Is More Carry Trade Volatility In Store for Markets?

Is Japan kicking the can down the road, creating a future risk of an even worse unwind?

Author: Chris Wood

Financial markets found out about the potential for a yen carry trade unwind last month as reflected in the roller coaster market action in Tokyo.

The Topix declined by 20% in three trading days in early August.

But the reality is that this was a correction driven by technical factors, the selling of leveraged positions, rather than anything fundamental.

Still Bank of Japan Governor, Kazuo Ueda, was unlucky in the sense that his long overdue decision to move more proactively to normalise monetary policy coincided almost to the day with the US employment report for July which finally showed real labour market weakness.

The issue now is whether the BoJ will retreat back into the cave.

Deputy Governor Shinichi Uchida gave a speech on 7 August where he was at pains to stress that the BoJ would not raise rates again if markets remained volatile.

Speaking to local business leaders in Hakodate, Uchida said that the BoJ needed to maintain the current policy interest rate for the time being, “with developments in financial and capital markets at home and abroad being extremely volatile”.

This is the same central banker who gave a speech in late May essentially declaring victory over deflation as discussed here previously (see When will local buying drive Japanese stocks to new high?, 26 July 2024 and Uchida speech: “Price Dynamics in Japan over the Past 25 Years”, 27 May 2024).

Meanwhile, talking heads were quick to criticise the BoJ for its rate hike.

This, in this writer’s view, was nonsense.

[su_note note_color="#80e3f9" radius="8"]The longer the Bank of Japan takes to normalise monetary policy, the bigger will be the resulting carry trade and the greater will be the ultimate disruption. That the central bank has already waited too long is evident from the fact that a 15bp increase in the overnight call rate target on 31 July could have had such an impact.[/su_note]

This is why former BoJ governor Haruhiko Kuroda should have declared victory over deflation and started to normalise monetary policy before he stepped down in April 2023.

That he did not do so left his successor Ueda with the tricky task.

The reality is that Ueda acted because he was undergowing political pressure at the time to address the collateral damage of the weak yen in terms of declining real wages.

Still the same politicians who were asking him to raise rates may now well be doing the opposite, or at least such is suggested by Uchida’s speech.

Japanese Investors Slowly Moving Back into Local Stocks

The hike coinciding with the weak US employment data was certainly unfortunate given Japanese Prime Minister Fumio Kishida’s sensible policy of trying to encourage domestic investors to invest into equities via the expanded NISA scheme.

This had been working.

The latest Japan Securities Dealers Association survey of 10 major traditional and online brokerages showed that domestic stocks accounted for 41% of the purchases via the new NISA program in the January-July period, compared with 56% for investment trust funds.

The survey also showed that purchases through NISA accounts totaled Y8.56tn in January-July, up fourfold from Y2.10tn in January-July 2023.

