Private Credit - This Cycles Systemic Risk

Author: Chris Wood

The Iran war is in the headline for entirely understandable reason. But AI remains the other key story for the US stock market.

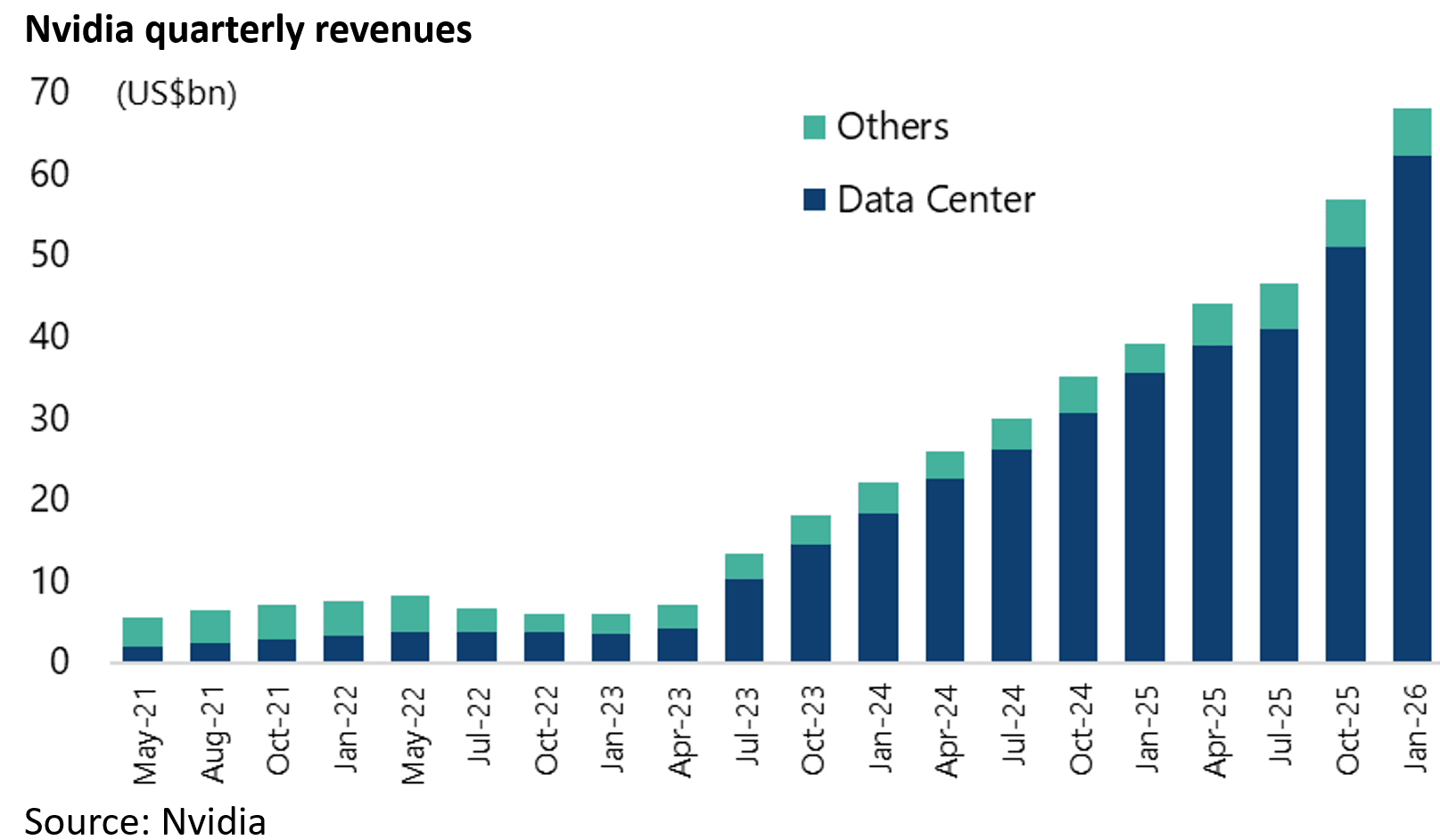

The latest Nvidia results confirm that AI capex remains strong.

This is no surprise based on recent hyperscaler guidance. Nvidia quarterly revenue rose by 20% QoQ and 73% YoY to a record US$68.1bn in the three months ended 25 January, with data center revenues up 22% QoQ and 75% YoY to US$62.3bn.

Still the key point remains if markets start to focus more on how the investors in AI capex are going to make the returns to justify this enormous spending.

