Has Passive Investing Gone Too Far?

Author: Chris Wood

This writer was interested to read of late about research on the distorting impact of passive investing, most particularly in the US stock market.

This research found that passive flows can exert a US$5 or more impact on index levels for each dollar of investment and potentially 20 times or more in the case of US Big Tech stocks (see NBER working paper: “In Search of the origins of financial fluctuations: The inelastic market hypothesis” by Xavier Gabaix and Ralph Koijen, June 2021).

More precisely, the research paper noted: “Only $0.8 was invested in equities, yet the value of the equity market increased by $4, again a five-fold multiplier”.

This dynamic is apparently amplified by the use of synthetic indices which only include the biggest stocks for convenience (as the larger their representation in the index – the higher the correlation with the index).

Such an approach also has the benefit of lowering trading costs.

Such findings are in the context of an era where passive investing has surged over the past 30 years and now dominates over half of US equity and bond funds.

This shift has clearly led to greater market concentration and reduced-price sensitivity.

As passive funds replicate indices with fewer securities, their influence on price action has grown, making markets increasingly flow-driven rather than fundamentals-based.

The Growth of the Magnificent-7 in recent years meant that holding those seven stocks has given passive investors the bulk of the index replication.

Other research seen by this writer shows that passive investors tracking five of the most popular indexes, including the S&P500, collectively owned 33.5% of the US stock market in 2021 (see “The Passive-Ownership Share Is Double What You Think It Is” by Alex Chinco and Marco Sammon, 7 April 2024).

The percentage has probably grown since.

This writer has long been critical of the theoretical case underpinning indexation since it amounts to everybody buying the same thing or what has been described in the past as “investor socialism”.

Still it is interesting to see some quantitative estimates of the impact.

Indexation and the Dangers of the Ultimate Momentum Trade

Meanwhile the dangers of indexation, in terms of it degenerating into the ultimate momentum trade, become even greater the more passive investing dominates the market.

Passive investing is estimated since late 2019 to have accounted for more than half of publicly traded assets in US equity funds.

It is also the case that a key source of these flows is retirement-linked passive investment as index funds have been sold as a cheap and convenient way to invest.

But there is also the reality of retail investors buying leveraged ETFs engaged in passive investment strategies.

Reuters reported in April that leveraged equity funds received inflows of US$10.95bn in April as of 21 April, surpassing a 5-year high of US$9.2bn recorded in March (see Reuters article: “Leveraged equity ETFs popular as investors bet on market recovery”, 24 April 2025).

Assets in leveraged equity ETFs traded in the US now total an estimated US$105bn.

The above reminds this writer of comments made by value investor David Einhorn of Greenlight Capital in February last year when he stated that he viewed the US stock market as “fundamentally broken” as a result of the combination of passive investing and algo-related trading (see Bloomberg article: “Einhorn Says Markets ‘Fundamentally Broken’ By Passive, Quant Investing”, 8 February 2024).

Einhorn stated that passive investors “have no opinion about value”, while quants base their trades on very short-term price moves like, as noted by Einhorn, “what is the price going to be in 15 minutes” (!)

This is the scary (to this writer) reality of the current US stock market and has been for some time.

Hyperscaler Results Are Critical to S&P 500 Returns

This is why the issue of whether Big Tech will be able to monetise its prodigious spending on the AI arms race is at least as important for the US stock market, if not more so, than the state of the US economy given Big Tech’s continuing dominance of the S&P500.