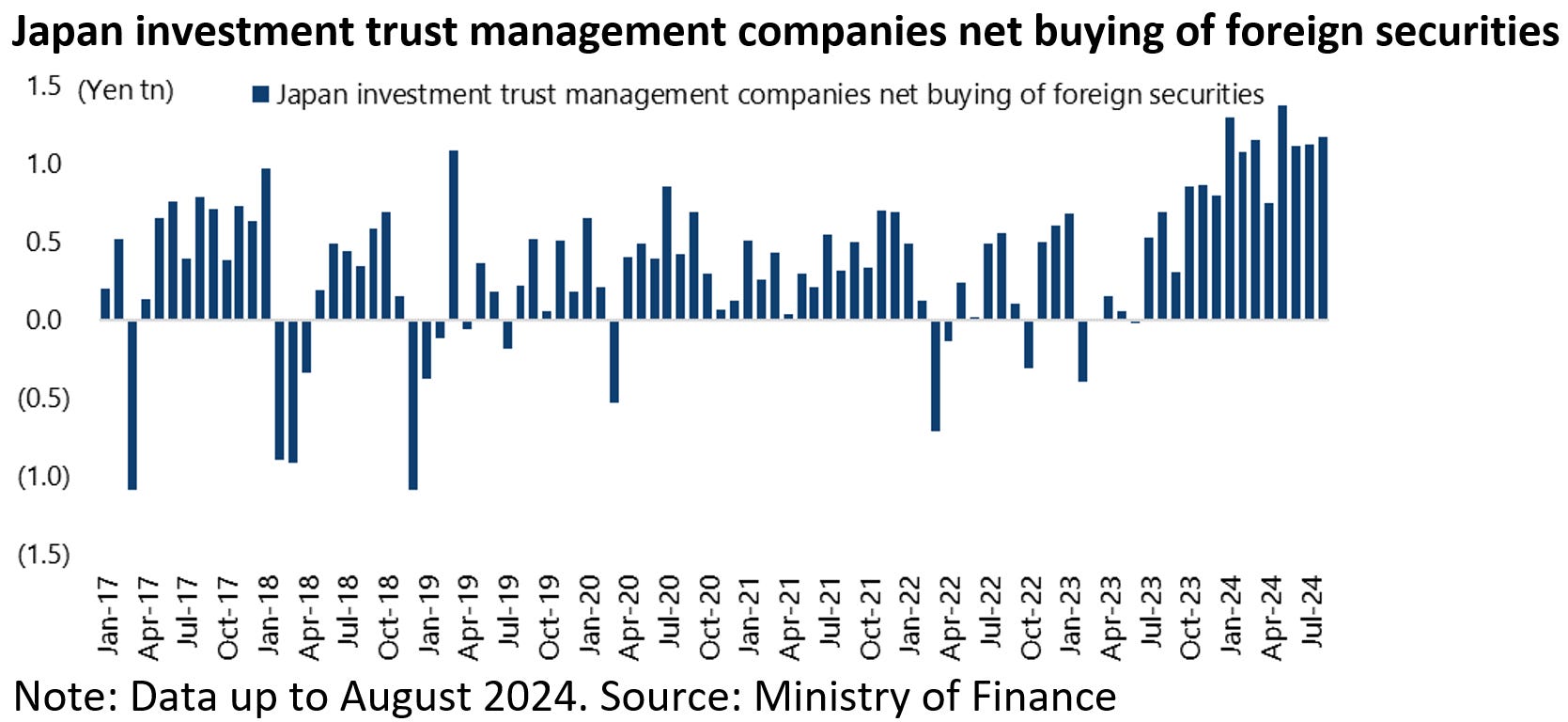

But the risk is that the extreme volatility seen of late as regards Japanese equities will encourage NISA flows into markets outside Japan.

The Ministry of Finance data shows that Japanese investment trust management companies bought a net Y1.17tn of foreign securities in August after buying a net Y7.87tn in the first seven months of 2024.