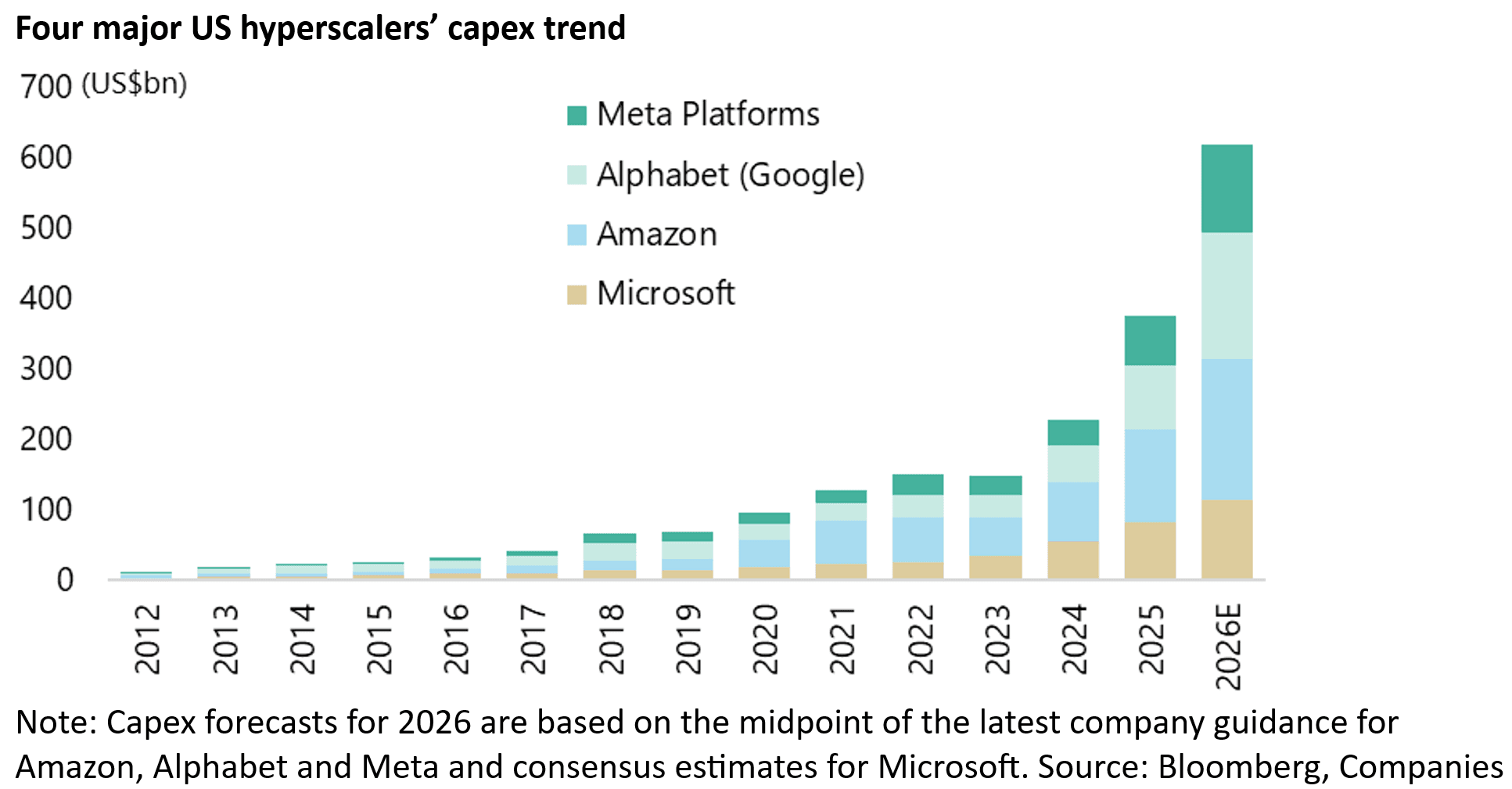

Remember that the four major US hyperscalers’ capex is projected to grow by a further 65% to an enormous US$620bn this year based on latest company guidance.

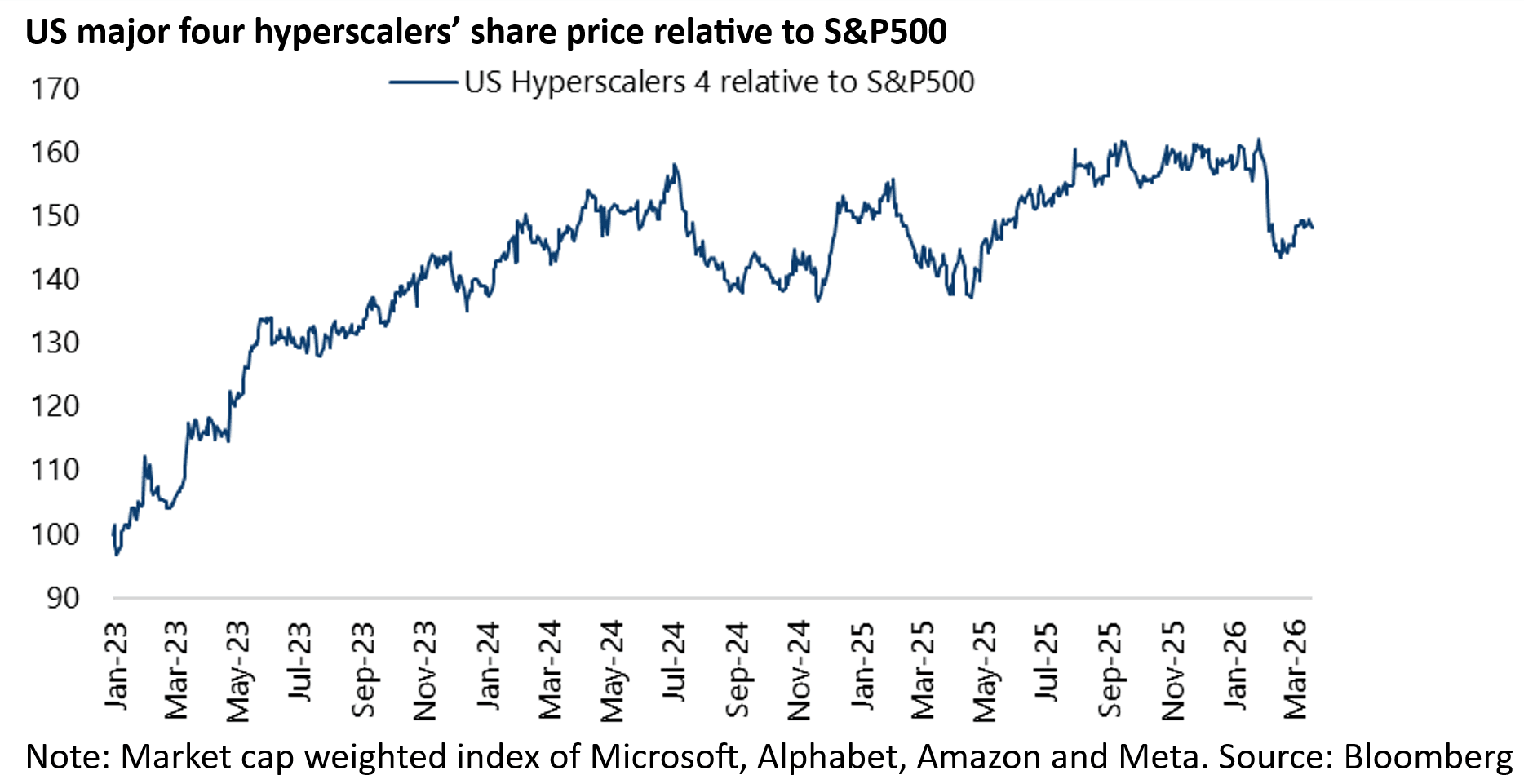

This questioning began with the 4Q25 results announced this quarter, with the shares of the four major hyperscalers underperforming the S&P500 by 7.1% so far this year.

