China's Energy Endgame: Is Battery Storage Making LNG and Nuclear Obsolete?

Author: Chris Wood

This writer is no energy expert.

But it is becoming increasingly apparent that energy could become the key factor in terms of determining not only the long-term winner in AI but also geopolitics in general. And this is not a reference to the current focus on Iran.

In this respect, there have been some interesting comments made on the AI thematic in recent months as it relates to energy. The first came from Nvidia chief executive officer Jensen Huang when he commented on the sidelines of a Financial Times conference last November that “China is going to win the AI race”.

The Nvidia boss, in particular, highlighted lower energy costs citing Chinese energy subsidies that made power more affordable for local tech companies allowing them to run Chinese alternatives to Nvidia’s AI chips. Huang actually said: “Power is free” (see Financial Times article: “Nvidia’s Jensen Huang says China ‘will win’ AI race with US”, 6 November 2025).

The second comment that caught attention came from Microsoft CEO Satya Nadella when he said in a podcast the same month that chip stockpiles were building up because Microsoft did not have enough power for some of their data centres.

In an interview on the YouTube channel Bg2 Pod on 1 November alongside OpenAI CEO Sam Altman, Nadella said: “The biggest issue we are now having is not a compute glut, but it’s power”.

These comments have caused concerns amongst tech investors about an inventory build for Nvidia and the rest of the AI “picks and shovels” plays as a result of this energy constraint.

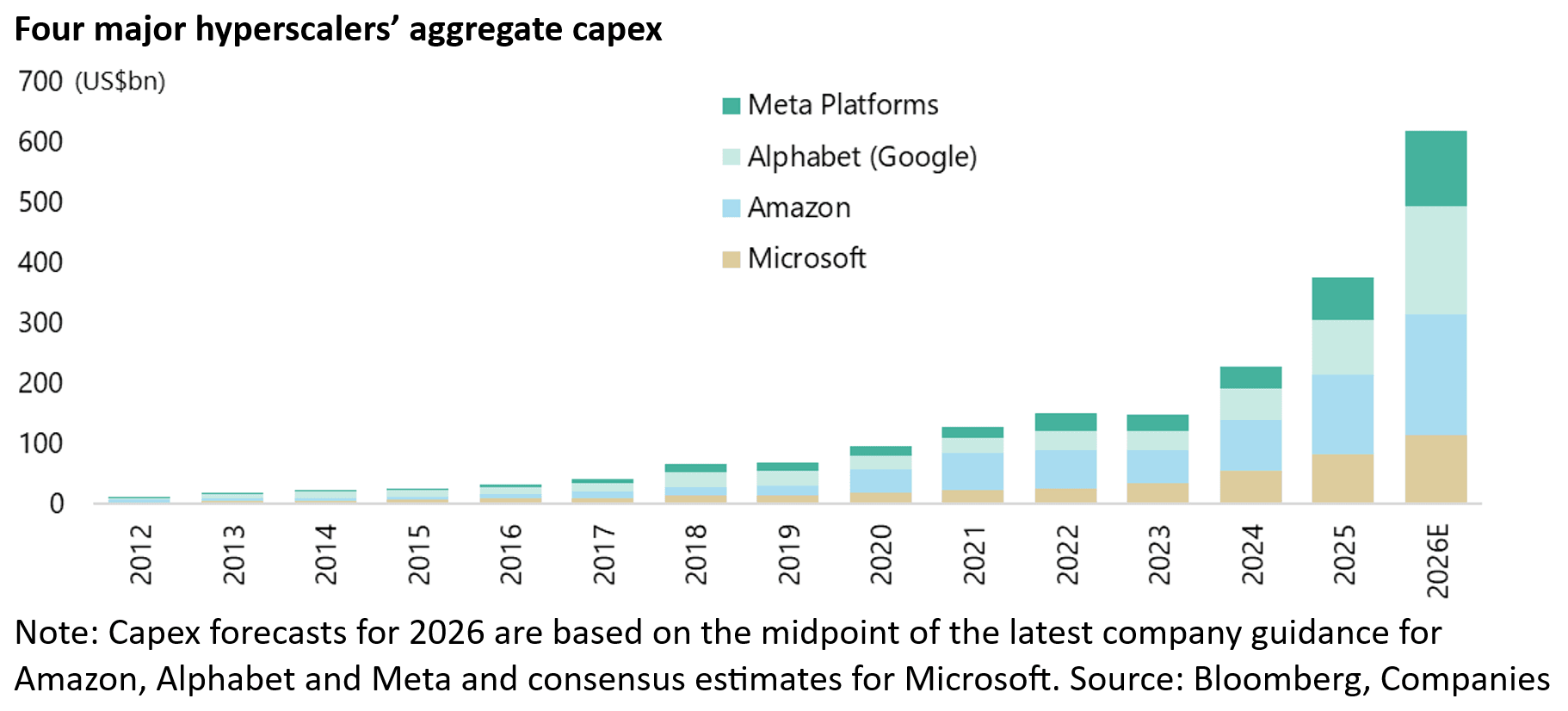

These tactical concerns are understandable given the ever rising forecasts of AI capex. The four major hyperscalers’ aggregate capex is projected to be US$620bn this year.