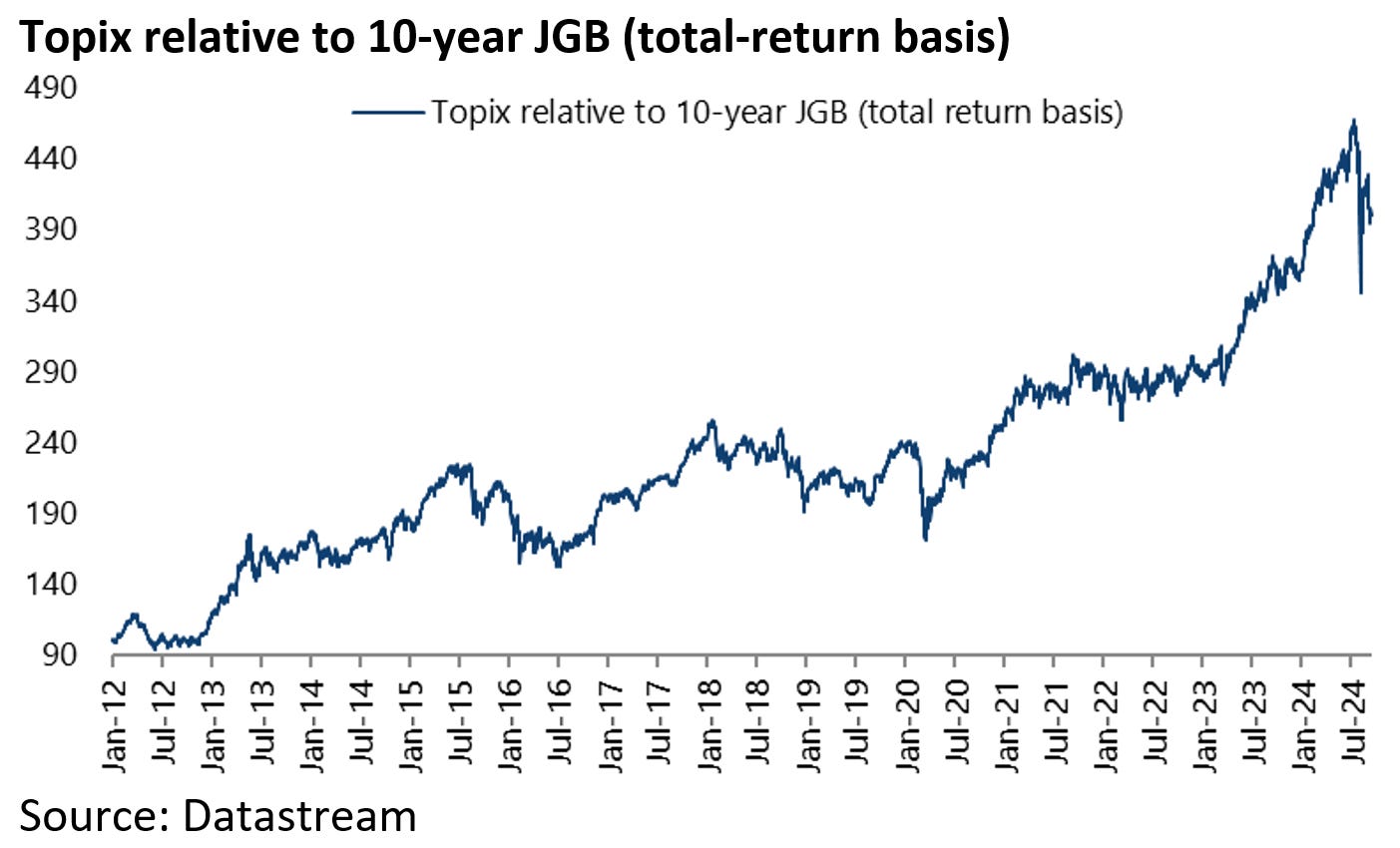

Meanwhile one reason why Japanese institutional investors have not reallocated out of yen fixed income into Japan equities, in spite of the dramatic outperformance of the Topix over the 10-year JGB since the launch of Abenomics in late 2012, is that they are obsessed with volatility-adjusted returns.

This writer has never been a believer in Sharpe ratios and the like but many asset allocators are.

Certainly, there has now been a reminder of the Japan market’s tendency for extreme volatility, which is itself a function of the lack of domestic institutional support which tends to make it a playground for foreigners.

