China Needs America Less Than You Think

Author: Chris Wood

Faced with The Donald Trump-triggered tariff war in recent weeks, China has become more focused on stabilizing domestic demand even if it has not been panicked into aggressive stimulus.

Thus, in late March China unveiled a “special action plan to boost consumption” with 30 policies covering eight areas.

The plan, jointly issued by the General Office of the Communist Party of China Central Committee and the General Office of the State Council, aims to stimulate domestic demand across the board. One aspect of this is to increase job security, pensions and social security.

True, these measures are not quantified. But such a policy should help stabilise consumer confidence and lead to a reduction in the household savings rate in the long term.

Still, if the government is increasingly demonstrating that it is prioritising domestic demand, when it comes to Chinese consumer confidence, it is also in part a question of time proving the best healer.

In this respect, there remains an element of post-traumatic syndrome following three years of on-and-off Covid-triggered lockdowns between 2020 and 2022.

It is certainly the case that the Chinese do not need handouts, given the enormous amount sitting in Chinese bank deposits, up Rmb79.2tn (US$10.4tn) from Rmb81.3tn (US$11.7tn) at the end of 2019 to Rmb160.5tn (US$22.1tn) at the end of March 2025.

The household savings rate is currently running at 31.8% of disposable income.

This high savings rate is one key reason why Washington does not have the leverage it thinks it has in the trade war which also explains why Trump in practice is progressively backing off the tariff agenda.

Another is that China’s exports to the US only account for 2.7% of its GDP.

While as regards third party countries, China is in most cases a more important trade partner than America.

A total of 143 or 71% of countries traded more with China than with the US in 2024, while 107 or 53% of countries traded more than twice the amount with China that they trade with the US, based on IMF’s data on international trade in goods by partner countries.

This compares with 22% and 11% respectively back in 2001 when China joined WTO.

China's is Quickly Becoming the World's Industrial Supplier

The other aspect of the China investment story, aside from the domestic economy getting less bad, remains dramatic advances in high-tech areas, a development long understood by Chinese specialists but which only really came to global investors’ attention with the DeepSeek moment in late January.

For example, China is increasingly competitive in previous high-tech sectors dominated by the likes of Japan and Korea.

This is not just EVs or batteries but also robots and automation.

Thus, China accounted for 51% of global industrial robot installations in 2023, with 276,288 new units installed, according to the International Federation of Robotics.

By contrast, there were “only” a combined 143,492 units installed in the US, Japan, Korea, and Germany in 2023, accounting for 27% of the total annual installation.

The Ministry of Industry and Information Technology announced back in 2023 a plan to position humanoids as a strategic tool for economic growth by 2027.

Chinese companies in this field raised Rmb5.4bn (US$769m) in 2023 and another Rmb7bn (US$997m) in the first half of 2024.

All of this is an endorsement of President Xi Jinping’s strategy of focusing on “new productive forces” and of the original “Made in China 2025” agenda launched back in 2015.

The Chinese government has supported this shift by directing banks to provide equity-like loans to strategic industries.

Thus, medium- and long-term loans to the industrial sector rose by 12.6% YoY in 4Q24.

This approach has enabled manufacturers to borrow from the earlier playbook of sacrificing profitability for scalability.

The result has been brutal domestic competition.

But the players which emerge from this and move into global markets are producing at levels of quality and cost that make them among the most competitive globally, with BYD in EVs and CATL in batteries perhaps the best examples.

US Energy Prices and Production on the Decline

Then there is the issue of energy.

The recent weakness in the oil price is of note, with the Brent crude oil price falling of late briefly below the US$60/bbl support level.

Weakness in part triggered by Saudi Arabia’s recent decision to increase production which seems designed to appease the 47th American president.

Saudi Arabia decided on 3 May to increase OPEC+ production by a further 411,000 barrels per day in June.

President Trump is due to visit Saudi and other Arab countries this week.