What if China Will No Longer Need New Nuclear or LNG

But the real strategic issue is why America has a power constraint relative to China.

And the answer seems to be that the amazing progress made in battery storage technology means that solar has become cheaper than coal in China even before the recent Iran-triggered rise in the oil price.

Or to be more precise, battery storage technology and the associated rapid fall in storage, as well as solar photovoltaic prices, have made “intermittent” solar and wind power, paired with battery storage, a competitive alternative to coal-based power.

Or in other words, the problem of having a reliable source of baseload, or readily available power, is close to being solved. Baseload refers to the minimum amount of electricity required or delivered by an electric grid at any given period of time.

If this is indeed the case then it must be asked why LNG or indeed nuclear will be required at all as energy sources going forward.

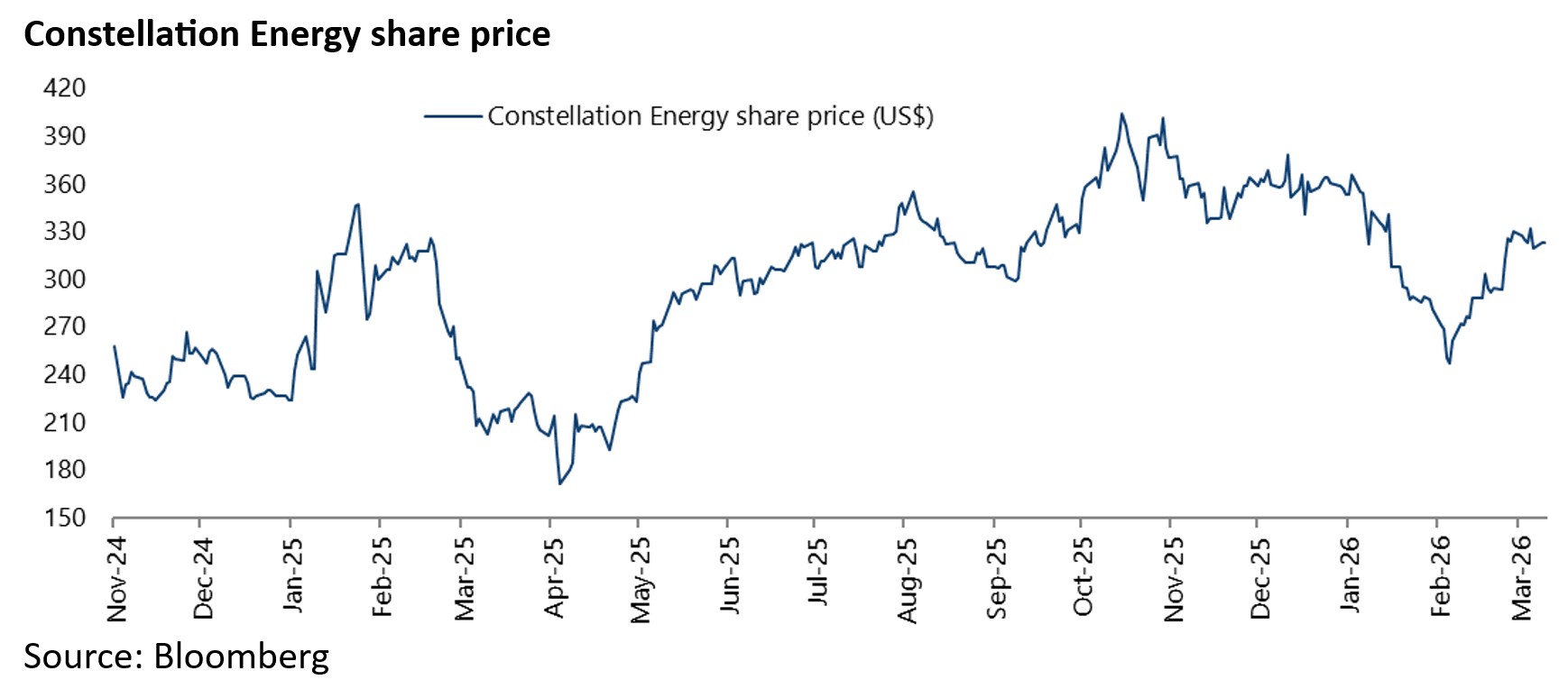

American related energy stocks have rallied in recent months on the perceived urgent need to build up energy sources to power all these data centres with some utilities turning into growth stocks.