This is why the base case of this writer is that the AI picks and shovels trade in the Western World has seen its best days in terms of the gains to be made in these stocks, most particularly in terms of relative outperformance.

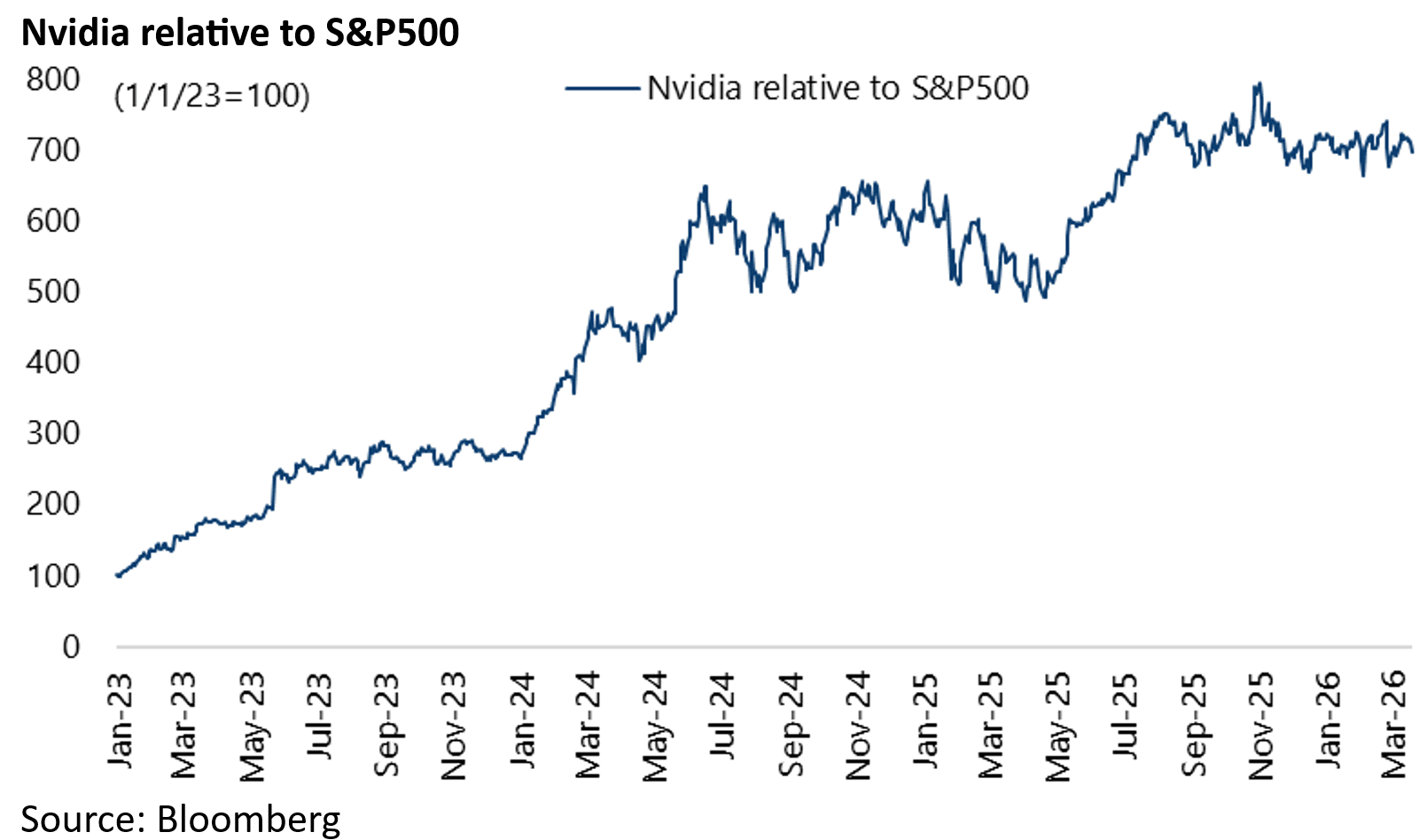

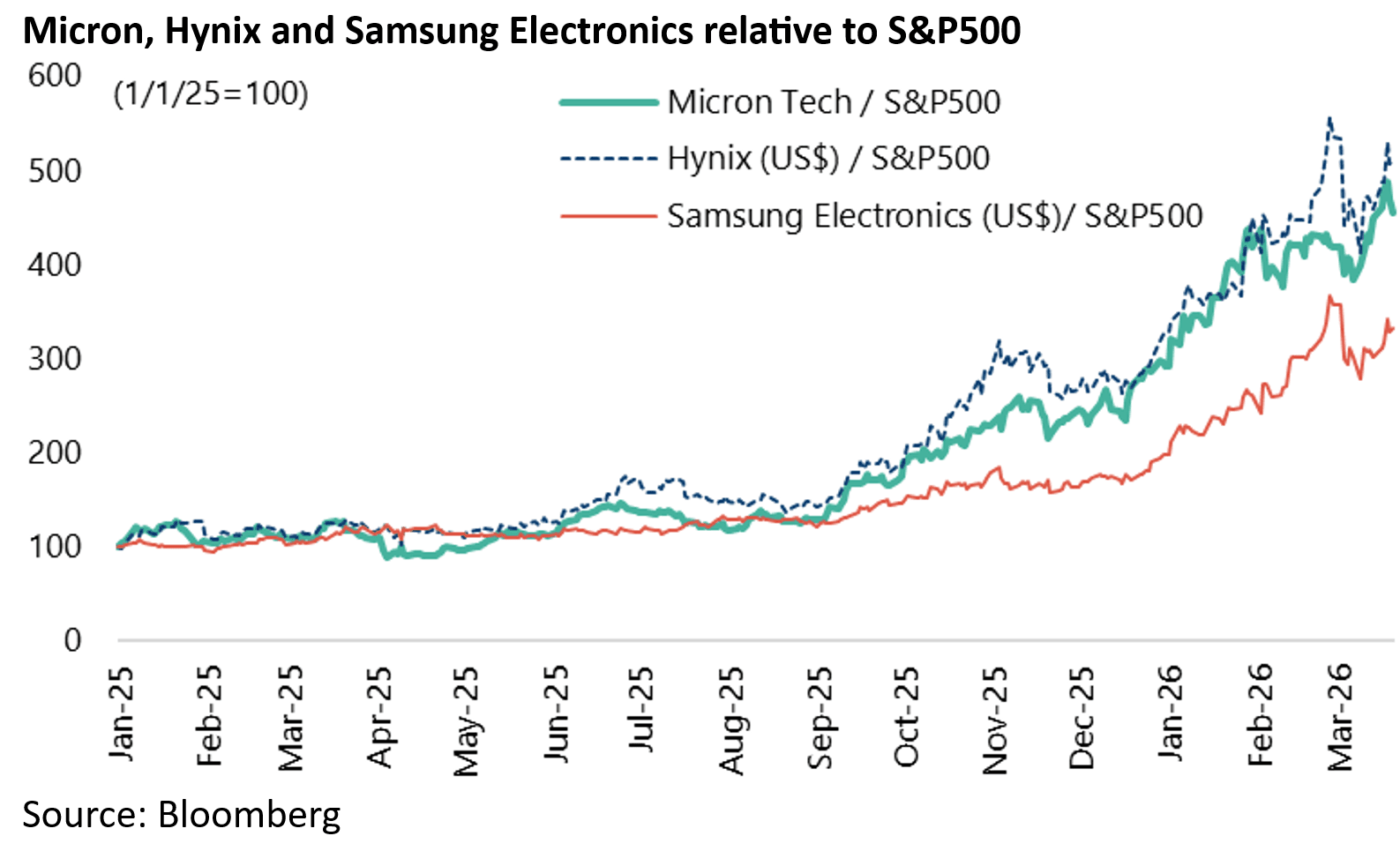

Indeed Nvidia has stopped outperforming the S&P500 since early November, though the DRAM memory producers are still outperforming for now.

Nvidia has underperformed the S&P500 by 12% since 3 November, while Micron, Hynix and Samsung Electronics have outperformed by 90%, 60 and 80% over the same period.

The other issue is who, if anyone, will most successfully monetise AI in the world outside China.

The best guess is that victory will go to Alphabet, which appears to have successfully integrated its Gemini AI into traditional search.

