Is Japan's Stock Party Over, or Is the Best Yet to Come?

Author: Chris Wood

“Government may declare official end of deflation”.

This was a frontpage headline in the Japan Times last quarter.

This, and the Nikkei breaking the 40,000 level for the first time ever on 4 March, suggests that this is a historic inflection point in Japan after more than three decades of struggling against the deflationary doldrums.

The Nikkei closed at 37,935 on 26 April.

Still, if this is the story of the moment, it is the case that the Japanese stock market remains almost exclusively driven by foreign money.

Foreigners now own 31% of the Japanese stock market, up from 4% at the peak of the Bubble in late 1989 since when Japanese domestic institutions have continued to reduce weightings to their own stock market.

Of late, foreign investment has picked up, as previously China-focused Asian equity funds have expanded their mandate to include the now far more exciting Japan market as China has succumbed to its own deflationary doldrums as discussed here recently (see Is China Investable Yet?, 28 April 2024).

Meanwhile, global investors have been adding to Japanese equities to reduce their underweight in Japan.

The motivation has been twofold.

To reallocate funds to another liquid market in Asia as they have stopped investing in China which has been increasingly viewed as ‘uninvestable’.

To hedge the risk that Japan is finally on the brink of a self-sustaining move out of deflation.

Still, the need to hedge the risk of being underweight Japan is less urgent for US-dollar-based investors because of the cheapness of the yen.

Thus, the Topix is up 42% from the beginning of last year in yen terms, but the weighting of Japan in the MSCI All Country World Index is down from 5.56% to 5.27% over the same period.

If this is the overall context, this writer is still waiting for confirmation that Japanese institutions believe in their own stock market in terms of a reallocation out of yen fixed income into Japanese equities.

There is still no compelling evidence of this.

Still, the much-trumpeted reform of the Nippon Individual Savings Accounts (NISA), which kicked in from 1 January, has led to the anticipated increase in flows into these accounts.

The new NISA rules have removed time limits on tax benefits and allowed people to put more into NISA accounts.

Under the new NISA system, the annual investment limit for a regular NISA account was doubled from Y1.2m to Y2.4m while the limit for the so-called Tsumitate NISA account was raised from Y400,000 to Y1.2m.

The previous limit on the tax exemption period was also abolished.

Breach of the 1989 Stock Market High is Drawing in Retail Investors, but Institutions Aren't Following.

Meanwhile, the breach of the late-1989 all-time high of 38,957 on the Nikkei in late February has begun to attract retail investor flows.

The top five onshore Nikkei 225 ETFs with assets over Y1tn have attracted Y459bn of inflows so far this year, compared with an aggregate outflow of Y104bn in 2023.

Note: Include five ETFs benchmarking the Nikkei 225 Index with assets over Y1tn. Data up to 26 April 2024. Source: Bloomberg[/caption]

In this respect, a younger generation who cannot remember the trauma of the extended hangover from the Bubble are more likely to invest.

It also should not be forgotten that a stock market rally is in the interest of both the Government Pension Investment Fund (GPIF) and the Bank of Japan, both of which have “skin in the game” in terms of their Japanese equity exposure.

The GPIF raised its target allocation to Japanese equities from 12% to 25% back in October 2014 by reducing its exposure to JGBs under pressure from then Prime Minister Shinzo Abe.

That move has paid off handsomely, though the reallocation was not followed by other domestic institutions.

Meanwhile, the BoJ’s equity exposure totaled Y64.1tn (US$454bn) at market value at the end of 4Q23, based on the BoJ’s flow of funds data.

On monetary policy, the Bank of Japan finally ended negative rates at its March monetary policy meeting.

The official line is that the central bank had been waiting for wage data.

The preliminary result of this year’s shunto wage round for big companies, announced in mid-April, show that the pay increase was 5.2% compared with last year’s 3.6%.

But the real issue for the economy at large will be what happens to SME wages, as they employ about 70% of private sector employees.

Last year, the estimate is that SMEs raised wages by 2%, with hopes that will rise to 2.5% this year.