See, for example, the chart below of Constellation Energy

But the quickest and cheapest way to address this problem for the US is surely to import the Chinese technology.

But that requires a realisation that technological disruption has arrived in the energy space.

In this respect, the narrative as regards solar and renewables has definitely been damaged in the West in recent years by the self-serving virtue signaling symbolised by the ESG movement and the related association of renewables with climate change obsessions and green politics in general.

The Trump administration has had no time for these woke obsessions and clearly the arrival of Donald Trump at the White House has triggered a full-scale retreat from such virtue signaling, with the only remaining proponents of these positions the true believers.

But the point to understand for the Trump administration, or indeed investors, is that the Chinese have been focused on improving battery storage technology not because of a green agenda but because it has the potential to remove China’s dependence on imported fossil fuels in a cost effective manner.

It is also, importantly, a huge advantage when it comes to AI.

Two key inputs are required for the development of AI.

That is power and compute. And the evidence increasingly suggests that China is far further ahead in energy than the US is ahead in compute.

On the latter point, Huang’s comments about China winning the AI race came after the Nvidia boss failed in his efforts to persuade Donald Trump to discuss in his meeting with President Xi Jinping last October a deal whereby America would allow the export of Nvidia’s Blackwell chips to China.

The idea appears to have been that this would be offered in exchange for Beijing relaxing restrictions on exports of rare earth materials.

Such hopes also drove a 15% rise in Nvidia’s share price in the five days prior to the meeting on 30 October in Korea.

A recommended article in the Wall Street Journal at that time reported that Trump backed off the proposed deal, as he “prepared to meet Xi”, because of comments from the likes of Secretary of State Marco Rubio that allowing the export of the Nvidia Blackwell chips would threaten US national security.

As a result, faced with “with nearly unified opposition from his top advisers”, according to the article, Trump decided not to discuss the advanced Nvidia chips during the meeting (see WSJ article: “Trump Aides Sank Nvidia Push To Export AI Chips to China”, 4 November 2025).

The above account reads very true to this writer.

Rare Earth’s Give China Far More Leverage Than America’s AI Chips

It is another example of how the conceptual vacuum symbolised by the 47th American president means he is vulnerable to making sudden changes in policy.

Instinctively, his views are contrary to the national security lobby, be it on Ukraine or the export of advanced semiconductors to China, but he still succumbs to their concerns.

The reality, of course, is what Nvidia’s Huang has doubtless been telling him.

That is that the semiconductor controls introduced by the Biden administration in October 2022 have backfired badly and are contrary to the US national interest as long argued here.

This is not only because they have deprived America’s tech companies, such as Nvidia, of their largest customer.

But also because they have massively incentivised China to develop its own semiconductor supply chain.

And it is clearly now the all-consuming focus of President Xi to end China’s dependence on Nvidia chips as soon as possible.

On this point, Reuters reported late last year that Beijing has issued guidance requiring all new data centre projects that have received any state funds to use only domestically developed AI chips (see Reuters article: “China bans foreign AI chips from state-funded data centres, source say”, 5 November 2025).

In this respect, it would have been interesting to see how the Chinese leader would have reacted if Trump had suggested the Blackwell deal advocated by Huang.

But for now it seems increasingly to be the case that China’s leverage on rare earths is much greater than America’s on semiconductors.

Meanwhile, if there is growing recognition in America of the energy deficit, there is much less focus on why America is behind which is obviously because it is committed to yesterday’s technology.

On that point OpenAI wrote an open letter to the White House Office of Science and Technology Policy (OSTP) last October highlighting how the PRC is way ahead of the US and stated that the OSTP should prioritise closing the “electron gap” by setting up an ambitious national target of building 100GW a year of new energy capacity to “fuel American AI dominance”.

If this is a seemingly ambitious target, it is still minimal compared with China’s progress in this area.