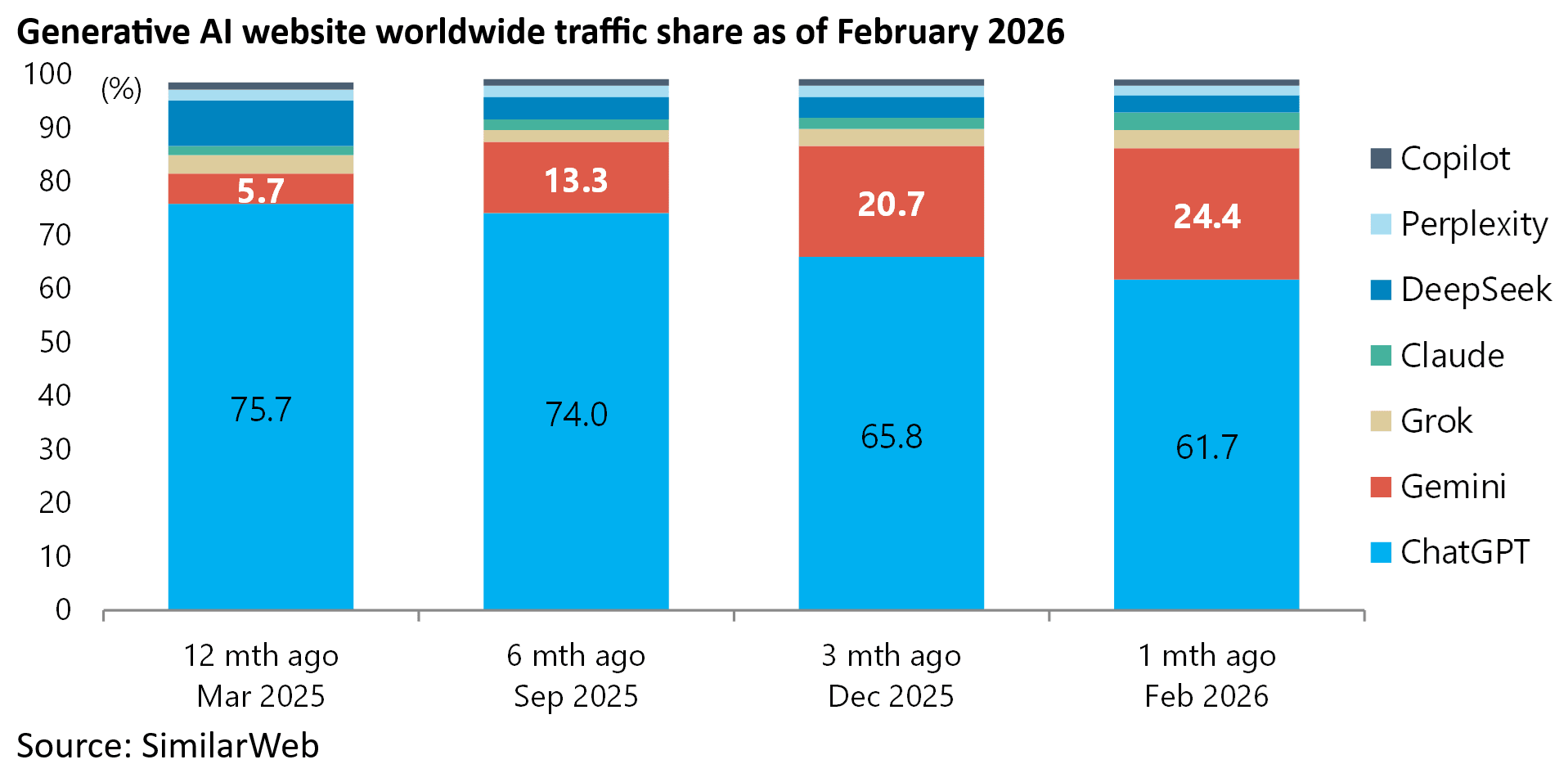

In this respect, the latest data continues to show people are spending less time on ChatGPT.

Gemini’s web traffic share in the Generative AI market has increased from 5.7% to 24.4% over the past 12 months, while ChatGPT’s market share has declined from 75.7% to 61.7% over the same period, according to SimilarWeb.

Unlike Last Cycle, Credit Spreads Won’t Foreshadow a Future Crisis

Moving on from AI, there continue to be problems emerging in the private credit space.

There have been two examples of late of BlackRock marking down a loan from 100 cents to zero.

The first involved private debt it had extended to Dallas-based Renovo Home Partners.

This was written down from a value of 100 cents on the dollar in October to zero in November.

BlackRock held the majority of Renovo’s roughly US$150m of private debt (see Bloomberg article: “BlackRock Faces 100% Loss on Private Loan, Adding to Credit Market Pain”, 10 November 2025).

