America's Financial Dominance is Ending, What Comes Next?

Author: Chris Wood

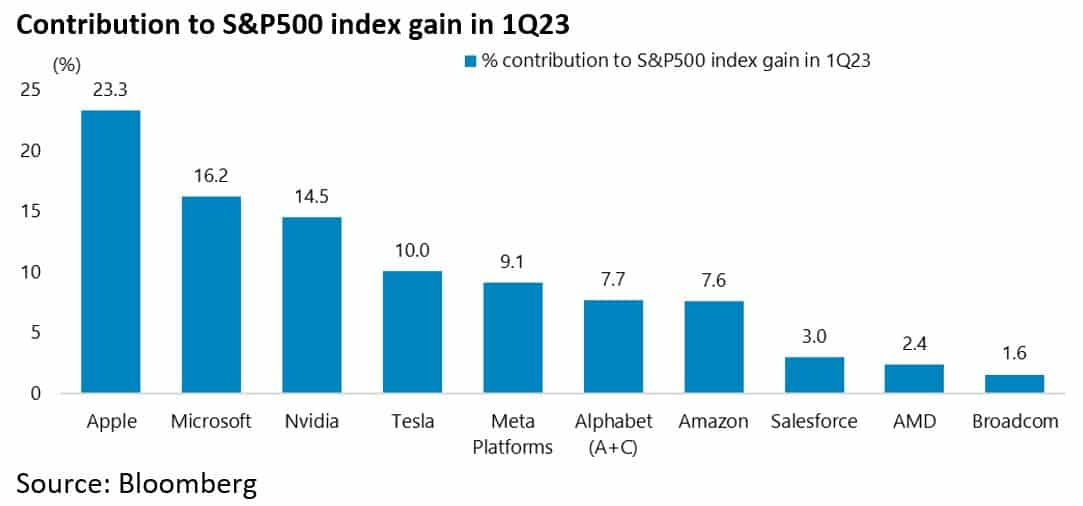

The most amazing statistic this writer has read about the concentrated nature of the first quarter’s US stock market rally is that three stocks, Apple, Nvidia and Microsoft, contributed to 54% of the gains in the S&P500.

And the top 10 stocks accounted for more than 95% of the gain.

Meanwhile if last quarter’s reversion trade was out of energy and into tech (i.e. the precise opposite of what worked in 2022), this writer has not given up completely on energy.

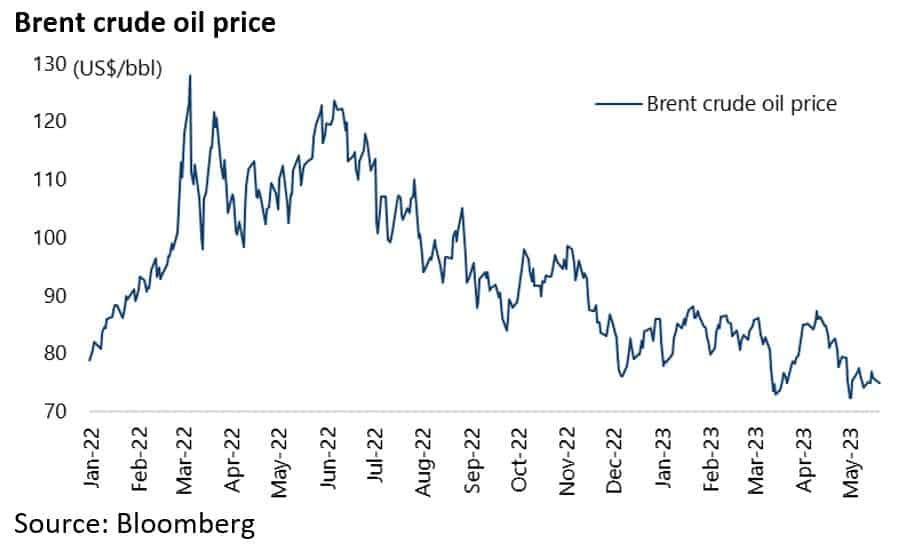

Financial markets were certainly reminded of the energy trade with the OPEC decision on 2 April to reduce supply by 1.16m barrels/day resulting in a 6.5% increase in the Brent crude oil price on the following day to US$84.9/bbl.

This is another reminder of the tight nature of the oil market in terms of supply, despite continuing US recession fears, which has caused oil to correct again since.

Perhaps more interestingly, however, it is also another reminder that the US-Saudi relationship is not what it was.