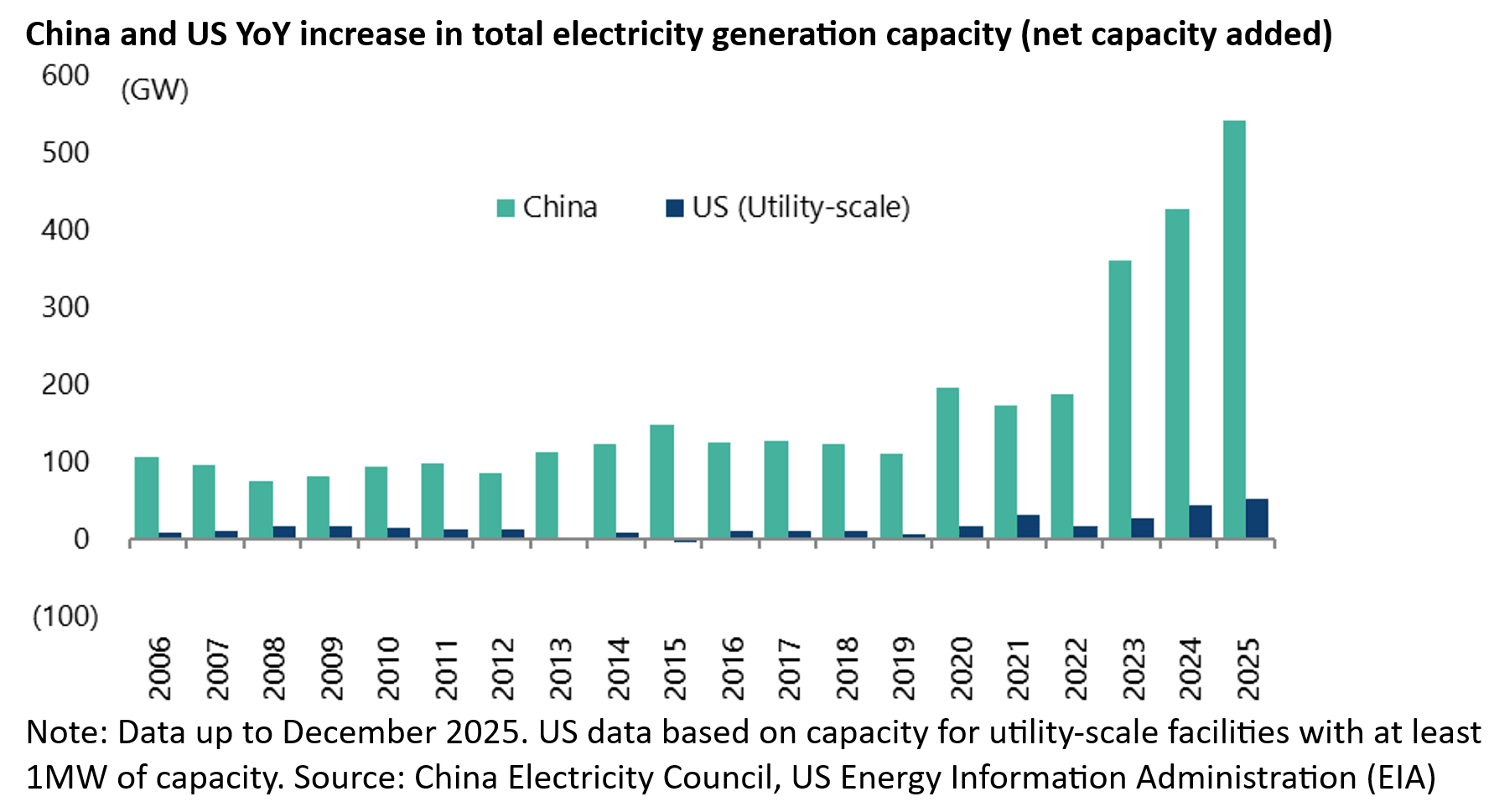

The OpenAI letter noted that China added 429GW of new power capacity in 2024, which was more than one-third of the entire US grid and more than half of all global electricity growth.

While China added a further 542GW of power generation capacity last year, compared with a net addition of 50GW in the US where total capacity was only 1,281GW at the end of 2025.

Perhaps even more importantly, China also added 378GW of solar generation capacity in 2025 - greater than the entire installed solar capacity in the US of about 274GW.

While China’s total power demand increased by 505TWh (Terawatt hours) in 2025, power generation from solar (336TWh) and wind (138TWh) sources increased by 474TWh in the same period.