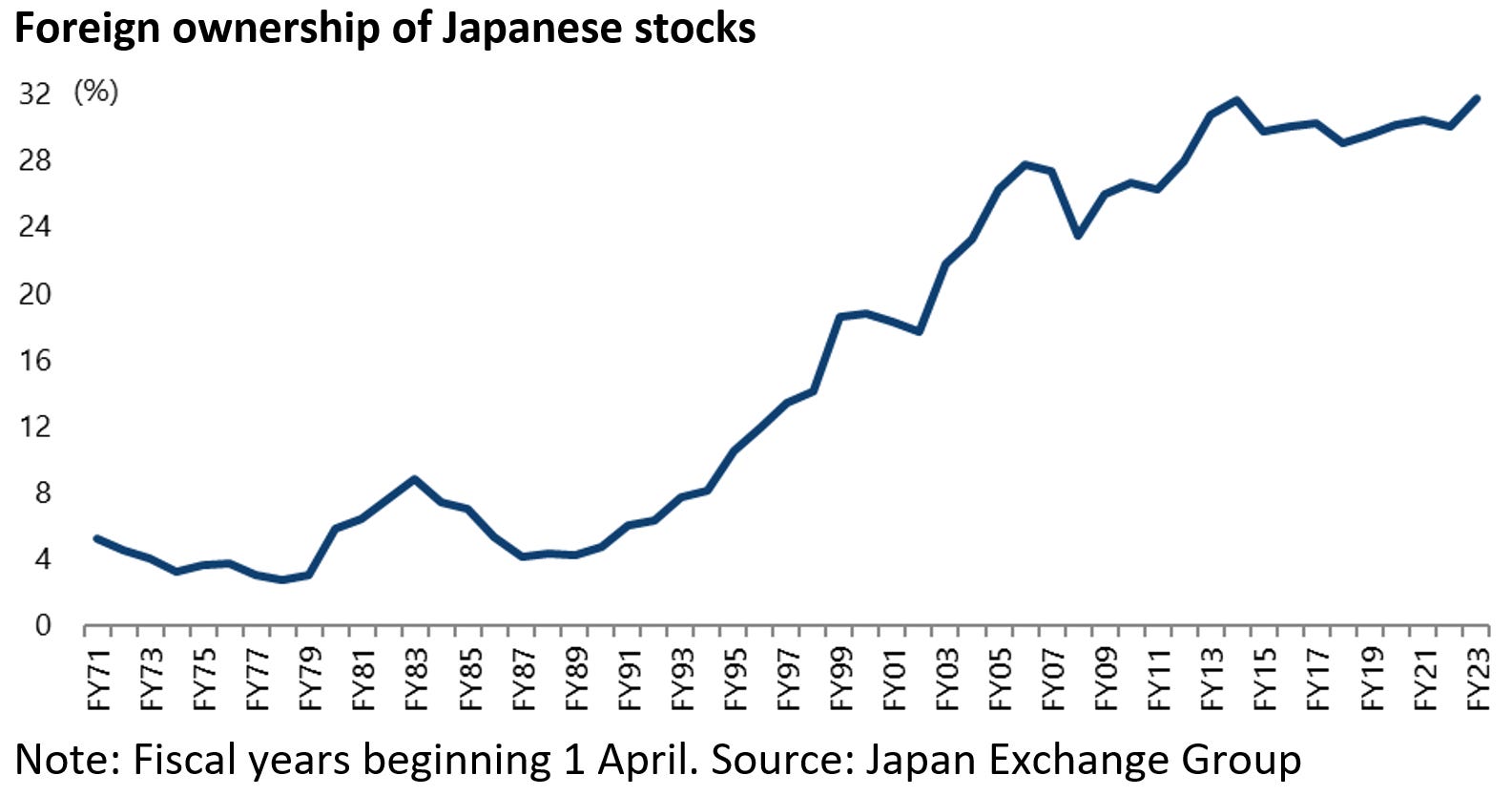

On that point, foreign ownership of the Japanese stock market has increased from 4.2% to 31.8% since the peaking of the Bubble at the end of 1989.

The US Job Marketing is Weakening, But Slowly

Meanwhile money markets are now discounting a further 7.5bp of BoJ rate hike by the end of this year and 120bp of Fed easing this year after the latest US employment and CPI data.

On employment, the US data continues to weaken without collapsing.