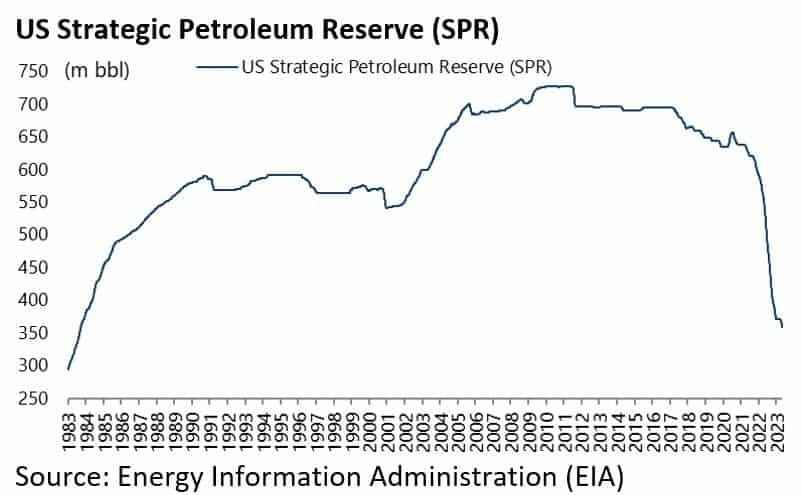

Will President Joe Biden be tempted to launch another raid on America’s Strategic Petroleum Reserve (SPR)?

He has already reduced it by 234.1m barrels since the start of last year from 593.7m barrels to 359.6m barrels on 12 May and was meant to start buying back oil last December.

On this point, the US Department of Energy announced on 15 May that it will purchase 3m barrels of crude oil for the Strategic Petroleum Reserve for delivery in August.

China and Saudi Oil Deal in Focus

Meanwhile there has continued to be much conjecture on exactly what was agreed between Saudi Arabia and China in terms of China paying for Saudi oil in renminbi when Saudi Crown Prince Mohammed Bin Salman (MBS) laid out the red carpet for President Xi Jinping during his three-day visit to Riyadh back in December.

On this point, Xi said last December at the China-Gulf Cooperation Council (GCC) Summit in Riyadh that China and Gulf nations should make full use of the Shanghai Petroleum and National Gas Exchange as a platform to carry out renminbi settlement of oil and gas.

Clearly, it makes no sense for either side to be too specific for fear of gratuitously provoking Washington.

But the days of the petrodollar surely look numbered.

This writer heard one interesting rumour when in China recently that Saudi was using the renminbi it was receiving for oil to buy gold on the Shanghai Exchange.

It is difficult to confirm this but it is certainly interesting that such stories are circulating.

On this point, it should be remembered that China launched in 2018 renminbi-denominated crude oil futures contracts on the Shanghai International Energy Exchange, and the renminbi has been fully convertible into gold on exchanges in Shanghai and Hong Kong since 2017.

Is Japan Ignoring Russian Oil Price Caps?

Meanwhile another development worth noting is a Wall Street Journal article last month reporting that Japan is buying Russian oil at prices above the arbitrary cap of US$60/barrel set by the G7, the EU and Australia back in early December (see WSJ article: “Japan Breaches Oil-Price Cap”, 3 April 2023).

Japan is meant to be a fully signed up member to the Western alliance against Ukraine.

But in reality its approach has been much more nuanced.

For example, European energy companies exited their investments in Russia without compensation on the outbreak of the Ukraine conflict whereas Japanese companies have not exited the Sakhalin projects.

Japan last year obtained an exemption to the price cap through 30 September for oil purchased from the Sakhalin-2 project in Russia’s Far East.

While ExxonMobil and Shell both relinquished their stakes in the Sakhalin projects, Mitsui Corp and Mitsubishi Corp still own a combined 22.5% stake in the Sakhalin-2 project.

Russia accounts for nearly one-tenth of Japan’s natural gas imports, mostly from Sahkalin-2.

It is also worth mentioning that the past quarter has also seen growing historical efforts by China to assert itself globally and prepare for a world where Washington has, via its move on semiconductors, effectively declared economic war against Beijing as previously discussed here (see The Shadow Semiconductor Wars Explained, 23 November 2022).

Recent notable examples have been China brokering a diplomatic rapprochement between Saudi Arabia and Iran in March, and Xi’s meeting with Russian President Vladimir Putin at the Kremlin in Moscow also in March, a meeting which was followed by Xi’s visits to three African countries to meet their heads of government.

Meanwhile, the foreign ministers of Saudi Arabia and Iran met in Beijing on 6 April for the first formal meeting of the countries’ top diplomats in more than seven years.