The second BlackRock loan written down from 100 cents to zero occurred more recently.

An SEC filing released in late February shows that BlackRock slashed the value of a US$25m loan to Infinite Commerce to zero at the end of 2025, just three months after valuing it at par (see Bloomberg article: “BlackRock Slashed Private Loan Value From 100 to Zero”, 5 March 2026).

Fraud appears to have played a role in some of the recently publicized problems in private credit.

But it is becoming ever more obvious that the dodgy loans in this cycle have been extended in the unregulated private credit market rather than in what used to be known as the junk bond market — as has long been this writer’s base case (see “Private debt – A ticking time bomb”, 30 August 2023).

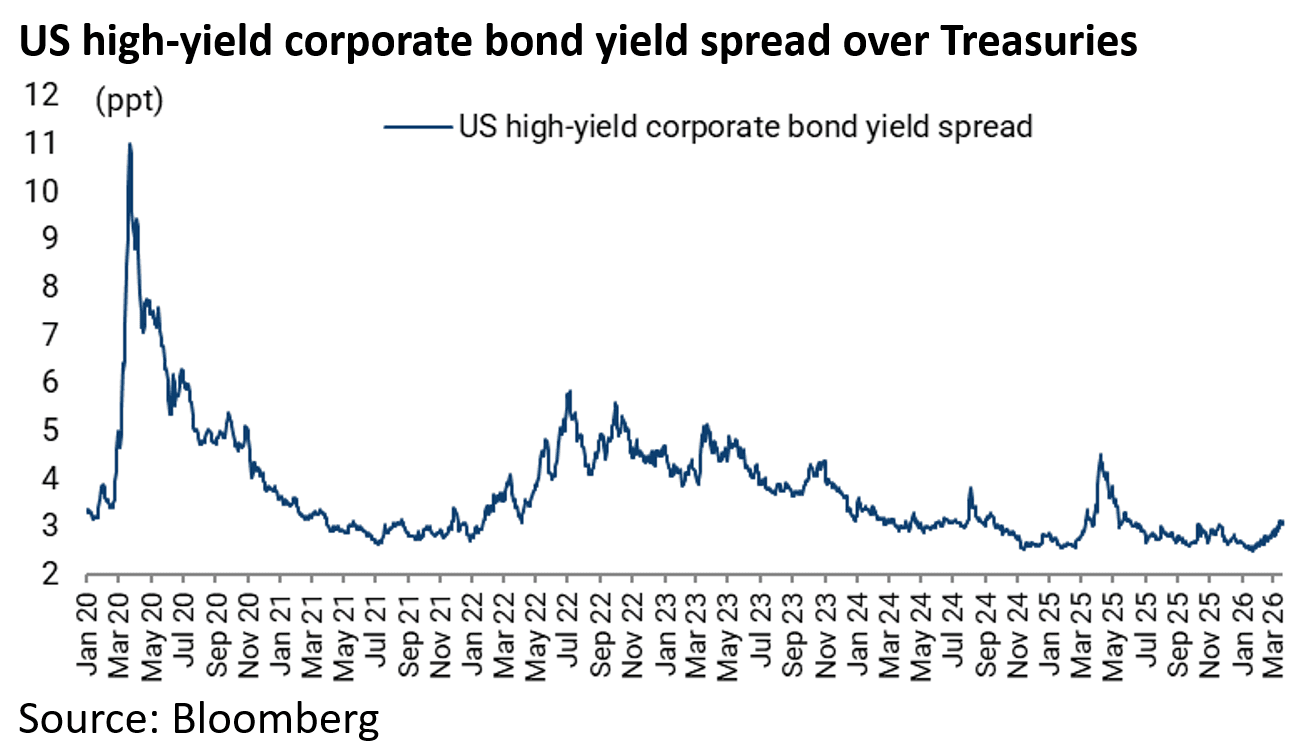

As such, credit spreads in the high-yield market will not play their usual role as a warning indicator.