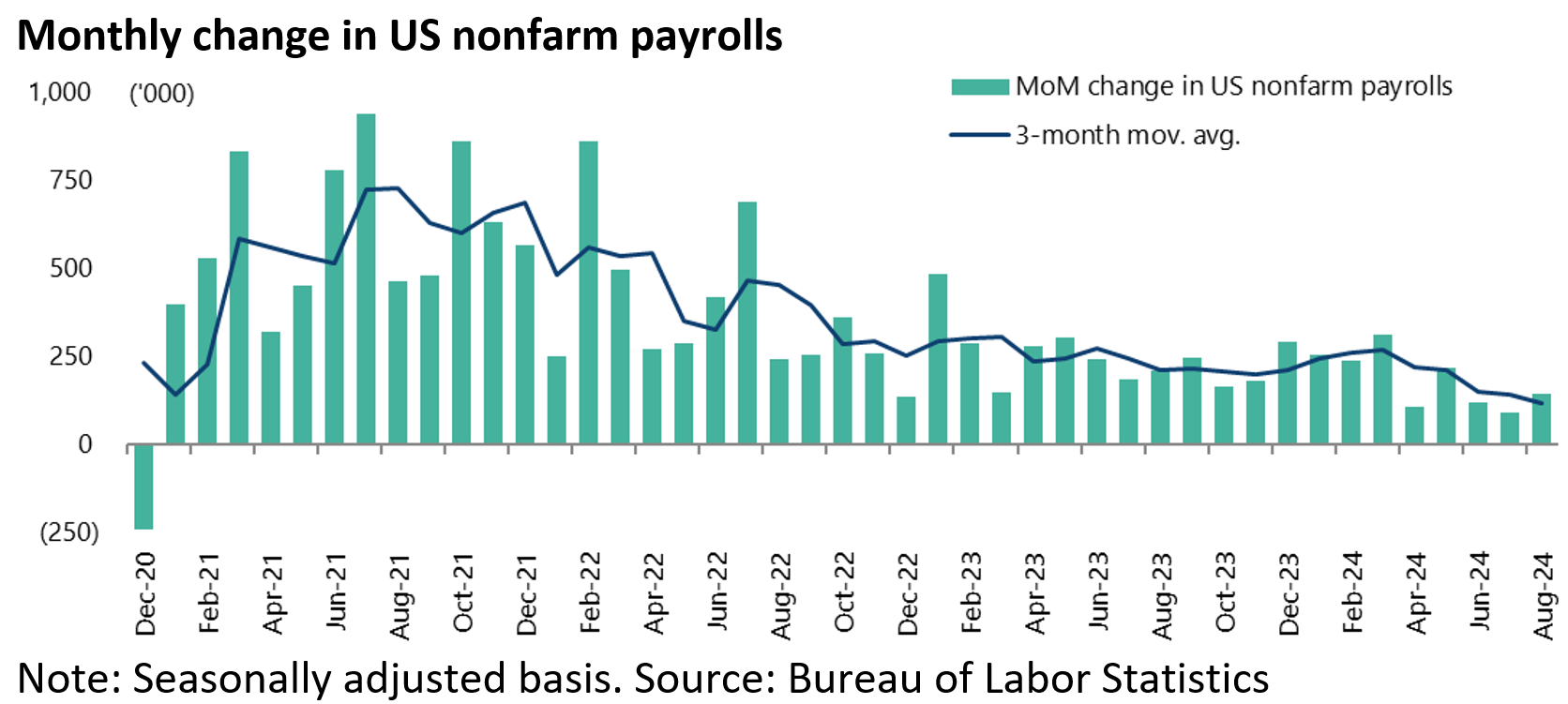

US nonfarm payrolls increased by 142,000 in August on a seasonally adjusted basis, compared with consensus expectations of 165,000.

While the increase in the previous two months was revised down again by a combined 86,000 with July job gains lowered from 114,000 to 89,000, the lowest level since December 2020.

