Are Emergency Rate Cuts Coming?

How Bad Is It?

Author: Chris Wood

The US employment data has remained critical for the many hoping for a resumption of Fed easing, be it owners of gold or private equity titans.

In this respect, financial markets will continue to react, first and foremost, to the headline payroll number, as they did on Friday with the data finally showing weakness triggering a big pickup in Fed easing expectations.

Money markets are now discounting 119bp of easing by the end of this year whereas before the payroll data it was only 86bp.

An intra-meeting cut, the first since March 2020, is now in the cards.

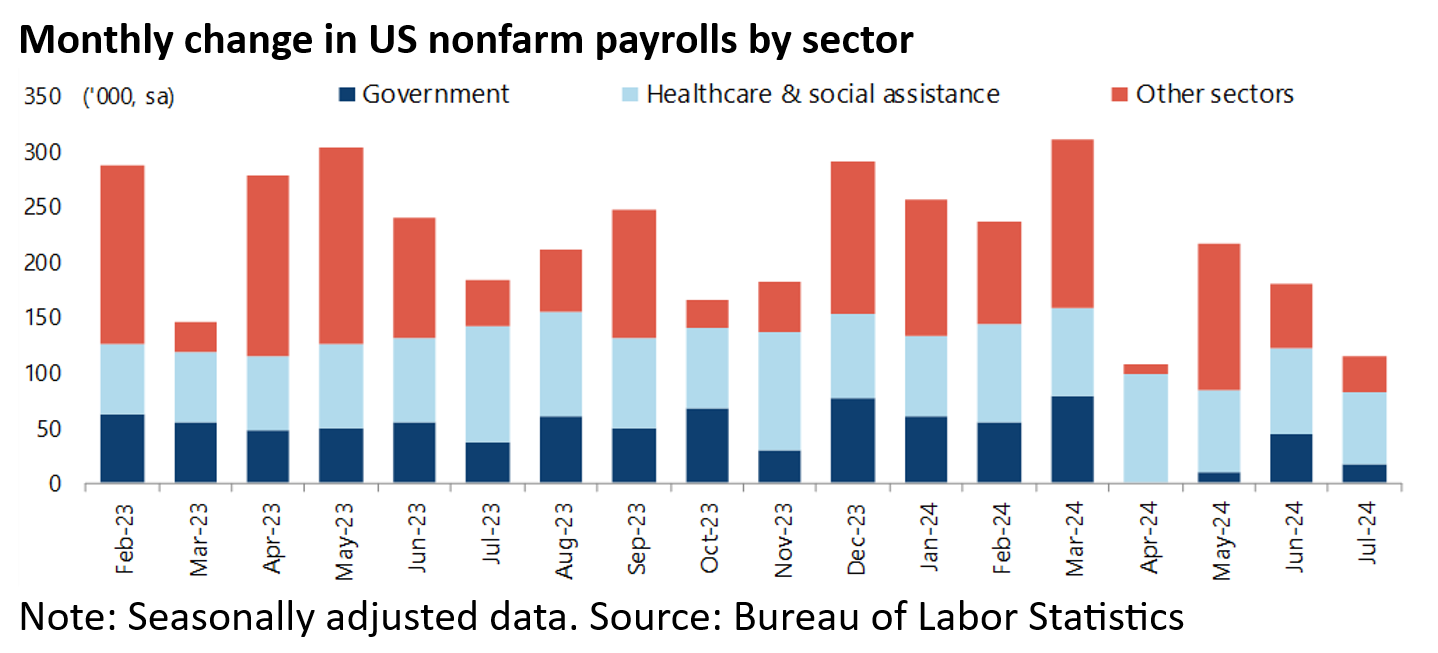

As for the payroll report itself, the headline increase of only 114,000 in July was the second lowest, after the 108,000 increase in April, since December 2020 when nonfarm payrolls declined by 243,000.

While the government and healthcare and social assistance sectors increased by 81,000 in July which means they accounted for a large 71% of the increase in payrolls.

Birth-Death Adjustment is Making Employment Look Stronger Than it Actually Is

Meanwhile, given the importance attached to the payroll data point, it is worth recording the rather bizarre methodology that goes into calculating this widely followed indicator of the labour market.

It is also worth noting again the different message sent by alternative data.

There are two statistical issues in the Bureau of Labor Statistics’ (BLS) job data which are worth highlighting, given the current importance attached to the employment data as regards the direction of US monetary policy.