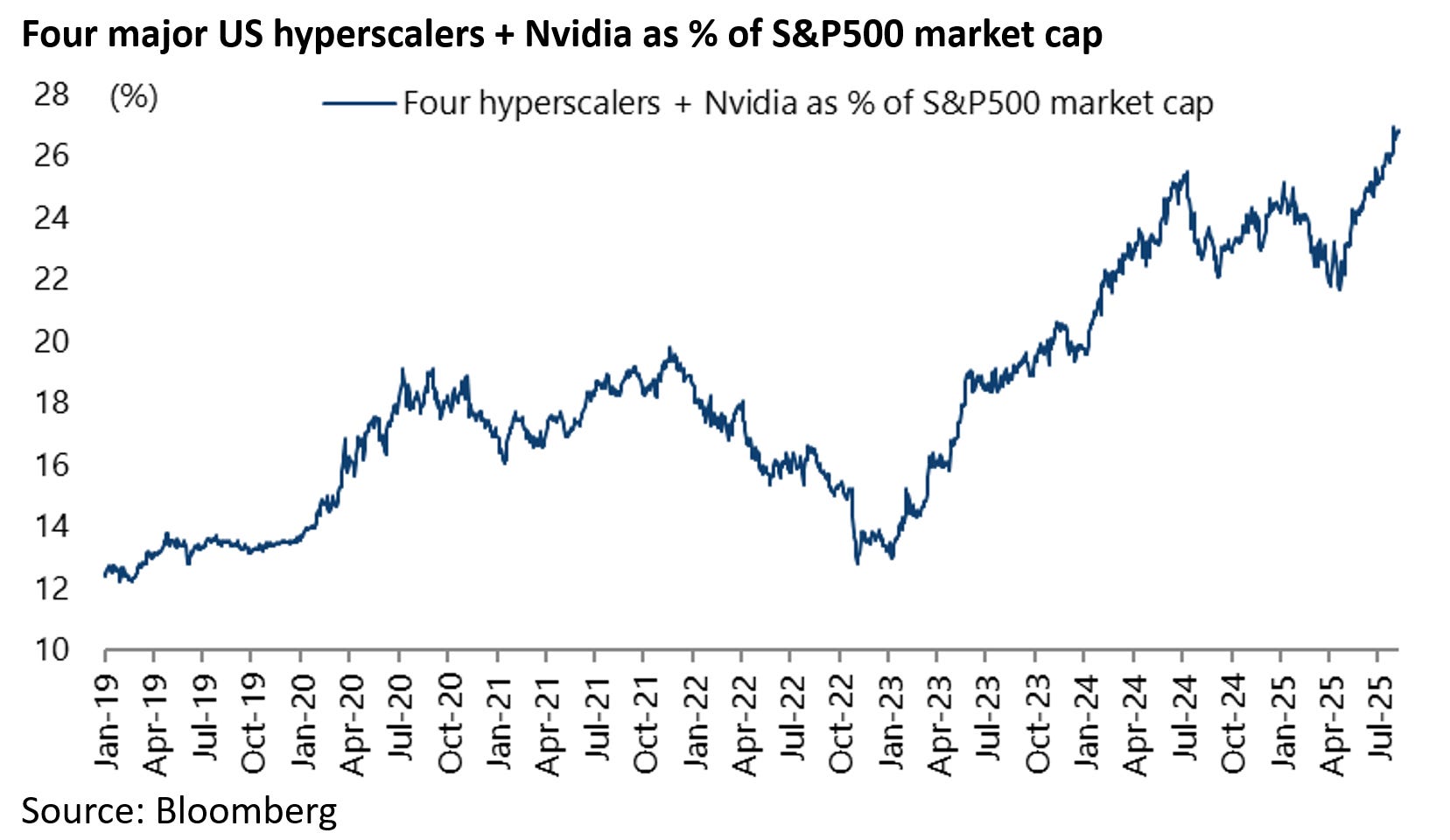

On this point, the Magnificent-7 stocks are now less relevant when it comes to the AI capex trade than the four hyperscalers and Nvidia.

These five stocks accounted for a record 26.9% of S&P500 market capitalisation at the end of July and now represent 26.8%.

They have also accounted for 49% of the gains in the S&P500 since the AI thematic entered the stock market with the announcement of Microsoft’s investment in ChatGPT maker OpenAI in January 2023 which is when the AI capex arms race really got under way.

