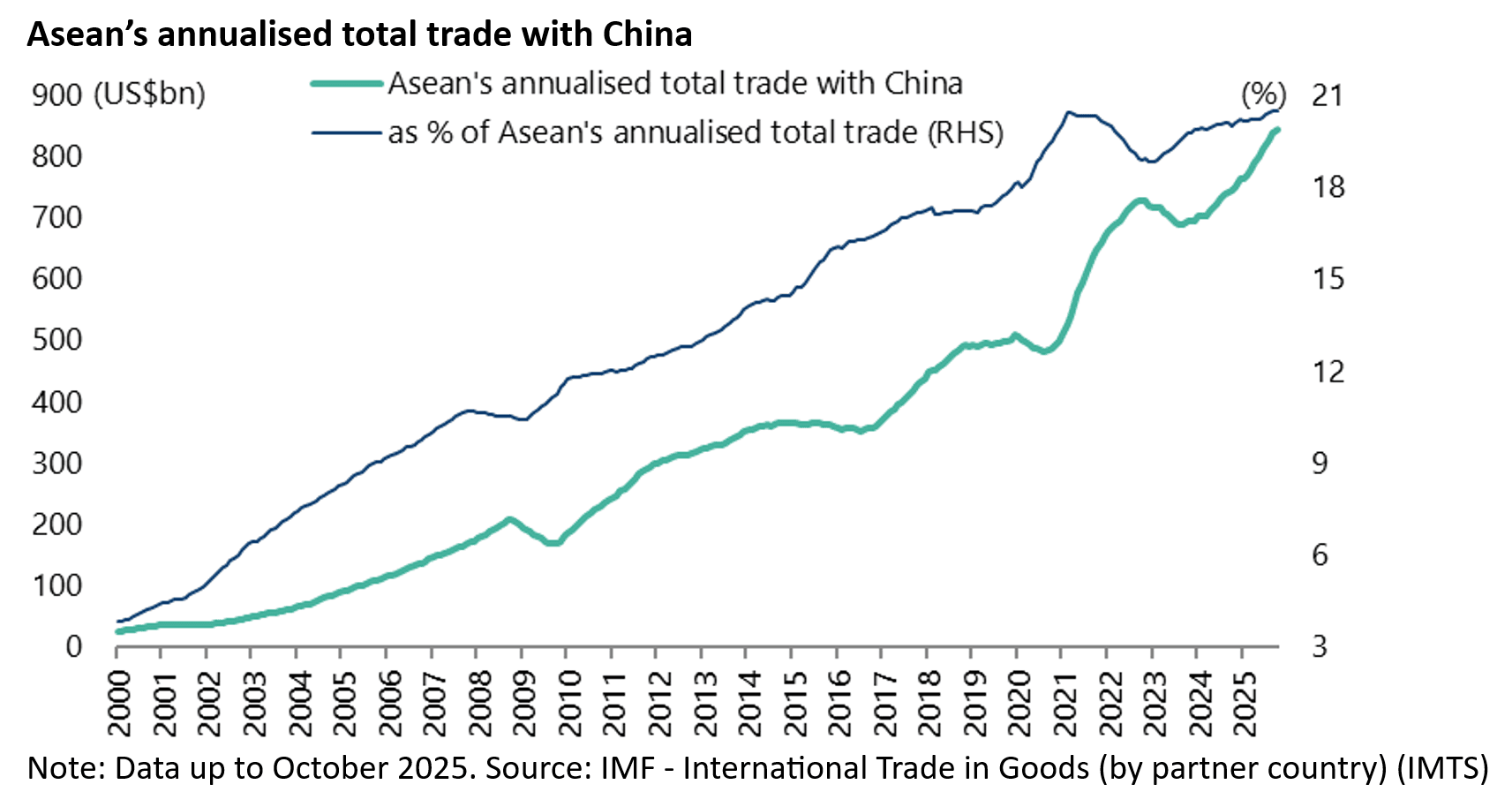

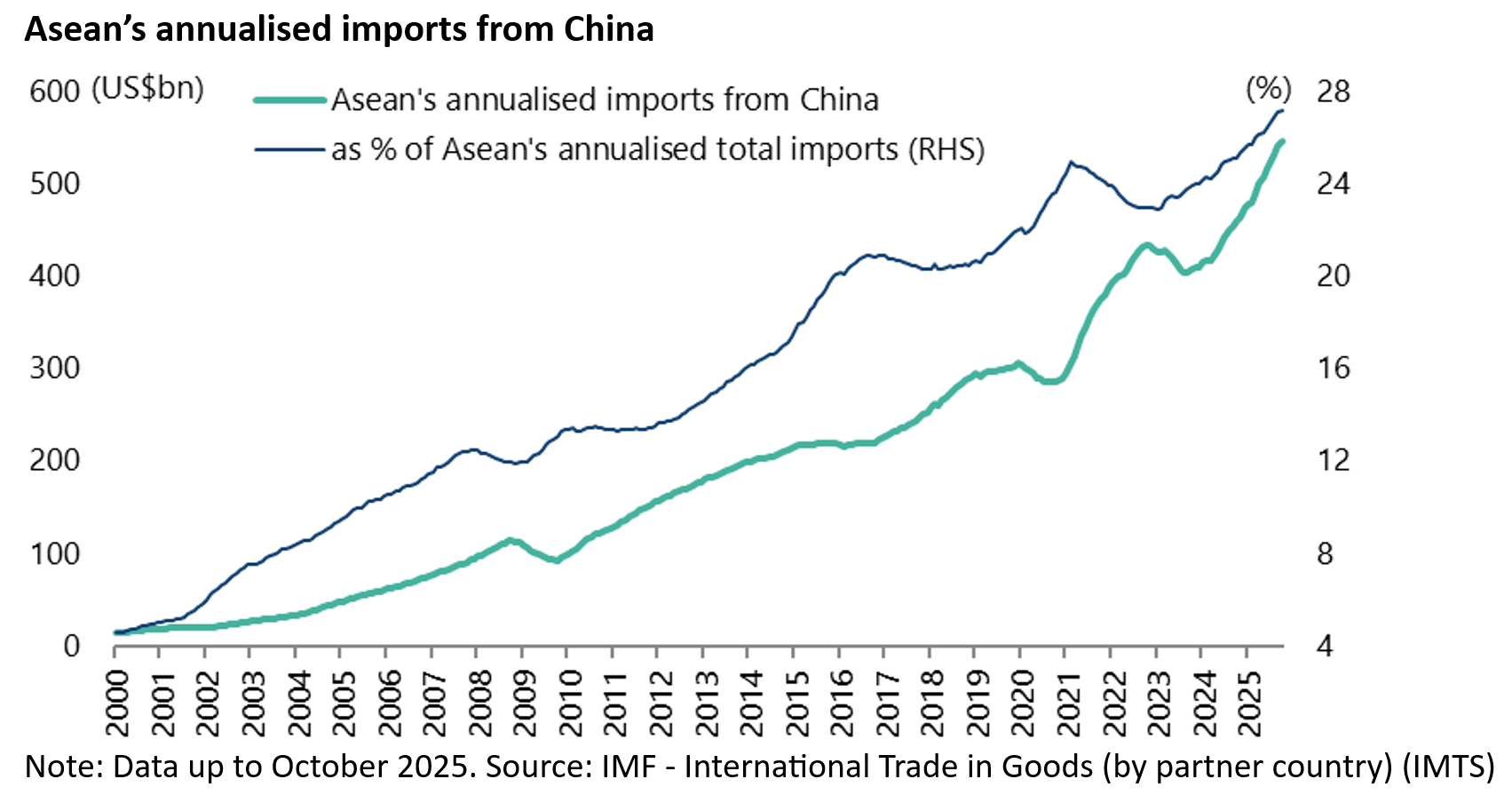

Meanwhile, in an Asian context, China has been Asean’s largest trading partner since 2009.

In this sense, globalisation is far from over. The numbers are worth spelling out.

Emerging markets’ exports to other emerging markets rose to an annualised US$4.96tn in the 12 months to October 2025, accounting for 46.2% of emerging markets’ total exports, up from US$292bn or 23.2% of total exports in 1999.

While China’s annualised exports to the Global South have increased from US$772bn in June 2020 to US$1.514tn in December 2025.

