Canary, Meet Leveraged Loans

Author: Chris Wood

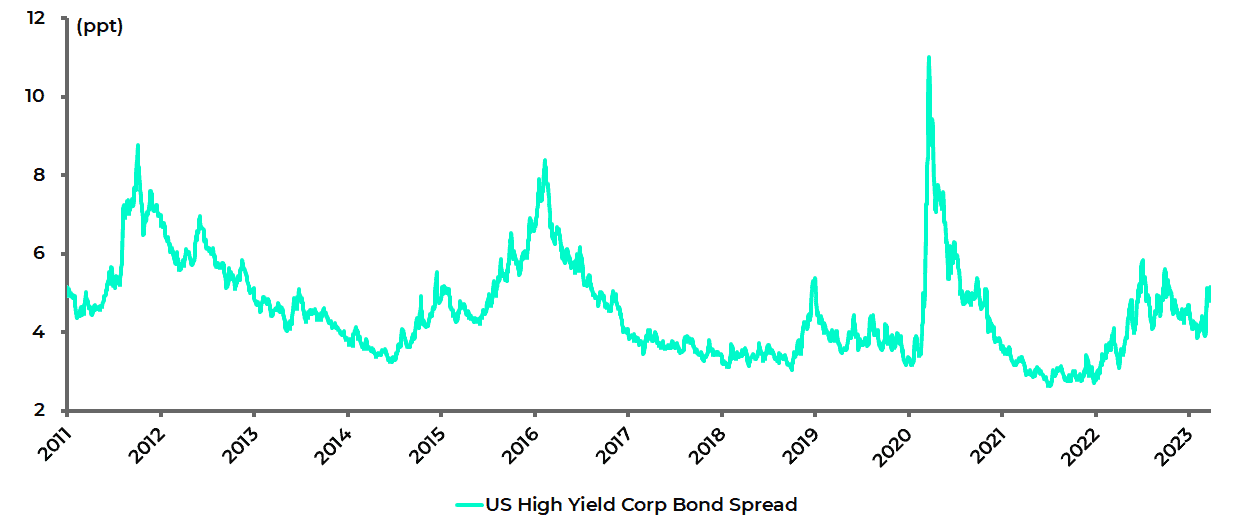

It remains remarkable how little US corporate bond spreads have risen so far in this monetary tightening cycle despite 475bp of Fed rate hikes since March last year.

The US high-yield corporate bond spread rose from 271bp in late December 2021 to a recent high of 583bp in July 2022 and is now 516bp, though up from 389bp in early March.

US high-yield corporate bond yield spread

Source: Bloomberg

This is despite growing recession talk stemming from rising fears that banks tighten lending standards following the ripple effects from the failure of Silicon Valley Bank.

The main reason for the lack, for now, of more evidence of creditor stress is that a large number of American companies “termed out” their debt in recent years, thereby taking advantage of then much lower bond yields to lock in financing costs, with an average US$455bn a year of high-yield bond issuance in 2020 and 2021.

US high-yield corporate bond issuance

Source: SIFMA

If this is one positive for the high-yield market, another is the improved credit rating quality compared with 2007 and the financial crisis.

Double-B rated companies are now around 50% of the market compared with 35% in 2007, while Triple-C represents only 10% compared with 20% in 2007.

The other point is that yields are now more important than spreads in the sense that the nominal yields have become much more attractive.

It is possible, for example, to earn 7.1% on two-year Double-B paper.

That is an attractive return with limited risk, just as 4.6% on a government guaranteed money market fund is a compelling return relative to bank deposits yielding on average 1.5%.

This is why, in the wake of the catalyst provided by Silicon Valley Bank, there is now growing focus among investors on the issue of money market funds attracting liquidity out of bank deposits.

US bank deposits have already declined by US$655bn or 3.6% as of 15 March since peaking in mid-April 2022. By contrast, assets in MMFs have risen by US$663bn or 14.8% since late April 2022 as of 22 March, according to the Investment Company Institute.

US bank deposits and money market funds’ assets

Note: Bank deposits data up to the week ended 15 March. MMF data up to the week ended 22 March.

Source: Federal Reserve, Investment Company Institute (ICI), Bloomberg

Are Private Loans the Canary in the Coalmine?

Meanwhile, returning to the high-yield market, it may well be that the real damage in this cycle in the credit markets should the US recession unfold, as is the base case here, will turn out to be in the private loan market rather than in the bond market.

In this respect, as previously discussed here (“Are Leveraged Loans This Cycle’s Ticking Time Bomb?”, 27 July 2022), leveraged loans have been the major funding source of the booming area of private equity in this cycle.

US leveraged loans outstanding have risen by US$933bn or 188% from US$497bn at the end of 2010 to US$1.43tn at the end of 3Q22.

US leveraged loans outstanding

Source: Federal Reserve – Financial Stability Report; S&P Global, Leveraged Commentary & Data

These leverage loans are linked to the interbank rate which is now 5.1% on 3-month Libor, up from 0.11% in September 2021.

Apparently, the vast majority of borrowers have not hedged against interest rate risk. The current yield on leverage loans is 9.7%.

US leveraged loans average yield and 3-month Libor

Source: Bloomberg

The Private Loan Market is Dangerously Murky

Staying on the subject of private loans, and the whole expansion of what might be termed shadow finance, there was an interested article in the Wall Street Journal in late January on the rising exposure of North American pension funds to private credit (see WSJ article: “Pension Investments in Private Credit Hit a High”, 30 January 2023).

The average exposure of public pension funds to illiquid, often unrated debt is 3.8%, according to this article, with investors lending out an estimated US$200bn in private credit last year with the size of the total market estimated at more than US$1tn outstanding.

The above article is testimony to an important point.

That is the more this writer learns about the shadow banking area in America, the explosion of which is the consequence of the heavy regulation of the commercial banks following the 2008 financial crisis, the more it becomes clear how little is known about it, a failing doubtless shared by many market participants and, quite possibly also, by banking regulators and the Federal Reserve.

Emerging Markets are Suprisingly Calm

Meanwhile another unusual feature of the current Fed tightening cycle is that many traditionally vulnerable emerging markets have not had to raise rates more than the Fed, or in some cases less.

Indonesia is the best example in Asia with Bank Indonesia having raised its 7-day reverse repo rate by 225bp so far in this tightening cycle from 3.5% to 5.75%, compared with the Fed’s 475bp of rate hikes.

Bank Indonesia policy rate and Fed funds rate

Source: Bank Indonesia, Federal Reserve

It is also the case that the Indonesian central bank has gone on hold at its last two monthly meetings suggesting its monetary tightening cycle is over.

The historically extremely highly volatile Indonesian currency, the rupiah, has also remained remarkably stable declining by only 6.1% against the US dollar since the start of last year and up 2.6% year-to-date.

Rupiah/US$ (inverted scale)

Source: Bloomberg

This is a reminder that monetary and fiscal policies remain much more orthodox in many emerging markets relative to the G7 world while inflation in many of these countries remains much less of a problem because demand was not artificially stimulated during the pandemic by paying people to do nothing

.