Rather, the risk is that there will be no warning whatsoever, which was the case with the above cited examples.

Meanwhile, the US high-yield corporate bond index is still trading at “only” 312bp yield spread over the Treasuries, compared with 1,100bp in March 2020.

Fundamentally, it is worth re-iterating that the explosion in private credit in the US over the past 15 years has been one massive regulatory arbitrage after the over regulation of the commercial banks which followed the subprime mortgage crisis of 2007-2008.

This regulatory arbitrage has limited what well-meaning commercial bank regulators can do about shadow banking because they do not regulate private credit. Nor for that matter does anyone else.

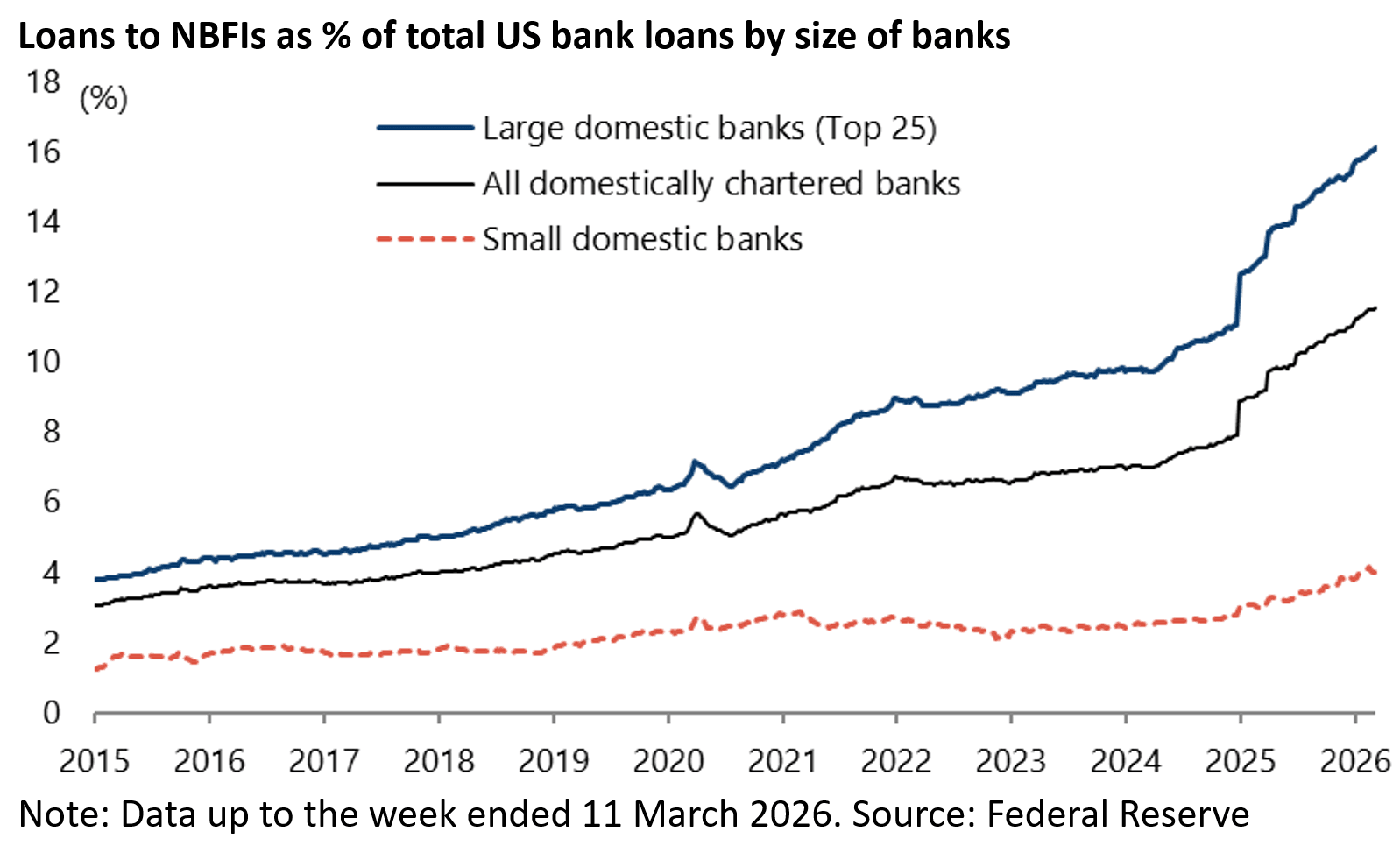

But increasingly concerned US bank regulators have started to address the issue by telling commercial banks to report their exposure to non-bank financial institutions (NBFIs), starting from December 2024.

Could the Shadow Banking System be a Systemic Risk?

