Don't Let the AI Trade Distract you from Opportunity in the Land of the Rising Sun

Author: Chris Wood

Financial markets continue to ignore continuing historical geopolitical developments and maintain a near all-consuming focus on AI.

As estimates for AI capex soar, the key issue remains when investors start to worry about the returns or the lack of them from all this spending with the next test the forthcoming earnings seasons.

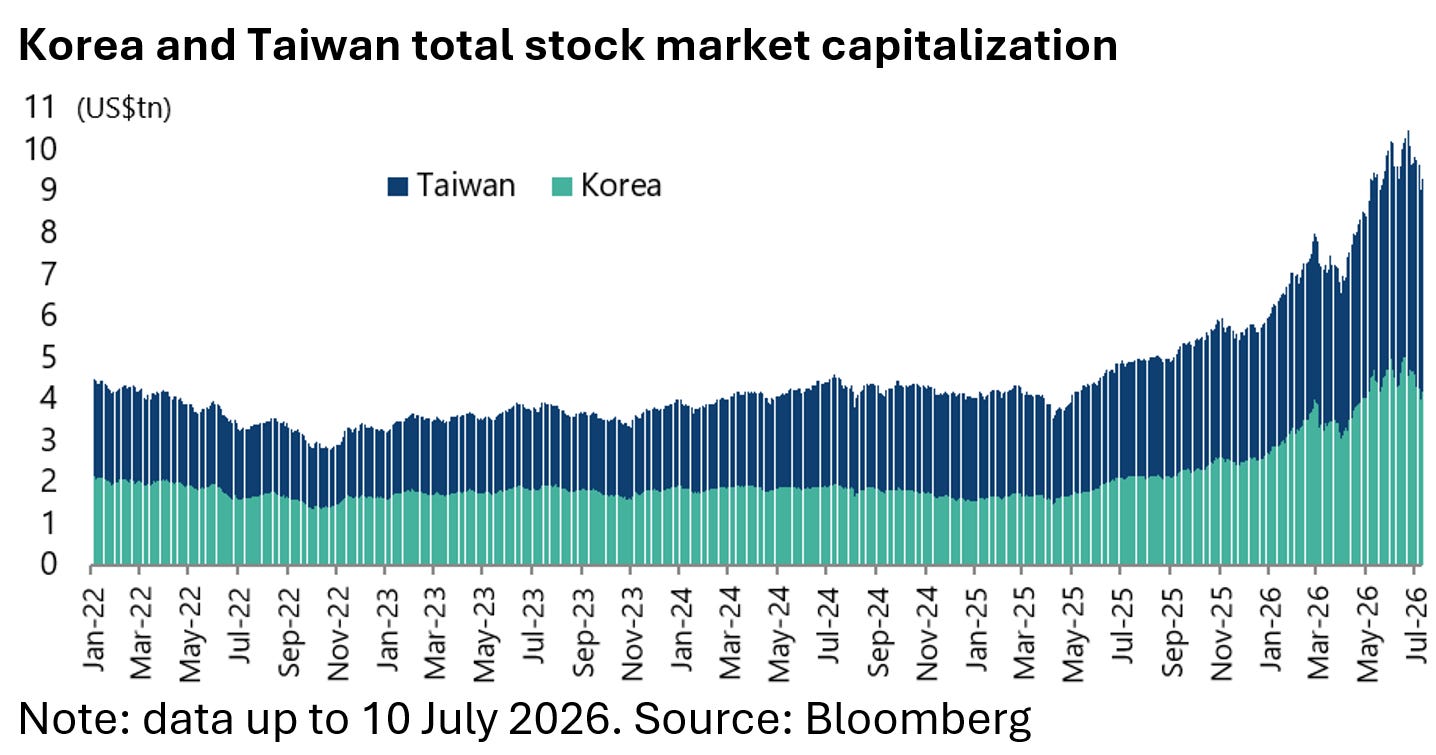

For so far virtually all the money in the AI trade has been made by the picks and shovels plays which has amounted, in significant part, to a massive redistribution of wealth from America to North Asia.

This is reflected in the increased capitalisations of the Korean and Taiwanese stock markets.

The combined stock market capitalisations of Korea and Taiwan have almost tripled from US$3.2tn at the start of 2023 when the AI story kicked off in stock markets to US$9.3tn, though down from a peak of US$10.5tn on 22 June, according to Bloomberg.