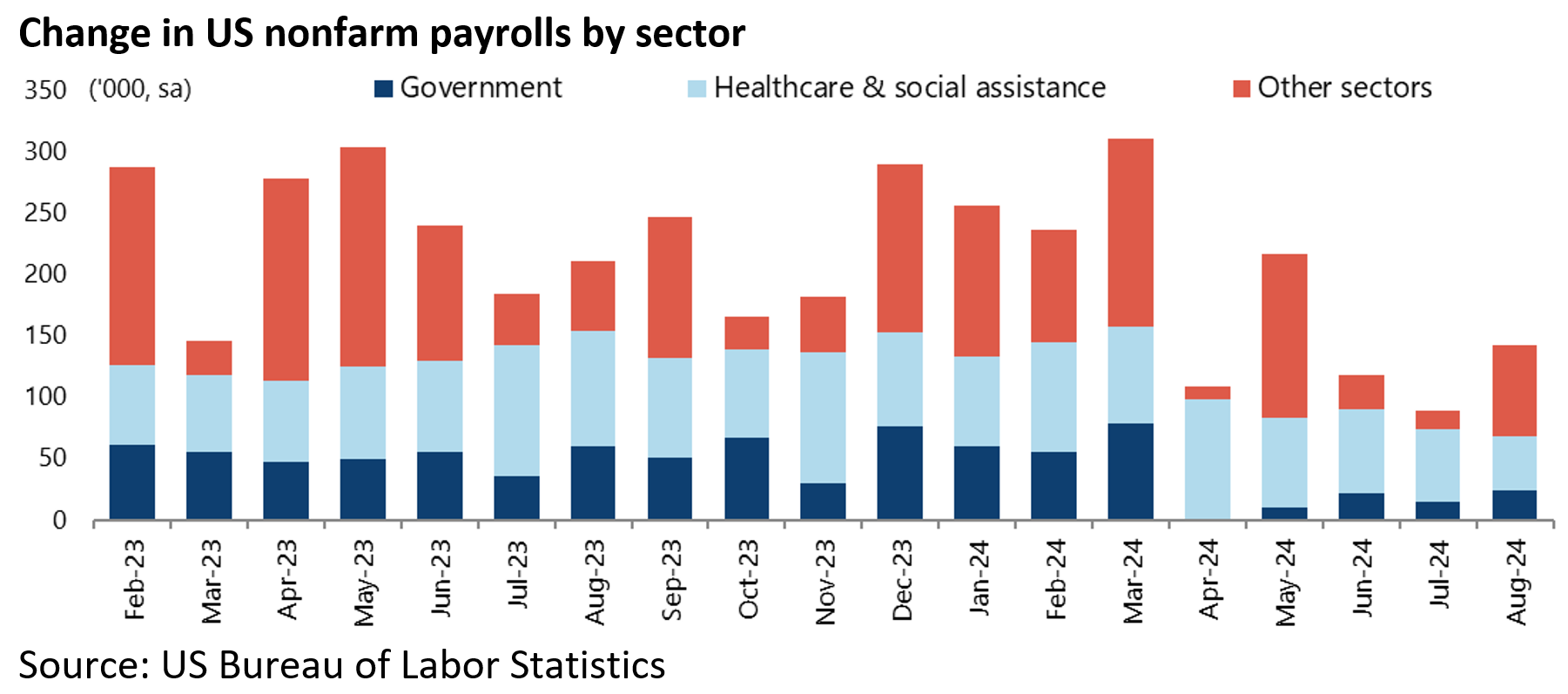

In terms of the details, employment in the government and healthcare and social assistance sectors increased by 68,100 in August on a seasonally adjusted basis, accounting for 48% of the increase in nonfarm payrolls.

On an annualised basis, the government and healthcare/social assistance sectors’ jobs have now increased by 1.407m in the 12 months to August, accounting for 60% of the 2.358m increase in nonfarm payrolls.

This reflects fiscal easing.