First Cracks in the Dollar's Hegemony Emerging

On the related point of the growing use of the renminbi in trade, there have recently been two interesting developments.

First, China’s CNOOC and France’s TotalEnergies finalised in late March the first-ever deal on liquified natural gas (LNG) in China settled in renminbi.

The trade involves about 65,000 tonnes of LNG imported from the United Arab Emirates, marking a further step in Beijing's seeming attempts to undermine the US dollar as the universal "petrodollar" for the oil and gas trade.

Second, Rio de Janeiro-based Chinese bank Banco BOCOM BBM, a subsidiary of China’s Bank of Communications, also announced in late March that it will be linked to China’s cross-border interbank payment system (CIPS), an alternative to SWIFT, to support trade settlements between China and Brazil in renminbi.

The bank will become the first direct participant in the CIPS in South America, while the Brazilian branch of the Industrial and Commercial Bank of China (ICBC) will become the renminbi clearing bank in Brazil.

The announcement came after China and Brazil reportedly reached a deal in February to trade in their own currencies, ditching the US dollar as an intermediary (see Asia Times article: “China and Brazil reach RMB-based trade deal”, 31 March 2023).

The World is Splitting into 2 Spheres of Influence, China & Ameria

In this respect, it is worth emphasising again that the Ukraine conflict has exposed a gaping chasm

between America and Europe’s view of the war and most of the rest of the world which takes a far more nuanced view of the conflict than the good versus evil Manichean narrative coming from Washington, Brussels and London.

The result is growing focus on a move towards a more bipolar world where there will be an American sphere of influence but also a Chinese one, in what might be termed a new world order.

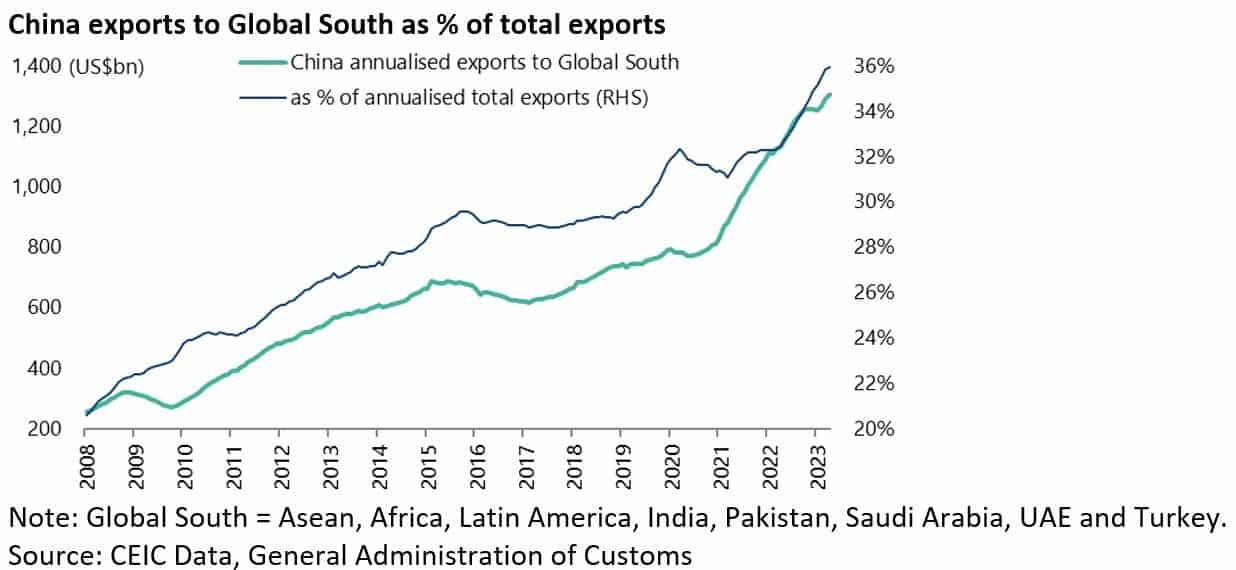

In this respect, China’s exports to the Global South, for want of a better term, now amount to 36% of its annualised total exports, up from 21% at the beginning of 2008.

And a growing proportion of this trade will likely not be transacted in US dollars.

This broad definition of the Global South includes Asean, Latin America, Africa, India, Pakistan, Saudi Arabia, UAE and Turkey.