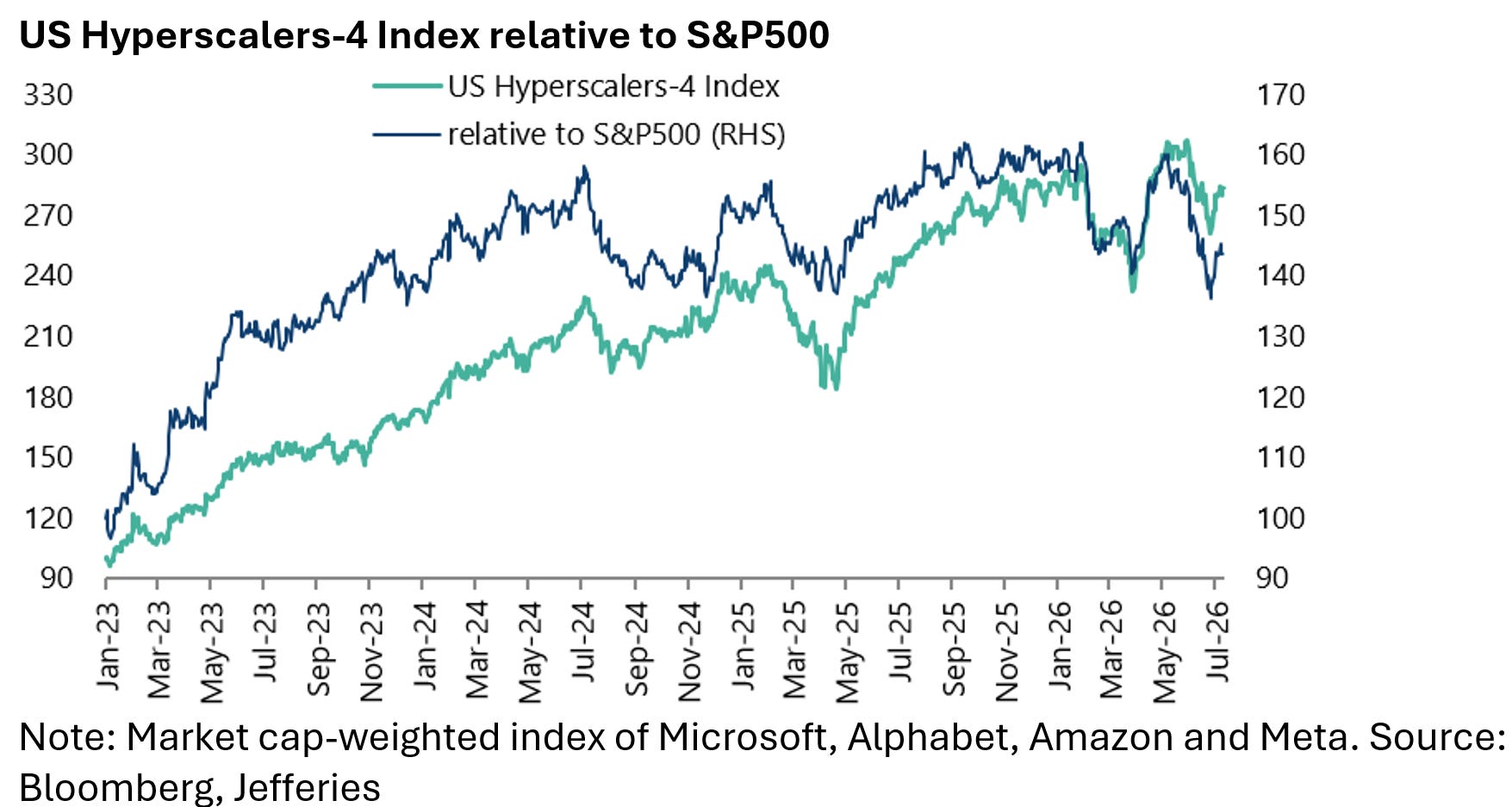

This is why the absolute and relative performance of the hyperscaler stocks need to be monitored closely.

While they have underperformed of late against the S&P500, they have not yet sold off aggressively on investor concerns about a lack of monetisation.

But that risk is growing with Alphabet, Amazon, Meta and Microsoft now down 13%, 12%, 16% and 31%, respectively, from their all-time highs reached in May or, in the cases of Microsoft and Meta, in July and August last year.

This has translated into growing relative underperformance of the hyperscalers against the S&P500 even as the S&P500 is still trading near an all-time high.