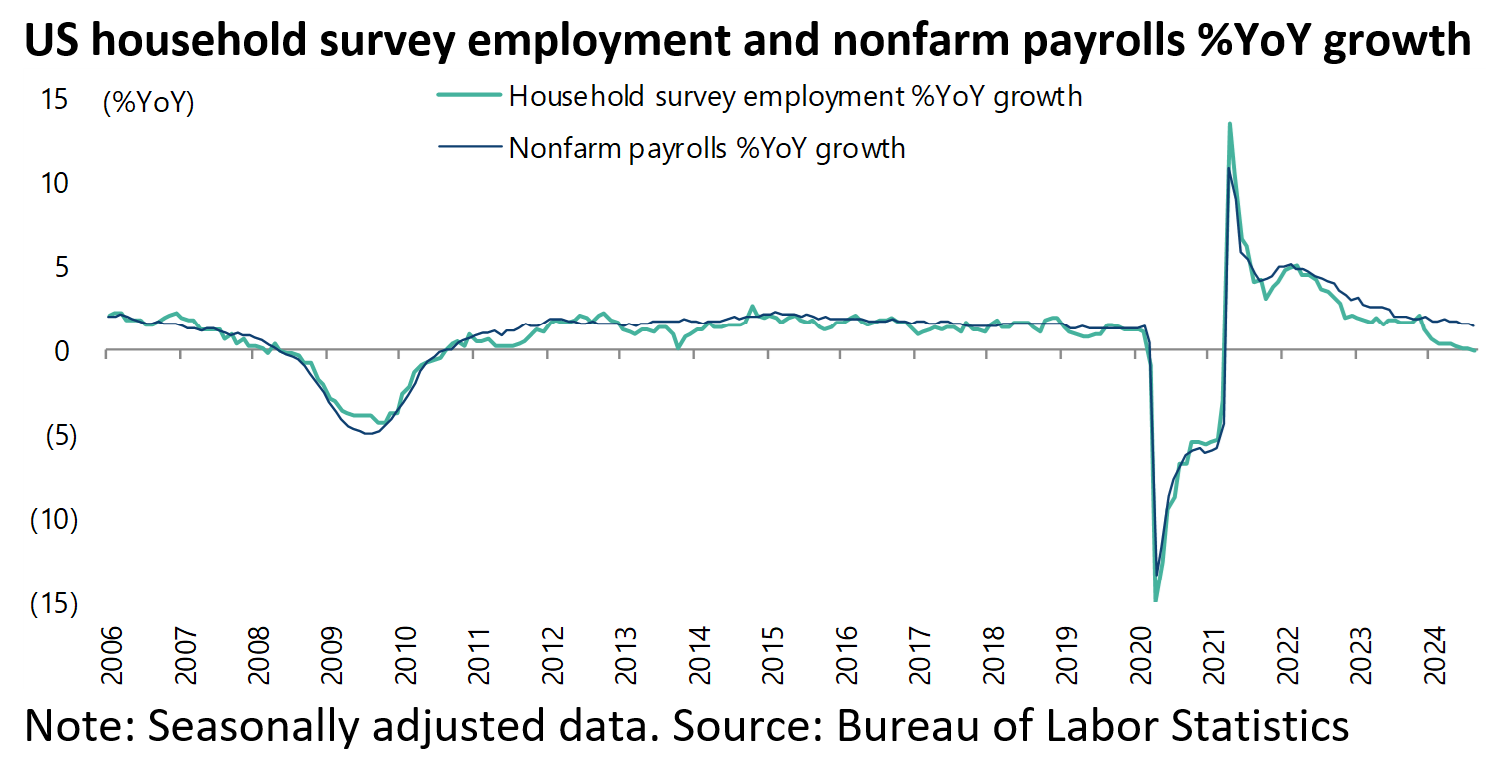

It is also worth noting that the household survey is now showing a YoY decline in employment generation as of August.

Household survey employment has declined by 66,000 or 0.04% in the past 12 months to August. This is the first YoY decline since August 2010 if the Covid-impacted period of 2020-2021 is excluded.

By contrast, nonfarm payrolls are still rising by 1.5% YoY.