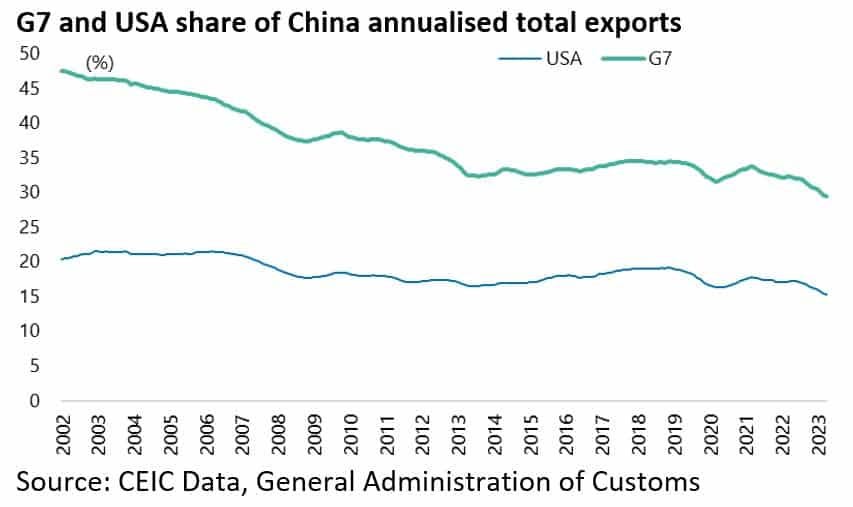

If such looks like the beginning of a new mega trend, it also remains the case that China has a practical stake invested in the status quo given that America still accounts for 15% of its exports and the G7 world for 29%.

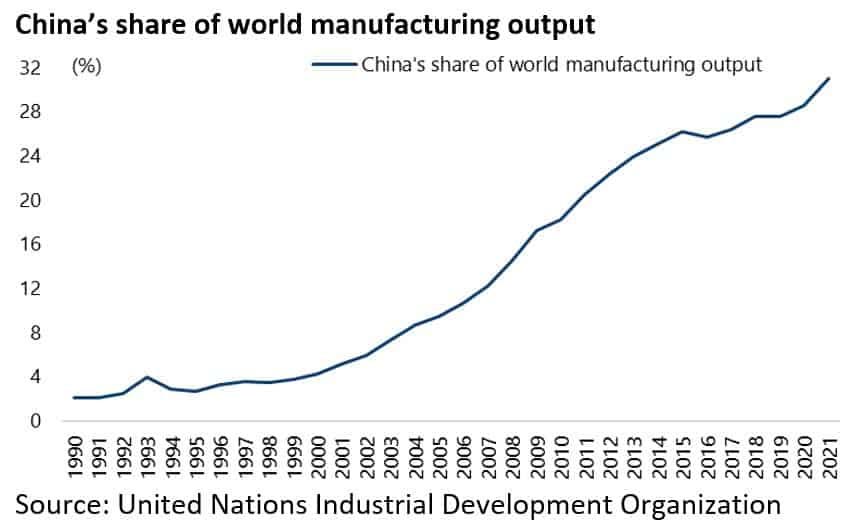

It is also the case that, for all the talk and indeed growing evidence of reshuffling of global supply chains, China still had a dominant 31% share of world manufacturing output as of 2021, the latest data available.

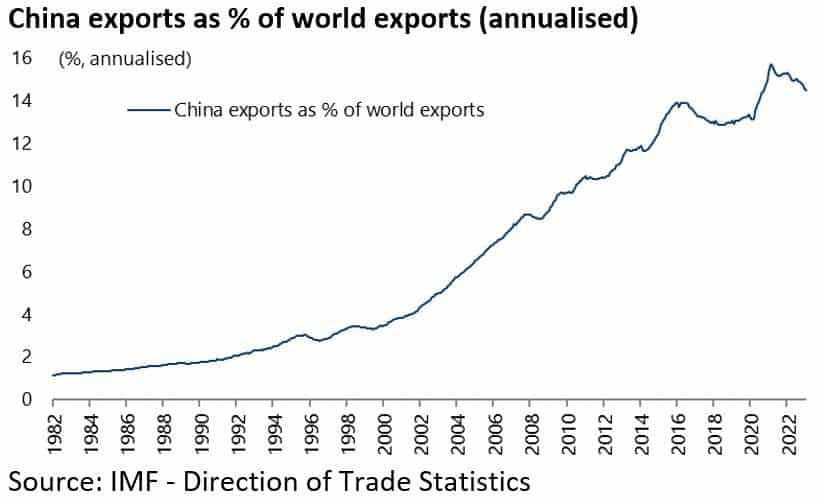

Similarly, China’s exports still accounted for 14.5% of annualised world exports in January, though down from a peak of 15.7% in February 2021.