By contrast, China’s annualised exports to the G7 have declined from US$1.161tn in August 2022 to US$928bn in December 2025.

As a result, China’s exports to the Global South now amount to 40.1% of its annualised total exports, up from 21% at the beginning of 2008, while the share of exports to the G7 has declined from 39% to 24.6% over the same period.

Similarly, Asean’s trade with China has risen from US$179bn or 11.6% of Asean’s total trade in 2009 to US$845bn or 20.5% of its total trade in the 12 months to October 2025.

In this respect, China could be said to be filling the vacuum left by Trump’s bilateral focus.

Meanwhile, from an Asean perspective, there continues to be remarkably little pushback in terms of the negative impact on domestic businesses of the continuing flood of Chinese imports into these countries.

Asean’s imports from China have risen from US$97bn or 13.3% of total imports in 2009 to US$545bn or 27.1% of total imports in the 12 months to October.

In the Stablecoin Game the Dollar Now Has some Competition

Changing subject but on a related theme, Stablecoins have clearly been identified by the Trump administration as one way of creating short-term demand for Treasury bills to fund America’s fiscal deficit, as previously discussed here (see An Exploration of Trump’s View on Crypto, Short Term Treasuries and Yield Curve Control, 11 September 2025).

But there is nothing that says stablecoins have to be US dollar based.

On that point, Hong Kong passed stablecoin legislation in May 2025 with the Stablecoins Ordinance taking effect on 1 August. The idea from a mainland perspective is that Hong Kong should be used as a pilot scheme, or “sandbox”, to experiment with stablecoins, with the plan to allow a small number of issuers to issue digital tokens pegged most likely to the Hong Kong dollar.

Hong Kong is a perfect environment for such an experiment since it is outside the mainland’s capital controls.

Indeed this is one of Hong Kong’s core “raison d’etre” as has also been demonstrated by the success of the Hong Kong Stock and Bond Connects which have now been in operation for 11 and eight years, respectively.

Still if the idea to experiment with a new financial technology makes sense, it is also a reality that stablecoins are a potential threat to the mainland’s ability to control its closed capital account.

This is why stablecoins remain banned in mainland China.

For similar reasons there is also a ban on trading cryptocurrencies in China which has been in place since 2021.

In June last year PBOC Governor Pan Gongsheng noted in a speech that digital tokens “posed great challenges to financial regulation” (see “Keynote Speech by PBOC Governor Pan Gongsheng at the 2025 Lujiazui Forum: A Few Observations on Global Financial Governance”, 18 June 2025); though he also acknowledged that “central bank digital currencies and stablecoins are thriving, making possible the simultaneous processing of payment and settlement”.

If the risks are clear, given that loss of control of the capital account is the ultimate nightmare for the PRC, it is also the case that the mainland authorities understand that it is unwise to shun outright a developing technology which has the potential at least to transform finance, not least in terms of the way international payments are handled.

There is also the point that currently about 99% of stablecoins are US dollar backed which further supports the US dollar’s global dominance.

For such reasons, it is both risky and unwise for Beijing to ignore the technology altogether, just as Beijing has experimented with internationalization of the renminbi in recent years even as it has maintained control of the capital account.

Still the practical problems represented by stablecoins, and the mainland authorities’ extreme cautions as regards this area, are reflected in a recent decision to delay the implementation of Chinese tech giants’ stablecoin issuance plans in Hong Kong.

Thus, the PBOC reportedly summoned in October a number of mainland firms under its jurisdiction, including banks and non-bank payment service providers, asking them to wait for its instructions before moving forward with their stablecoin initiatives in Hong Kong (see South China Morning Post article: “China’s pause on stablecoin projects will not dampen Hong Kong’s crypto push, experts say”, 25 October 2025).

The Chinese government also announced on 6 February rules barring individuals and businesses from issuing stablecoins linked to the renminbi overseas without regulatory approval (see Nikkei Asia article: “China bans unapproved issuance of yuan-linked stablecoins overseas”, 7 February 2026).