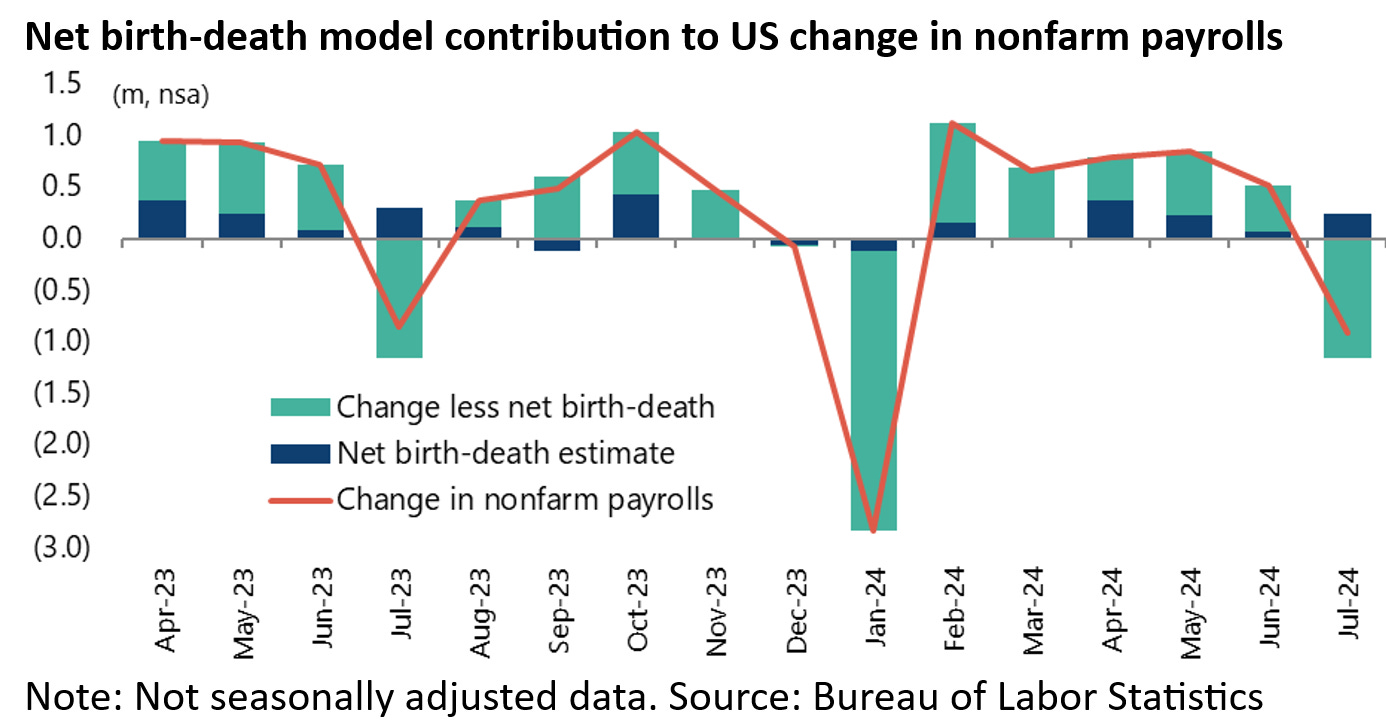

First, there is the methodology that goes into compiling the establishment survey’s nonfarm payrolls data, namely the so-called “net birth-death” adjustment.

This is used to estimate the net effect of job gains from business openings (births) and job losses due to business closings (deaths).

It also should be noted that the net job gains/losses from the net birth-death model is measured only on a non-seasonally adjusted basis and therefore it should be compared with the non-adjusted nonfarm payrolls data.

The state of play at present is that the net birth-death model has added 1.276m of jobs to the nonfarm payrolls in the past 12 months to July, accounting for 52% of the total increase in nonfarm payrolls of 2.464m on a non-seasonally adjusted basis.

Excluding the jobs derived from the net birth-death model, US nonfarm payrolls have increased by only 1.188m or 99,000 per month over the past 12 months.

This raises the important issue of how the net-birth death model is actually calculated.

The answer is that it is a model based on lagged historic data on business formations but that the process is too complicated to go into detail here.

Still the model is probably using data based on the 2021-22 pace of small business creation which, given the subsequent rise in interest rates, is probably not appropriate.

Household Survey vs Nonfarm Payrolls

The second issue worth noting is that the number of nonfarm payrolls includes multiple jobholders.

On that point, the one difference between the establishment survey of nonfarm payrolls and the household survey of employment is that if a person has three jobs it will count as three in the payroll data but only as one in the household survey.

The establishment survey is counting the number of paid jobs in America while the household survey measures the number of employed workers, including self-employed and unpaid family workers.

That means multiple jobholders are counted as one employed person in the household survey.

As a result, the job growth is much lower by this measure.

Indeed there has barely been any growth at all.

Household survey employment increased by only 57,000 or 0.04% on a YoY basis in July, the lowest rate of growth since August 2010 if the Covid-impacted period of 2020-2021 is excluded.

By contrast, nonfarm payrolls still rose by 1.6% YoY in July.

US Consumer Has Been Hurting For a While

Staying in America, it is also worth noting from the doveish standpoint that real retail sales growth remains negative.

US real retail sales, excluding food services, declined by 1.0% YoY in June.

Indeed, this data point has been in a declining trend since September 2022 save for December 2023.

Meanwhile, the University of Michigan consumer sentiment index declined by 1.8 points from 68.2 in June to an eight-month low of 66.4 in July.

This came after 11.2 points of decline in the previous three months from a recent high of 79.4 in March, though it is still well above the low of 50.0 reached in June 2022.