Thus, the hyperscalers have underperformed the S&P500 by 10% since early May and are down 7.6% from the peak reached in late May on a market cap-weighted basis.

As for the S&P500, it is now only 0.6% below the peak reached on 2 June.

Investors Continue to Ignore Iran’s Potential Impact on Bond Yields

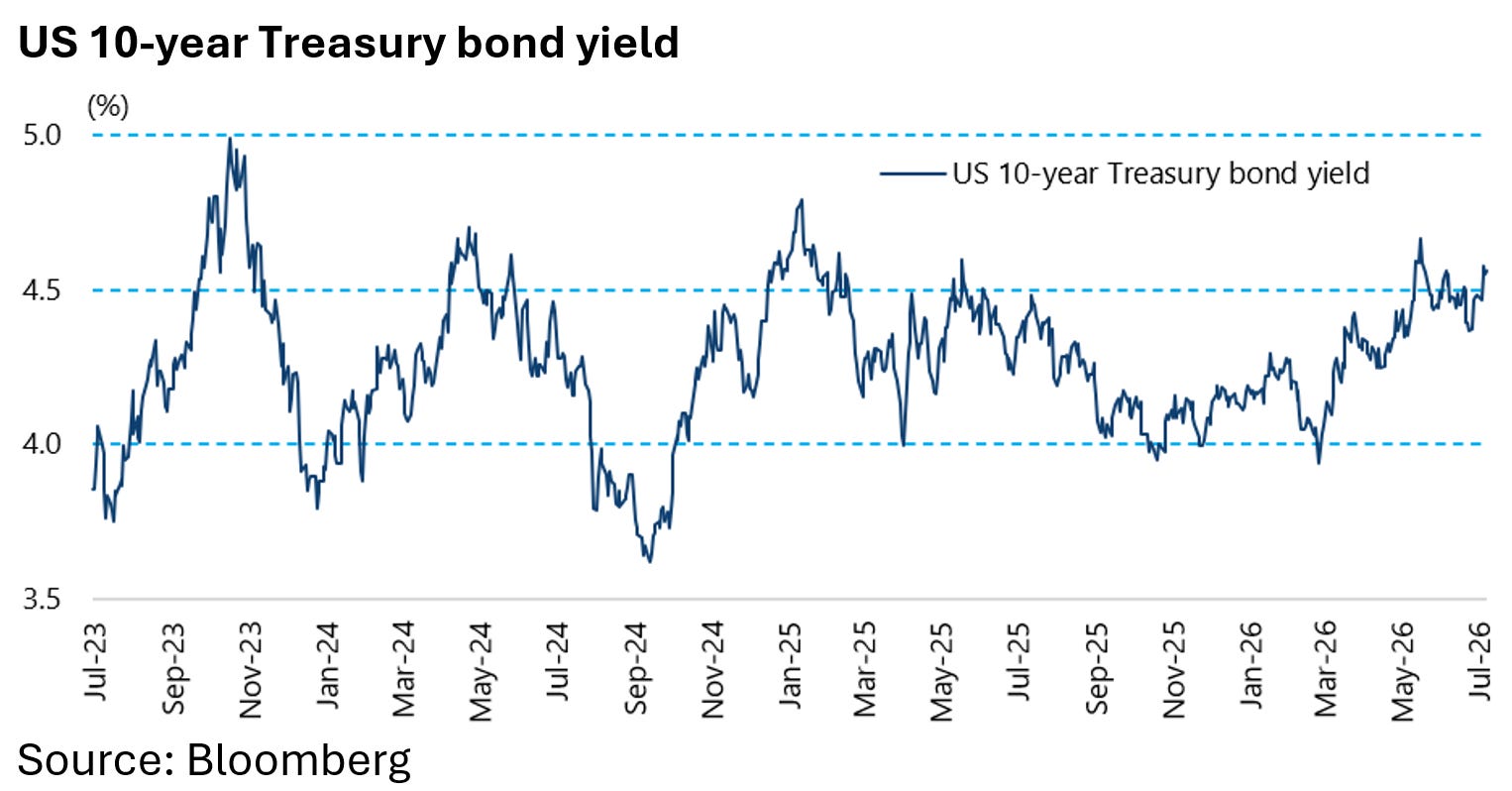

Meanwhile with the latest revival of tensions with Iran, where geopolitics could matter for markets is the bond market where the ten-year Treasury bond yield remains the most important price in world markets.