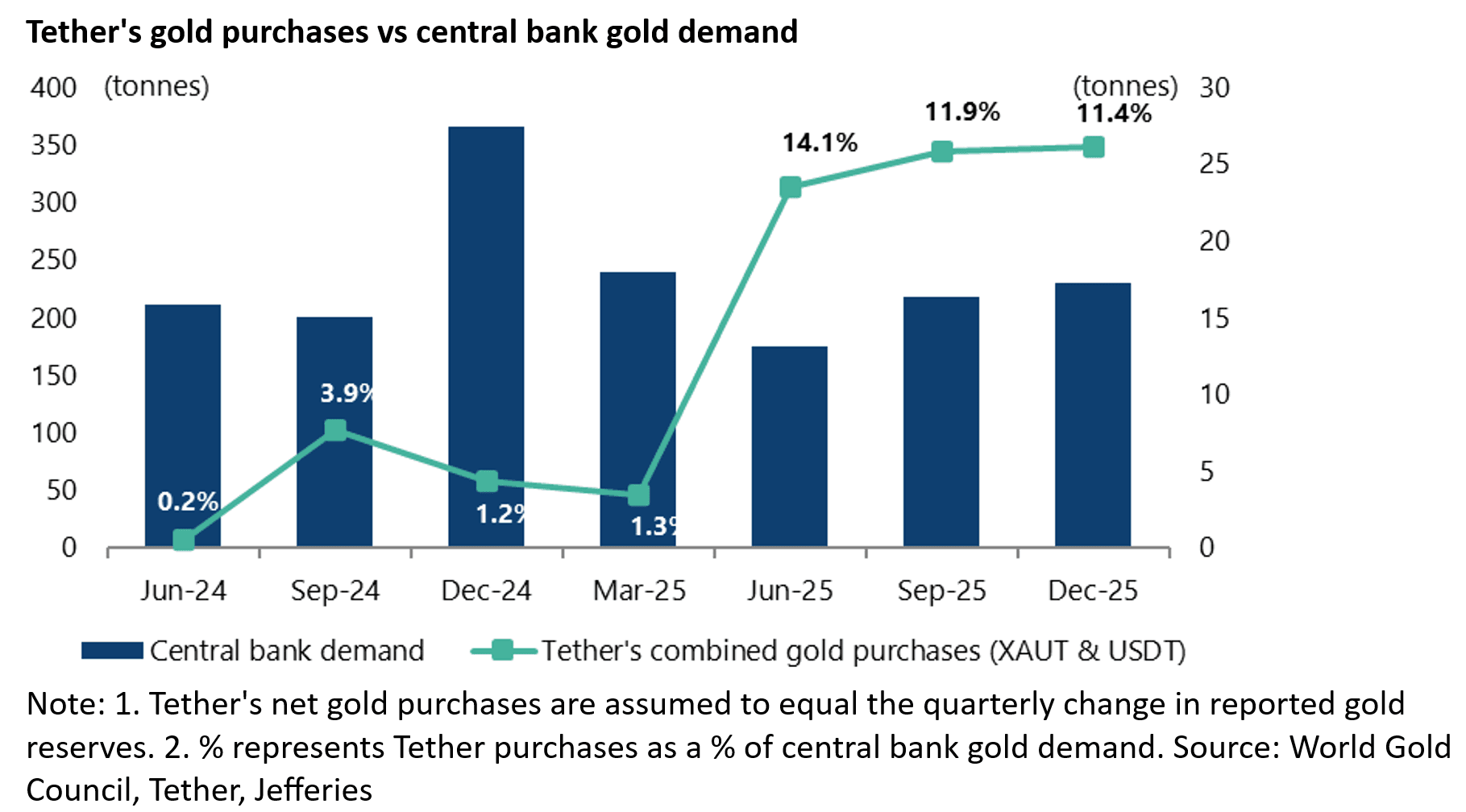

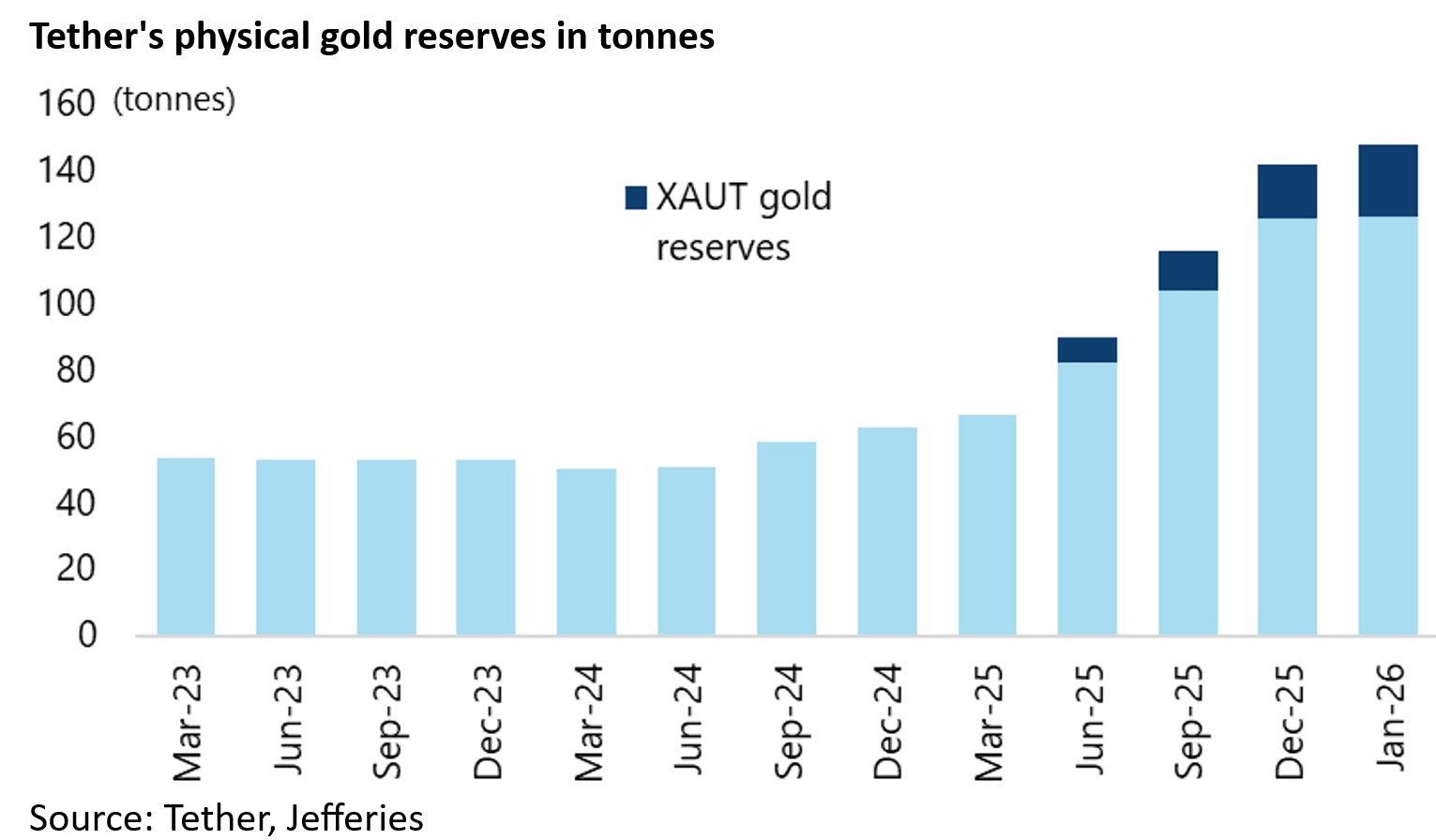

Meanwhile, it is interesting to note that the biggest issuer of stablecoins globally, Tether, has been a major buyer of gold in recent months.

Indeed Tether is the largest non-sovereign buyer of physical gold globally.

Its physical gold holdings rose to 142 tonnes worth US$19.7bn at the end of last year and an estimated 148 tonnes valued at US$23.3bn at the end of January, after purchasing 26 tonnes in 4Q25 and a further 6 tonnes in January.

Interestingly, these purchases exceeded the quarterly additions of most central banks ranking only third behind Poland and Brazil last quarter.

It is also the case that tether’s gold purchases of 26 tonnes in 4Q25 were equivalent to 11.4% of total central bank gold demand of 230 tonnes last quarter.

So, Tether has seemingly been one of the main drivers of gold’s rally in recent months.