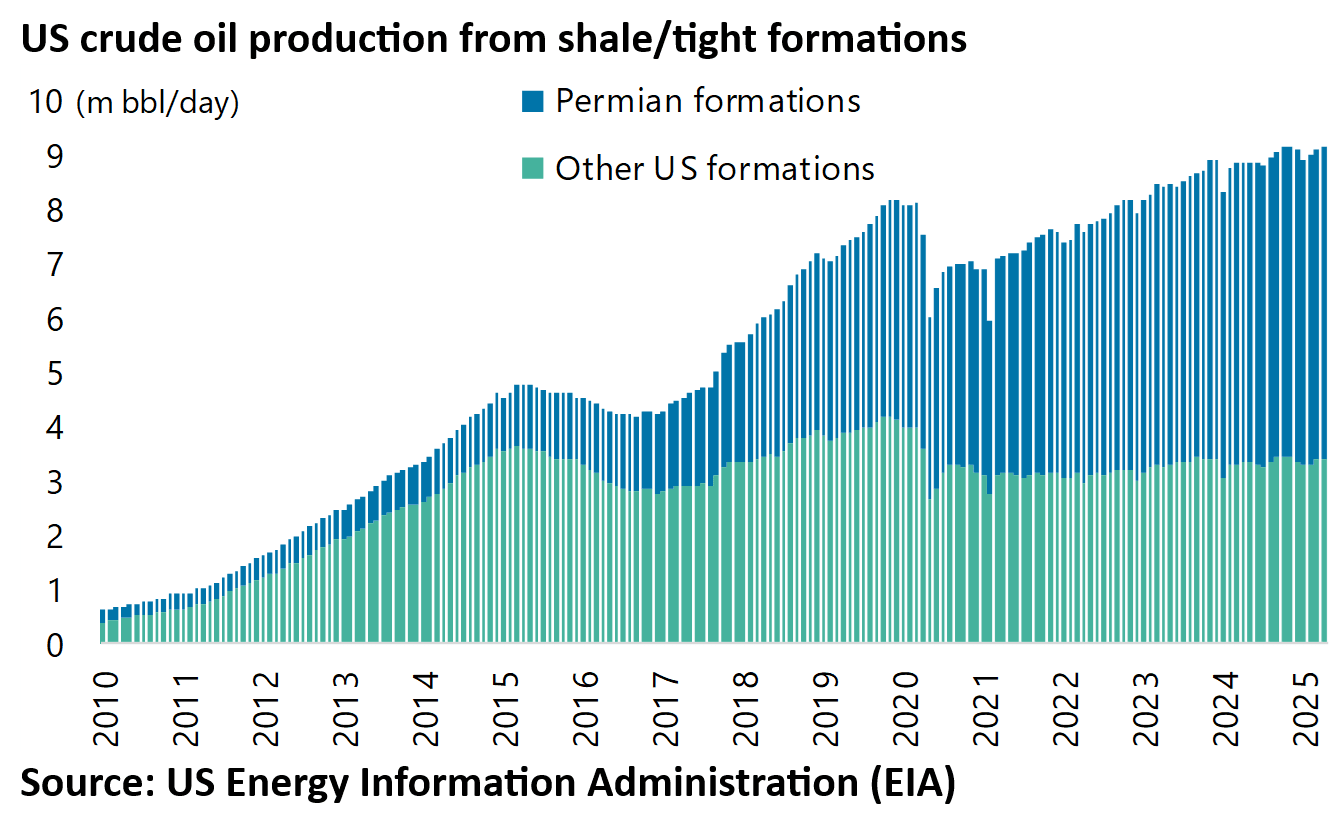

This price action is also in spite of the growing evidence that shale production has peaked.

Thus, US shale oil production peaked at 9.17m barrels/day in November and has since declined by 0.2% to 9.15m bbl/day in April, according to the Energy Information Administration (EIA).

Excluding the largest Permian shale region, shale oil production in the other US formations peaked at 4.19m bbl/day in October 2019 and has since declined by 18% to 3.43m bbl/day in April.

While production in Permian peaked at 5.73m bbl/day in December and was 5.72m bbl/day in April

Solar Just Hit Price Parity with Coal in China

Staying on the energy theme, this writer’s attention was recently caught by a prediction that battery storage plus solar will become cheaper than spot coal power in China by the end of this year, thanks to the continuing drop in battery prices.

This is of huge potential interest, as China is the testing ground for increasing penetration (or dominance) of renewables in what has been a coal-dominated energy system. Energy storage is so important because storage prices will determine the success of renewables.

Battery energy storage systems (BESS) now account for one-quarter of global battery shipments, up from 5% in 2019, with CATL the dominant player.

In this respect, China is the key country to monitor since it is likely to be the first example of a coal-dominated large producer hitting a large solar-powered free energy system.

On this point, China has already, from this year, made storage attachment mandatory for any new solar installation.

Indeed, in the very long run, battery storage has the potential to make coal obsolete even potentially without any sun or solar.

In this respect, while China has a bad reputation with the green crowd for its still increasing coal production,

the reality is that it has also been expanding renewables more aggressively than anyone for the practical reason that it is likely to end up cheaper if storage technology can deliver as already discussed.

This is a reminder, if it was needed, that the renewable story does not need the likes of ESG or net-zero commitments to deliver if it is cost-competitive.

Meanwhile, the Trump-triggered stampede out of ESG and net-zero commitments continues.