The issue of monetisation of AI capex, or the lack thereof, came to the fore with the DeepSeek moment in January which has raised the risk that large language models on which so much money is being spent will become commodities, as previously discussed here (Own the AI Picks and Shovels, Not the Models, 9 April 2025).

But investors have completely forgotten about that for now as they have celebrated the recent surging capex announcements by the hyperscalers and others as they pursue the dream of so-called AGI.

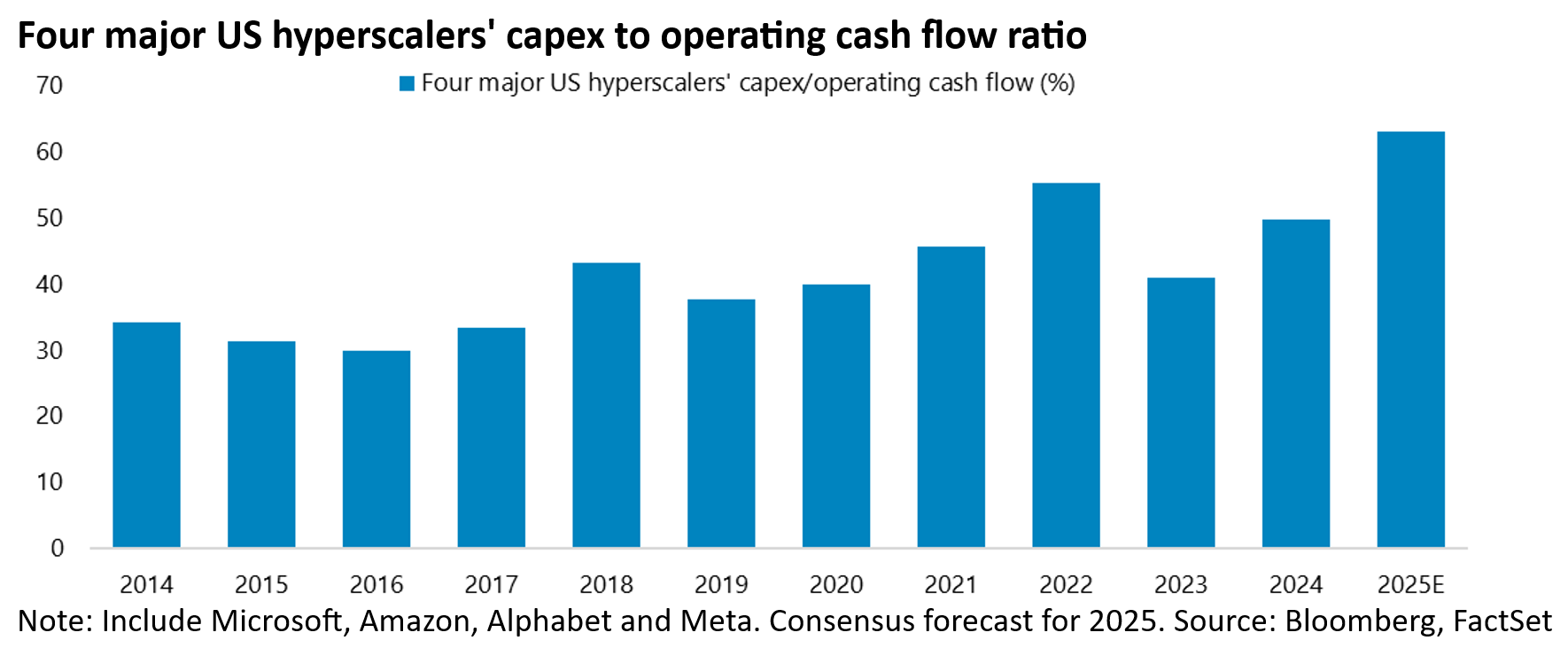

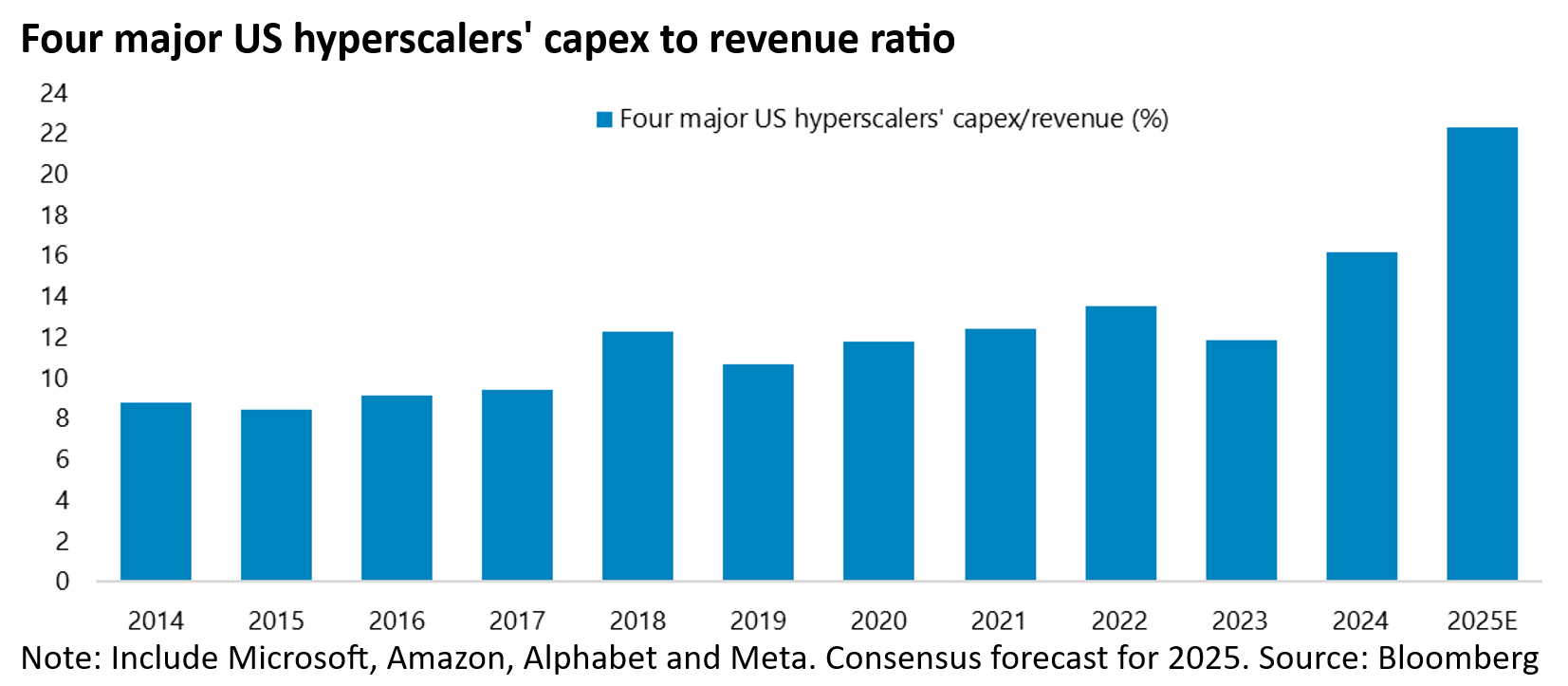

The four hyperscalers are now guiding to spend about US$350bn in capex this year and perhaps more than US$400bn next year based on the latest guidance and consensus estimates.

The projected capex of the four hyperscalers this year amounts to 63% of forecast operating cash flow and 22.3% of forecast revenues, up from 41% and 11.8% in 2023.

These are huge numbers.