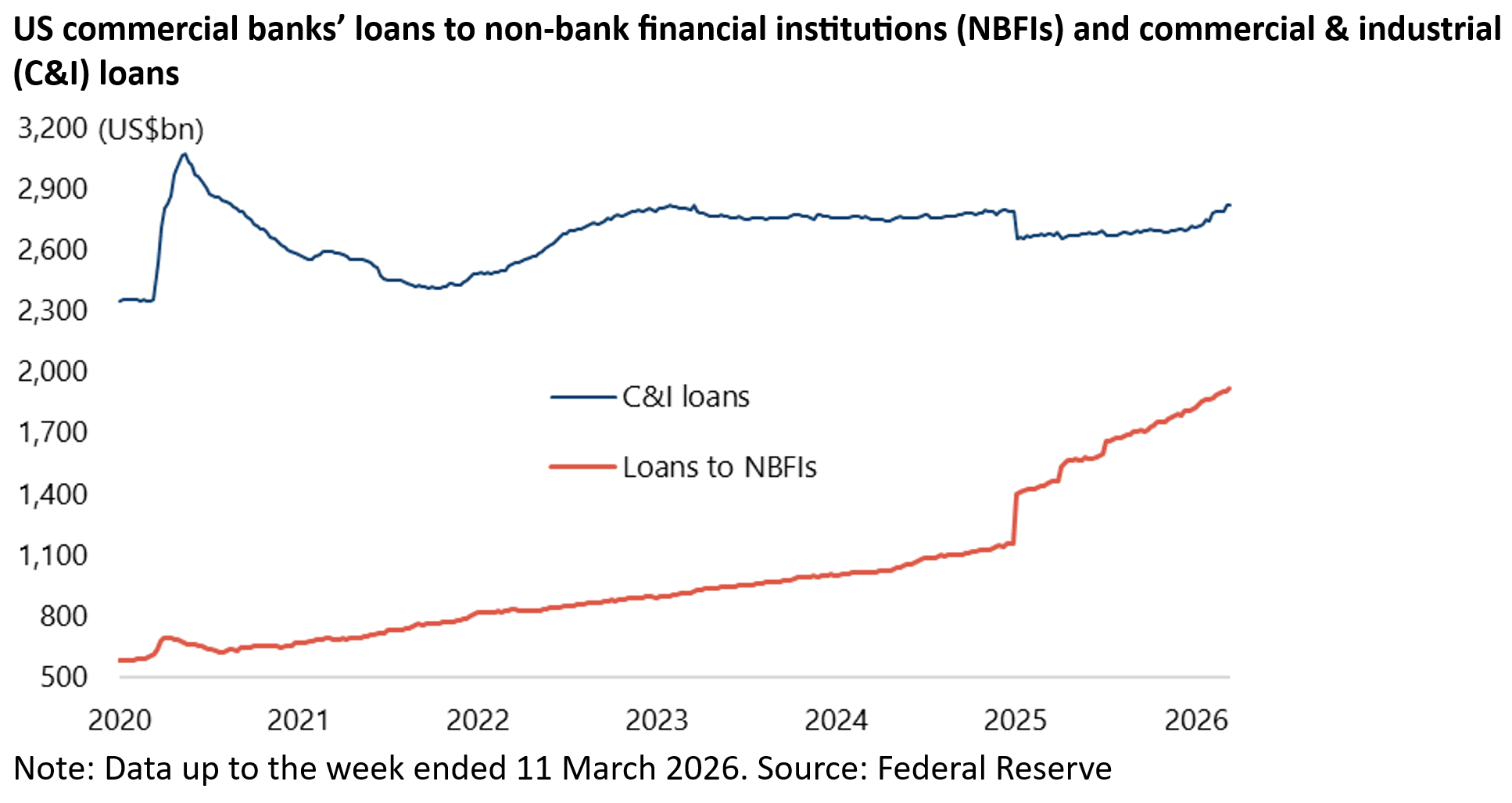

The latest information shows, unsurprisingly to this writer, a dramatic surge in commercial bank lending to NBFIs, as previously discussed here (see “The Financial Assets Most at Risk From Trump’s ‘Bull in a China Shop’ Strategy”, 3 June 2025).

US commercial banks’ loans to NBFIs have risen to US$1.92tn in the week ended 11 March, up 65.9% since the last week of 2024.

While commercial and industrial (C&I) loans rose by only 1.1% to US$2.82tn over the same period. This latest data is the result of a loan reclassification since the start of 2025.

A Moody’s report published last October has provided more data on this area of lending (see Moody’s report: “US private credit market reshapes bank lending and risk”, 21 October 2025).

The report confirms that lending to NBFIs has been the fastest-growing loan category in US commercial bank lending, with such loans representing 10.4% of total US bank loans as of 2Q25, up nearly threefold from 3.6% a decade ago.

A further data point worth noting is that NBFI lending accounts for a higher 15% of the loans of the 25 largest US domestic banks as of 2Q25.

Meanwhile latest weekly data released by the Federal Reserve shows that NBFIs’ share of US bank loans has increased further to 11.6% for all US domestic banks and 16.2% for the 25 largest banks as of the week ended 11 March 2026.

Note: Data up to the week ended 11 March 2026. Source: Federal Reserve

Another Moody’s report published last November focuses on a related issue.

That, the growing exposure of US life insurers to private credit or what are termed “less-liquid and privately rated investments” (see Moody’s report: “Private assets boost US life insurers’ returns but reduce liquidity, transparency”, 12 November 2025).

Such illiquid investments accounted for 18% or US$685bn of the industry’s US$3.8tn in fixed income holdings at the end of 2024, according to Moody’s.

Furthermore, the exposure is concentrated with 10 life insurers accounting for 43% of the illiquid assets. The same Moody’s report also notes that life insurers’ exposure to illiquid assets has continued to grow in the first half of last year.

On a related point, it is also worth highlighting that UBS Chairman Colm Kelleher warned last November that insurers shopping for better ratings on their private credit assets are creating a “looming systemic risk” to global finance (see Financial Times article: “UBS chair warns of ‘looming systemic risk’ from private credit ratings”, 4 November 2025).

Kelleher said the insurance industry, especially in the US, was engaging in “ratings arbitrage” akin to what banks and other institutions did with subprime loans before the 2008 financial crisis.

Similarly, the Bank for International Settlements (BIS) also said last October that ratings on private credit assets held by US insurers might have been inflated and warned of the risk of fire sales during periods of financial stress.

Smaller rating agencies have captured market share in private credit by providing so-called private letter ratings, which are typically only visible to an issuer and select investors, according to the BIS (see BIS Paper – “The transformation of the life insurance industry: systemic risks and policy challenges”, 27 October 2025).

The above is why it is no surprise to read that the National Association of Insurance Commissioners (NAIC) recently restructured its task force focused on the “scrutiny of private and complex asset holdings”.

The regulatory focus is long overdue, given the longstanding practice of growing “payments in kind” (PIK) in private credit also previously discussed here (see “Private Credit’s Incredible Vanishing Cashflow”, 16 December 2024).

This is a practice where companies financed by private credit are opting to increase their principal balance outstanding rather than paying cash to make interest payments.