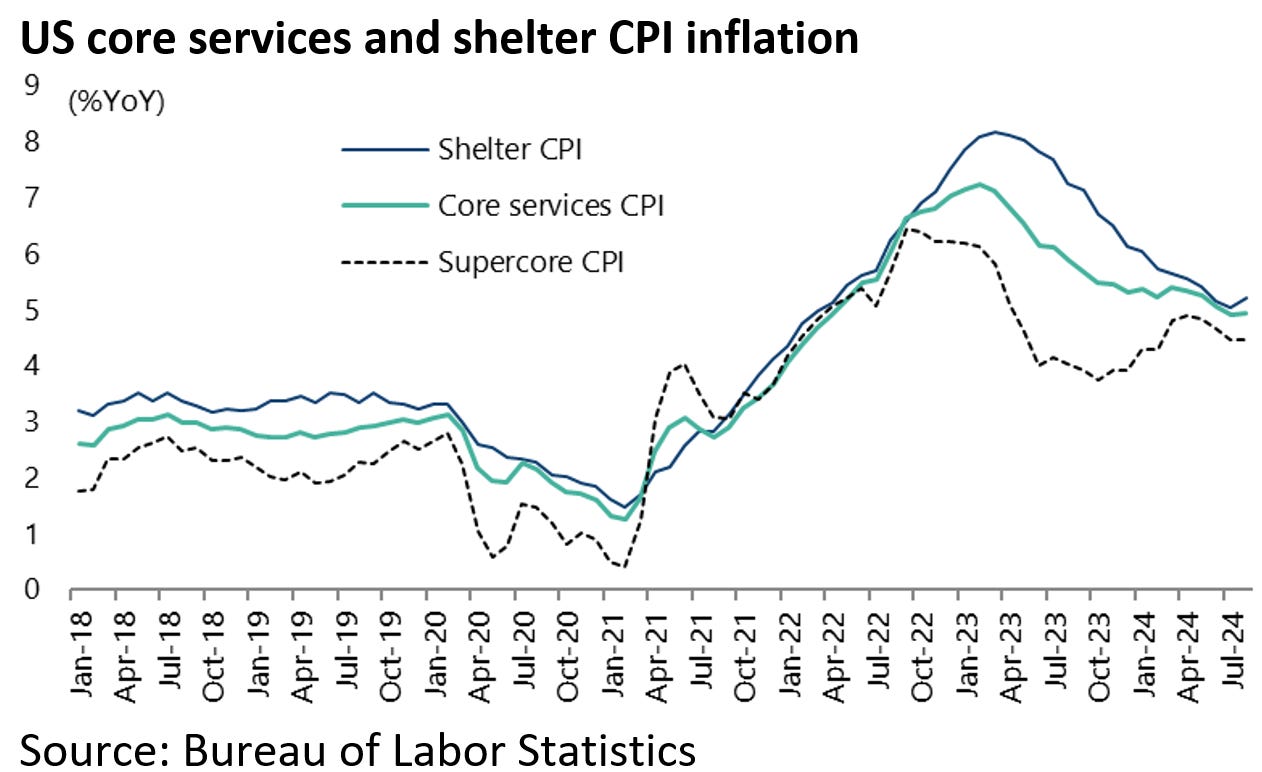

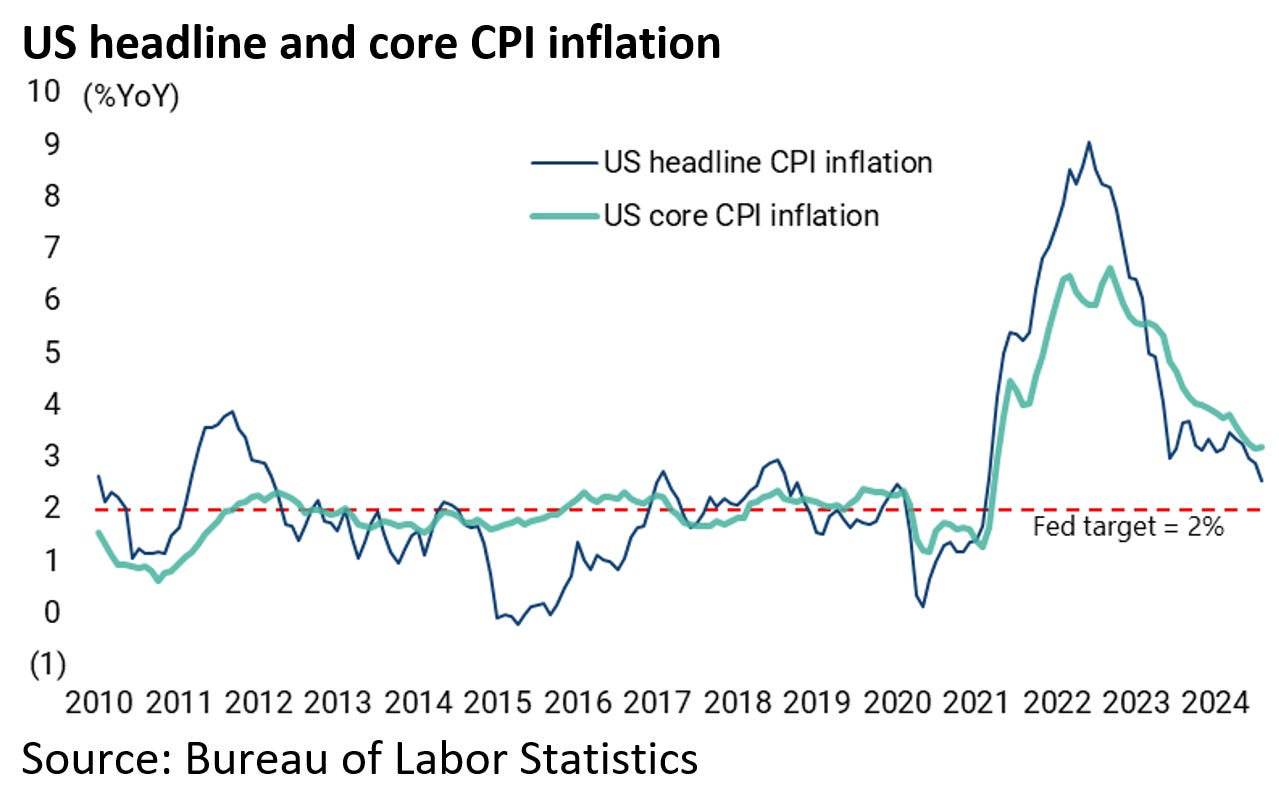

Inflation is Falling but Still Above Target and Sticky

As for inflation, the August US CPI data released last week was broadly in line with consensus expectations.

Headline CPI rose by 0.2% MoM and 2.5% YoY in August, in line with consensus expectations and down from 2.9% YoY in July.

While core CPI rose by 0.3% MoM and 3.2% YoY, compared with consensus expectations of 0.2% MoM and 3.2% YoY.

Still services inflation remains relatively sticky.

Core services CPI rose by 4.9% YoY in August with shelter CPI inflation at 5.2% YoY, compared with 4.9% YoY and 5.1% YoY respectively in July.

While the so-called supercore inflation, which measures core services CPI excluding housing, was unchanged at 4.5% YoY in August.