The ten-year yield has now broken back above the 4.5% level, at 4.56%.

Indeed, how it behaves is probably more important than what the new Fed Chairman says or the FOMC does.

A clear break above the 4.5% level should be viewed by equity investors as a warning, more akin to a yellow signal at a traffic light, but nothing more detrimental given the for now continuing powerful earnings momentum in the US driven by AI capex.

But a more decisive move above 5% would be more like a red traffic light. It would also make it hard for the Fed to avoid renewed monetary tightening even though the base case for now is that the Fed remains on hold.

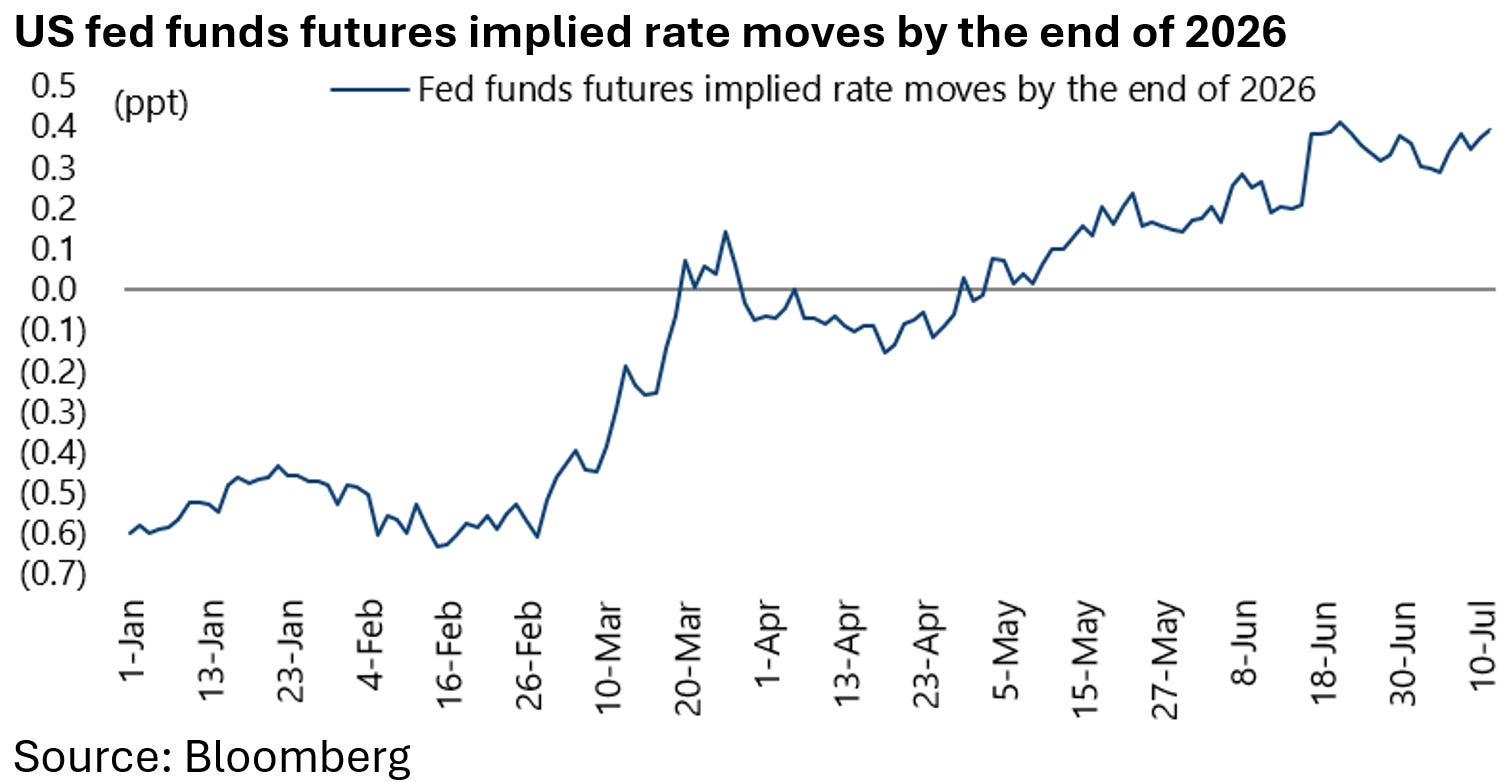

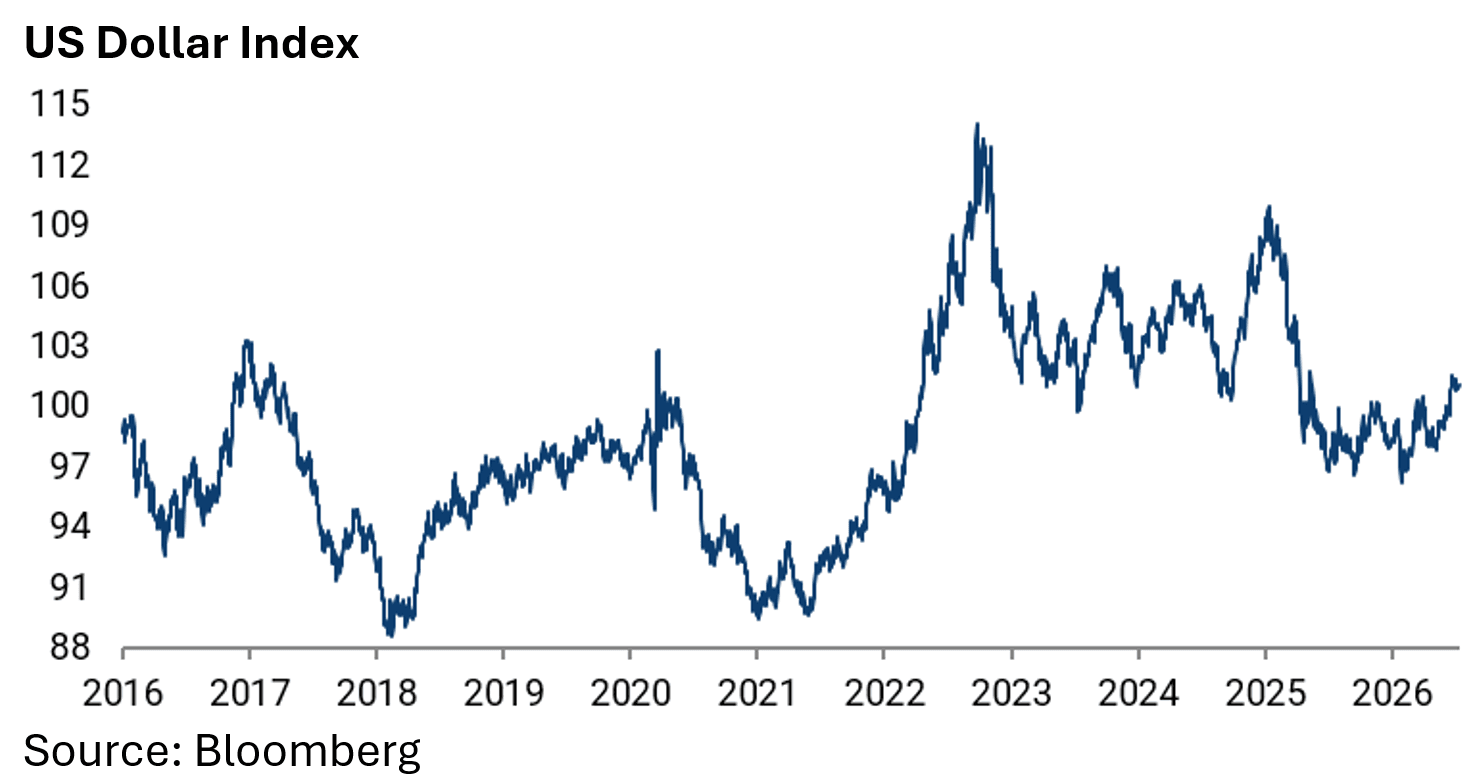

Higher Treasury bond yields and anticipated renewed Fed tightening, with money markets now expecting 39bp of rate hikes this year compared with 61bp of easing as recently as late February, may well have triggered a short-term bid for the dollar.

In fact the US dollar index is up 5.8% since late January.

But sooner rather than later we think higher yields will become dollar bearish because markets will refocus on America’s still deteriorating fiscal position which in turn will lead to renewed focus on the US dollar debasement trade.