While such PIK is counted as “income” each quarter, the private credit funds do not receive cash payments until the loan is refinanced or matures.

Retail Investors Beware

Then there is the related issue that private credit has begun to be sold to retail investors following deregulation last May.

This is despite the fundamentally illiquid nature of the underlying assets as has become clear of late as investors have tried to pull out of these so called “semi-liquid” funds.

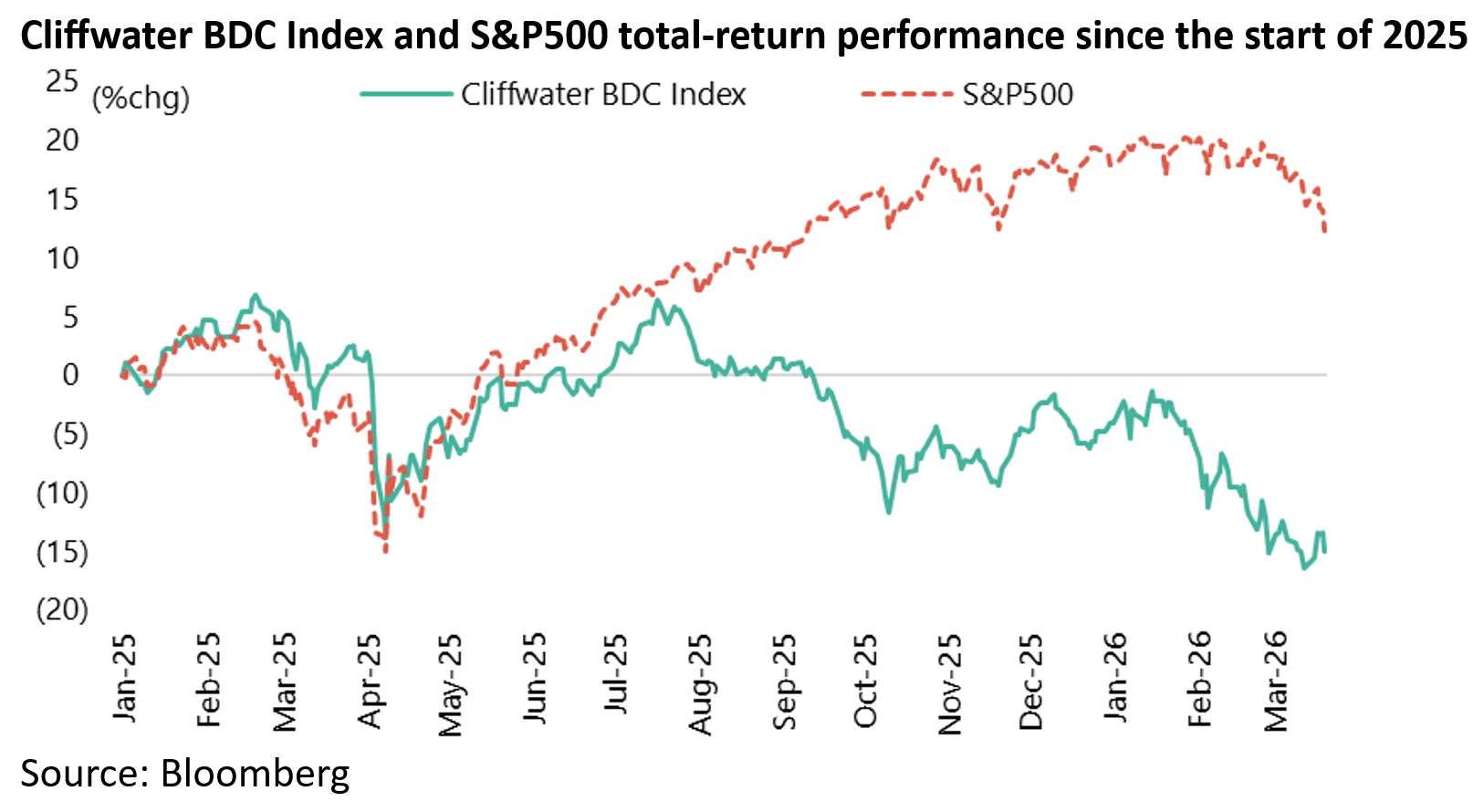

Still, some transparency on the pricing in this sector can be obtained by monitoring quoted business development companies (BDCs).

On this point, the Cliffwater BDC Index of 41 lending-oriented exchange-traded BDCs has shown a diverging trend with the S&P500 since mid-July 2025.

The index has declined by 20.1% since mid-July on a total-return basis and is down 14.9% since the start of 2025.

By contrast, the S&P500 has risen by 4.2% since mid-July on a total-return basis and is up 12.4% since the start of 2025.

Meanwhile there is a certain symmetry, or should this writer say inevitability, in that the two obvious areas of excess in this cycle have begun to converge: private credit and AI capex.

Still, this writer would advise all lenders, be they commercial banks, insurers, or private credit players, to become extremely wary of extending more credit to data centers, as this cycle is now so well advanced.

Investing in data centers, or what used to be characterized as “digital infrastructure”, seemed entirely sensible a few years ago. But as the AI capex arms race has reached ever more maniacal proportions, and as debt has increasingly been employed rather than cash to finance such spending, the endgame in terms of a massive oversupply of data centers seems increasingly inevitable.

Chris, You are the most talented macro analyst or strategist I ever worked with. You nailed the Japan bubble, the Asian Financial Crisis, the internet bubble and the GFC. I think you are incorrect on the dynamics and economics of AI. Please reach out anytime if you would like to discuss. Best wishes, James

Great article!

I wrote about private credit risk today as well.

Private Credit…Is The Next Risk For The Economy And Real Estate Hiding In Plain Sight?

https://hallmarkabsservice.substack.com/p/private-creditis-the-next-risk-for?utm_campaign=post-expanded-share&utm_medium=web

Mike