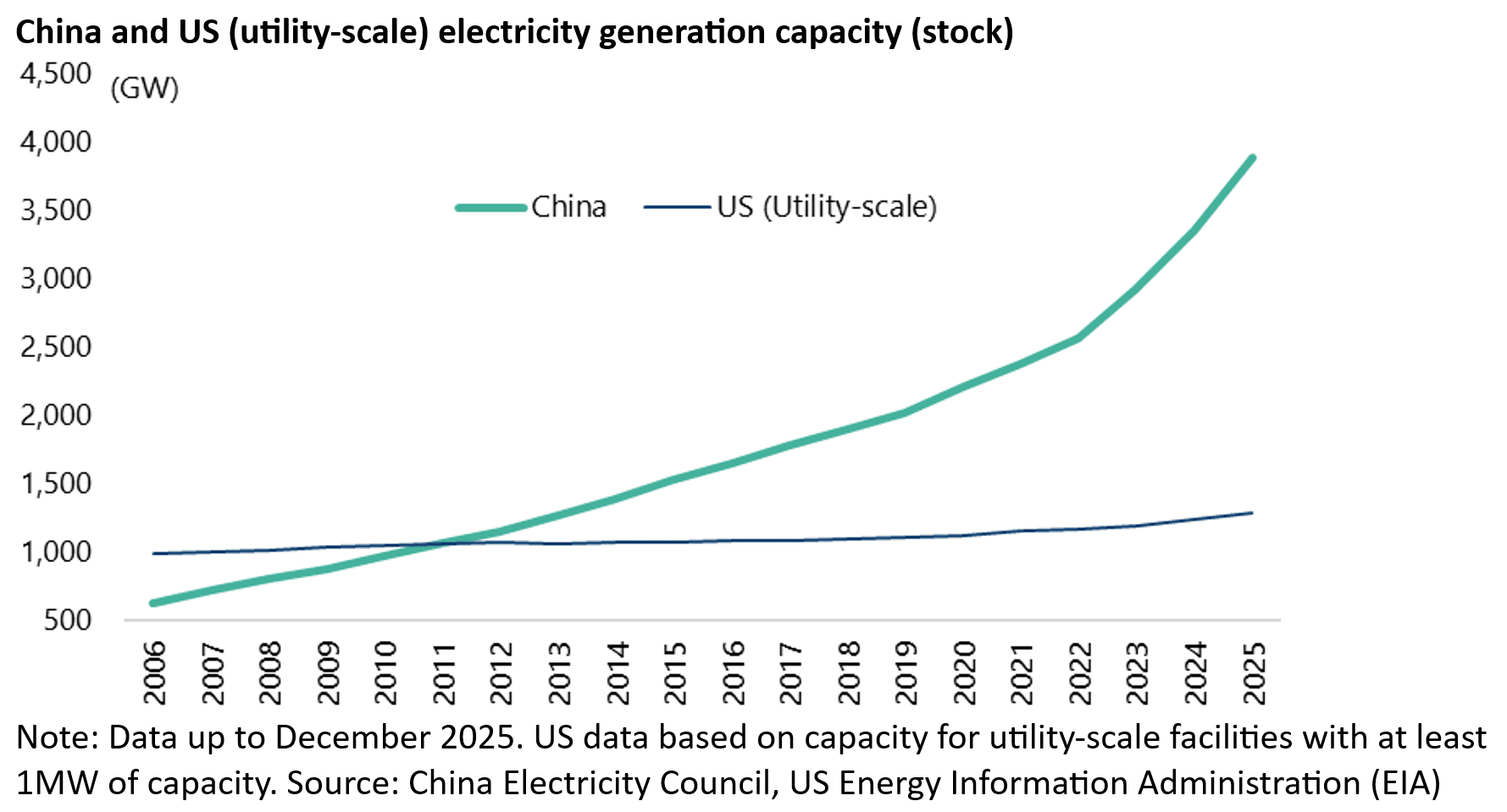

Meanwhile the dramatic growth in Chinese electricity generation capacity, in terms of both flow and stock, are shown in the two charts above.

The development of a solar based generation system augmented by battery storage, and the key word is system, raises the real possibility that the US is at risk of losing energy dominance to China.

This is a very big deal in the context of which recent tactical victories for America, such as getting the Europeans to buy more expensive LNG by stopping them buying cheap Russian energy, are not very important at all.

This is where the puck is headed. Graphite demand for Battery Energy Storage System (BESS) grew 44% in 2025. The full report -

https://oculusresearch.substack.com/p/graphitethe-elephant-in-the-power

There are solutions (fuel cells) coming to the market which can scale to 20-25 GW per annum over the next 5 years which will help the US level the energy playing field. Fuel cells cost are falling by 10 pct per year and have very attractive economics relative to gas turbines for carbon capture. Most of the hyperscalers have signed on and have orders in to test the solution at scale ie in the 100s of MW per site. Once they validate it in the field over the next 12 months, my guess is everyone will hear about it. Never bet against US innovation - we always win