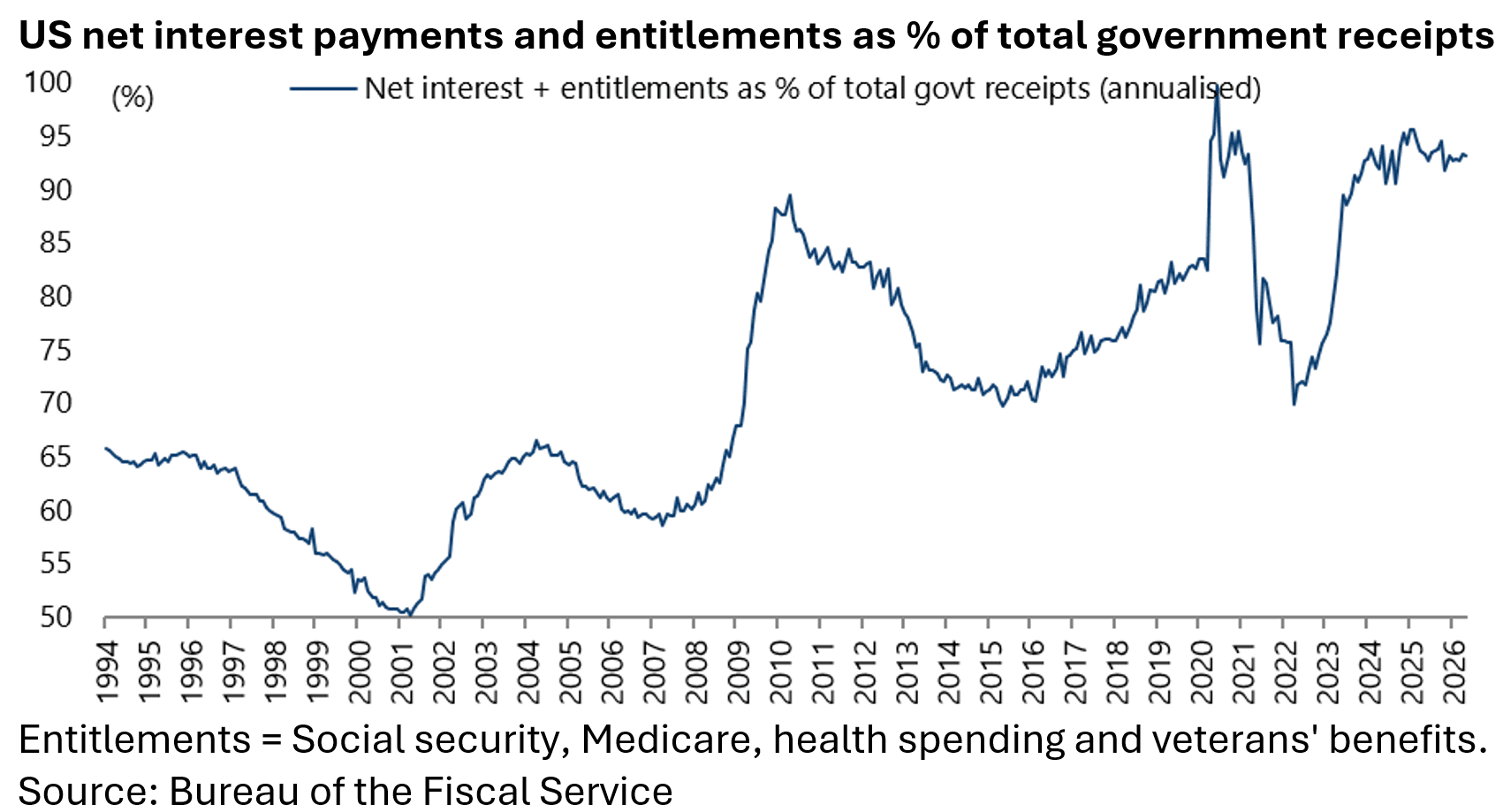

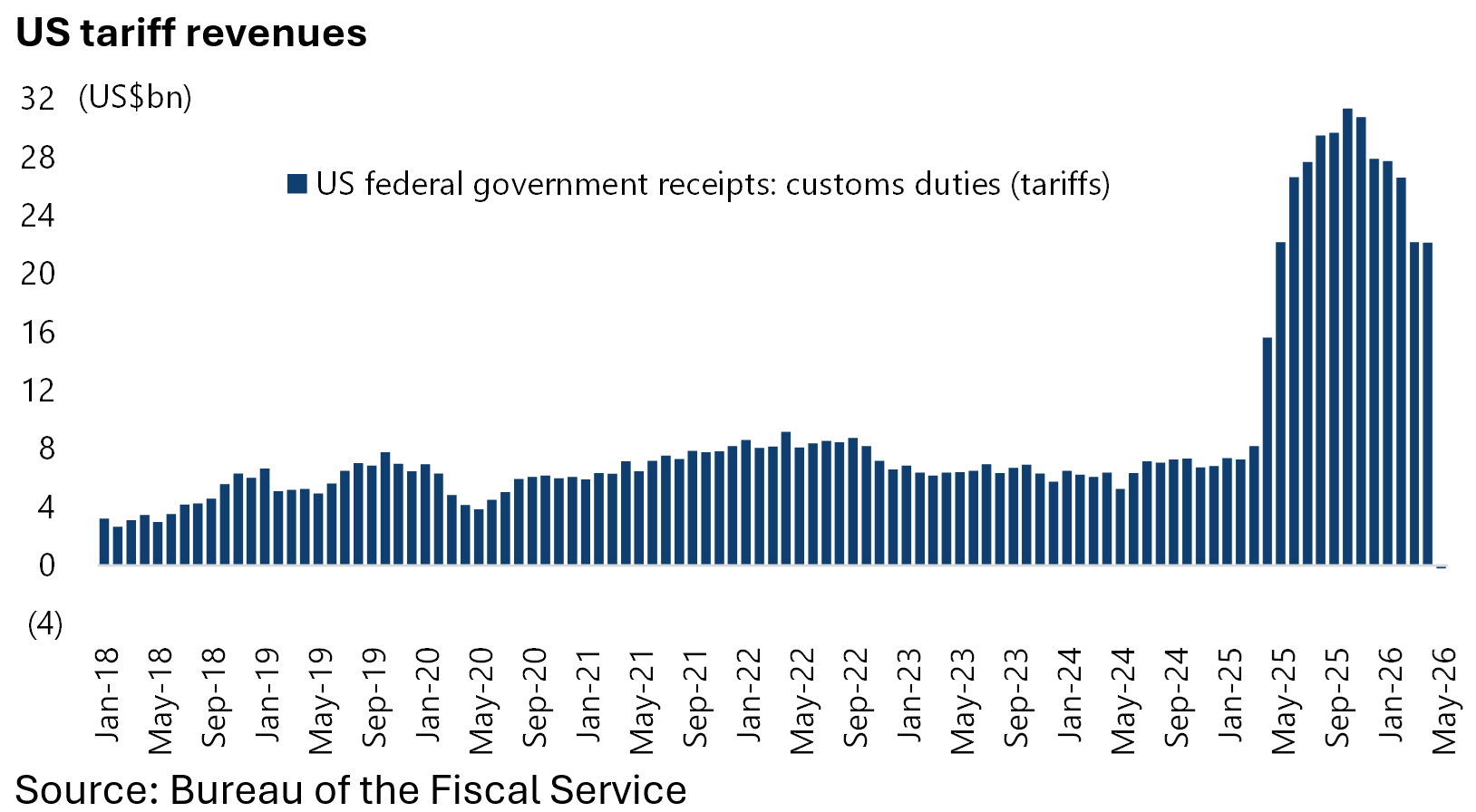

US net interest payments and entitlements were still running at 93.1% of total federal government receipts in the 12 months to May despite the increase in tariff revenues over the past year and more, and those revenues are now falling, having peaked at US$31.35bn in October 2025.

Indeed, tariff revenues declined to a negative US$42m in May as the US Treasury refunded US$21.97bn in tariff revenues previously collected which were declared illegal by the Supreme Court in February.

This more than offset gross tariff collections of US$21.93bn in May.

For Now We Recommend Focusing on the Nikkei, Not the S&P.

Meanwhile, if the arrival of a new Fed chairman is an important event, and Kevin Warsh sensibly maintained a more hawkish line than expected in his first FOMC meeting in June since the obvious risk is that the markets will test him, this writer’s view remains that the monetary policy debate is most important in Japan at present given that the yen has just broken through the key 160 level. The yen is now Y162/US$.

The Nikkei 225 Index has Outperformed the S&P 500 by 20% over 5 year, even including the weakening of the Yen. In the paid section of today’s research note we lay out all the economic factors that are likely to drive continued outperformance of the Japanese stock market over the medium term.

Keep reading with a 7-day free trial

Subscribe to Grizzle Research & Quant to keep reading this post and get 7 days of free access to the full post archives.