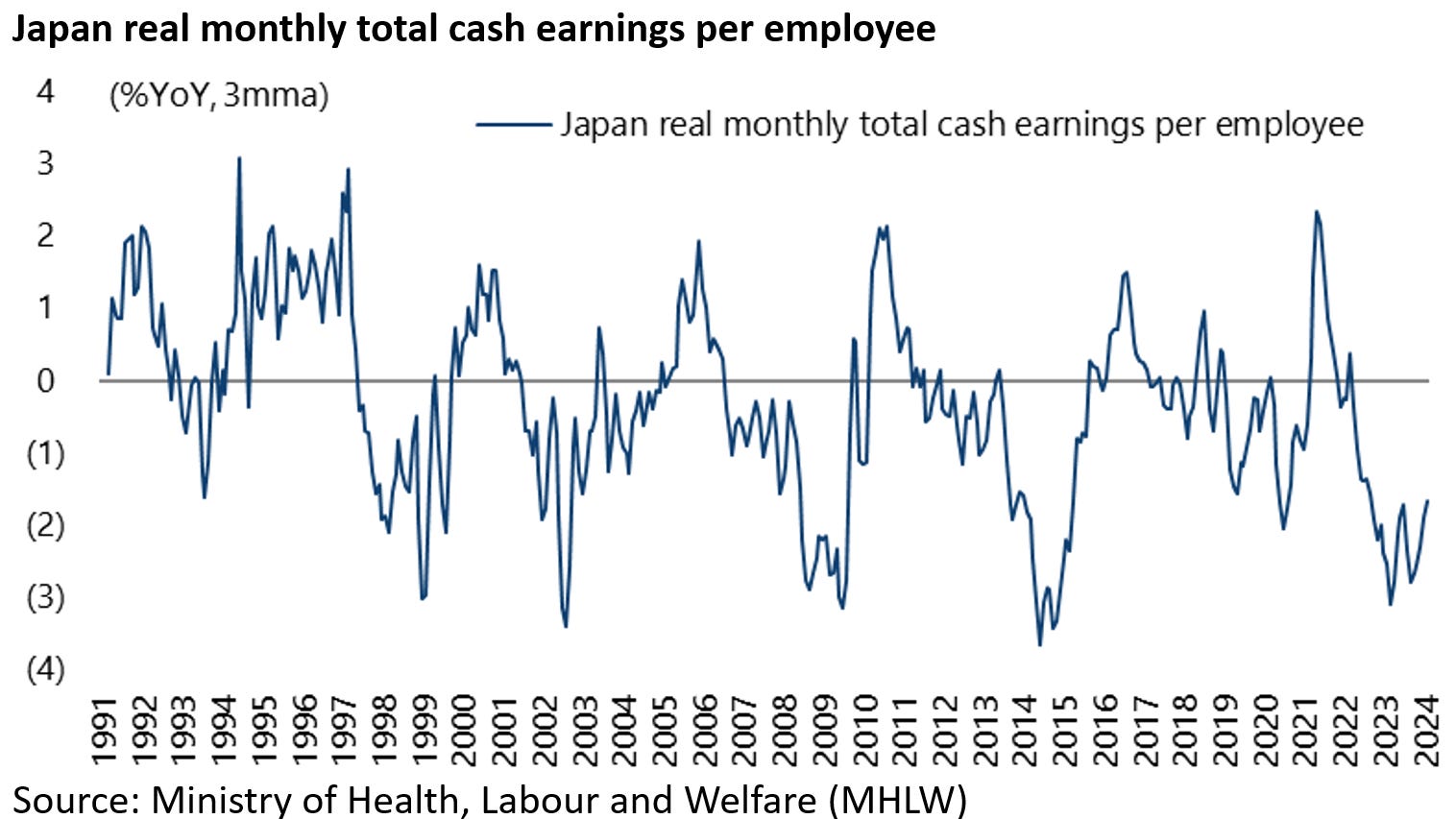

The lack of a bigger pickup in SME wages is probably the biggest risk to the reflation story, given that real wage growth is still negative.

Real average monthly total cash earnings per employee declined by 1.8% YoY in February and by 1.7% YoY in the three months to February.

If the end of negative rates has sent a positive signal, there is certainly room for more rate hikes since the BoJ’s deposit facility rate is only 0.1%.

A CAPEX Cycle is Japan's Best Chance to Reignite Inflation

Meanwhile the best hope of a sustained reflationary cycle is a capex cycle driven by the ultra-competitive yen.

In this respect, it makes increasing sense for Japanese corporates, which for years have been moving production offshore, to reverse that course given how low Japanese wages are in dollar terms.

Average monthly schedule cash earnings per full-time employee are now running at only US$2,225 down from US$3,800 in 2012.

One thing is for sure. Corporate profits in Japan, thanks to the weak yen for exporters, have been surging and labour has not been getting much of the benefit.

Japanese nonfinancial corporations’ annualised profits to sales ratio rose from 4.7% in 4Q20 to 7.0% in 4Q23, while their annualised wages and salaries to sales ratio declined from 8.9% to 8.1% over the same period.

This is despite the severe shortage of labour driven by Japan’s demographics.