All the Reasons For and Against a Fed Rate Cut in September

Is a 0.5% cut the right number?

Author: Chris Wood

The hopes for pre-election Federal Reserve easing have increased since the latest employment and inflation data.

If the US nonfarm payroll data for June came in slightly above expectations, up 206,000 compared with the forecast of 190,000, the most interesting point was the downward revision of 111,000 jobs in the previous two months.

This was the biggest downward revision over a two-month period since the 167,000 downward revision for the period of December-January reported in early March.

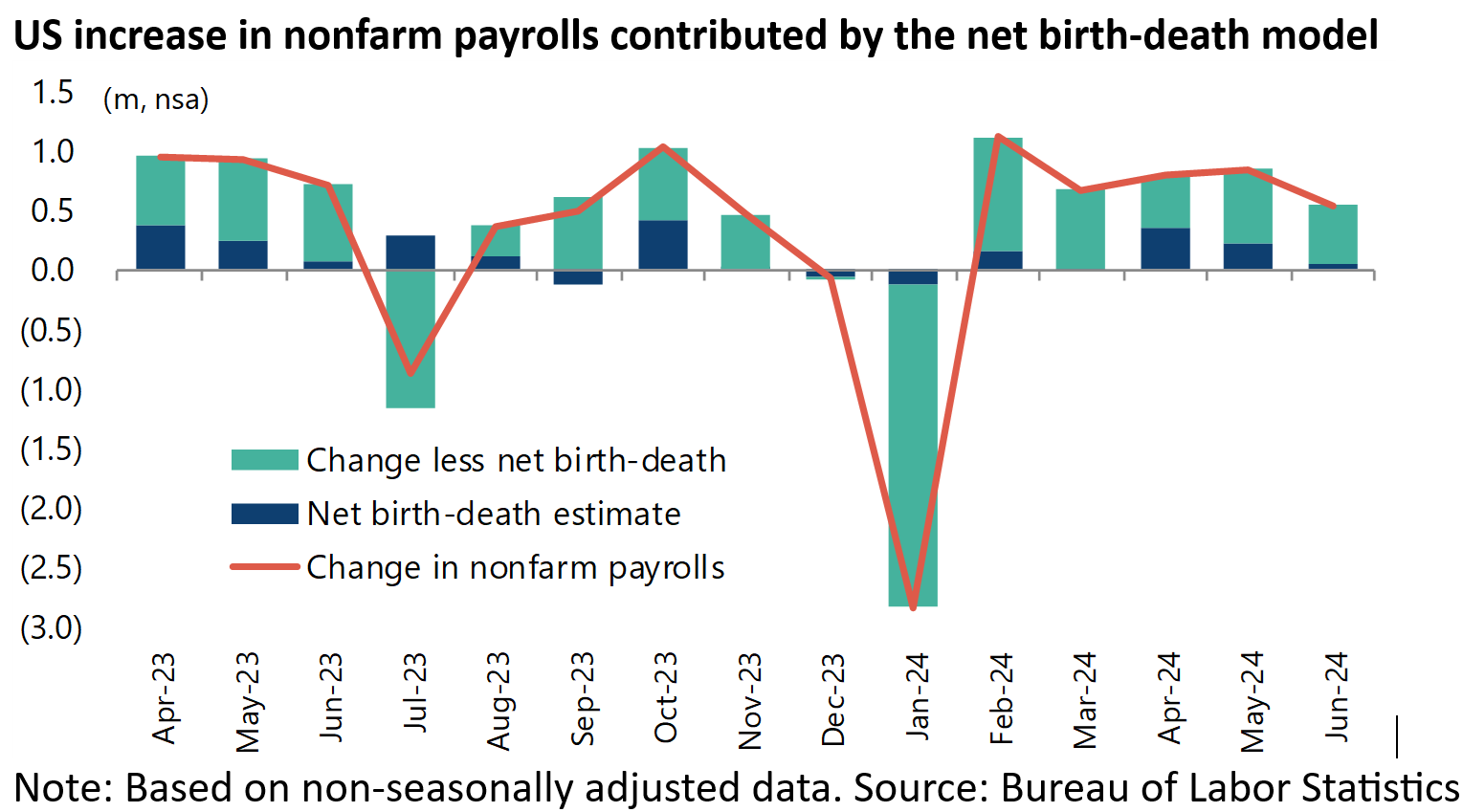

This raises the issue of the methodology that goes into computing the payroll data, most particularly the Bureau of Labor Statistics’ so-called “net birth-death” adjustment.

This is used to estimate the net effect of job gains from business openings (births) and job losses due to business closings (deaths).

The net job gains/losses from the model is measured only on a non-seasonally adjusted basis and therefore it should be compared with the non-adjusted nonfarm payrolls data.

The chart below shows that the net birth/death adjustment has accounted for a significant 52% of the jobs created in the past 12 months.

Thus, the net birth/death model has added 1.325m of jobs to US nonfarm payrolls in the past 12 months to June, compared with the total increase in nonfarm payrolls of 2.55m on a non-seasonally adjusted basis.

The net birth/death model is apparently based on a model measuring small business formation during the 2021-22 period.

It is, therefore, probably exaggerating the current growth in new businesses because this is a period when small business formation boomed.

US average monthly new business applications rose from 293,181 in 2019 to a monthly average of 437,166 in 2021-22 and 457,844 in 2023, though new business applications have since declined by 9% from a recent high of 473,722 in July 2023 to 431,246 in June.

The second issue remains the large number of jobs generated by the government and healthcare sectors, which primarily reflects fiscal easing.

The government and healthcare and social assistance sectors have accounted for 1.647m or 63% of the 2.611m increase in nonfarm payrolls in the past 12 months to June on a seasonally adjusted basis.

They accounted for 152,000 or 74% of the 206,000 job gains in June.

Earnings Growth is Weakening

If the above details signal that the US labour market is not quite as healthy as the headline data suggests, average hourly earnings growth also continues to slow in a way which would please the Fed.

US average hourly earnings growth of private employees decelerated from 4.1% YoY in May to 3.9% YoY in June, compared with a recent high of 5.9% YoY in March 2022.

Small Business Hiring is Paradoxically Picking Up

Meanwhile, the latest NFIB small business survey has shown a re-acceleration in SMEs’ hiring intentions.

This had been the indicator signaling in recent months a weakening of the labour market given its historical correlation with unemployment.

The small business hiring plans index rose from 11% in March to a five-month high of 15% in both May and June, though the unemployment rate rose from 3.8% in March to 4.1% in June.

The above is another example, among many, of how this cycle is different, reflecting probably the peculiar dynamic of the pandemic and the resulting tendency on the part of small businesses to hoard labour.

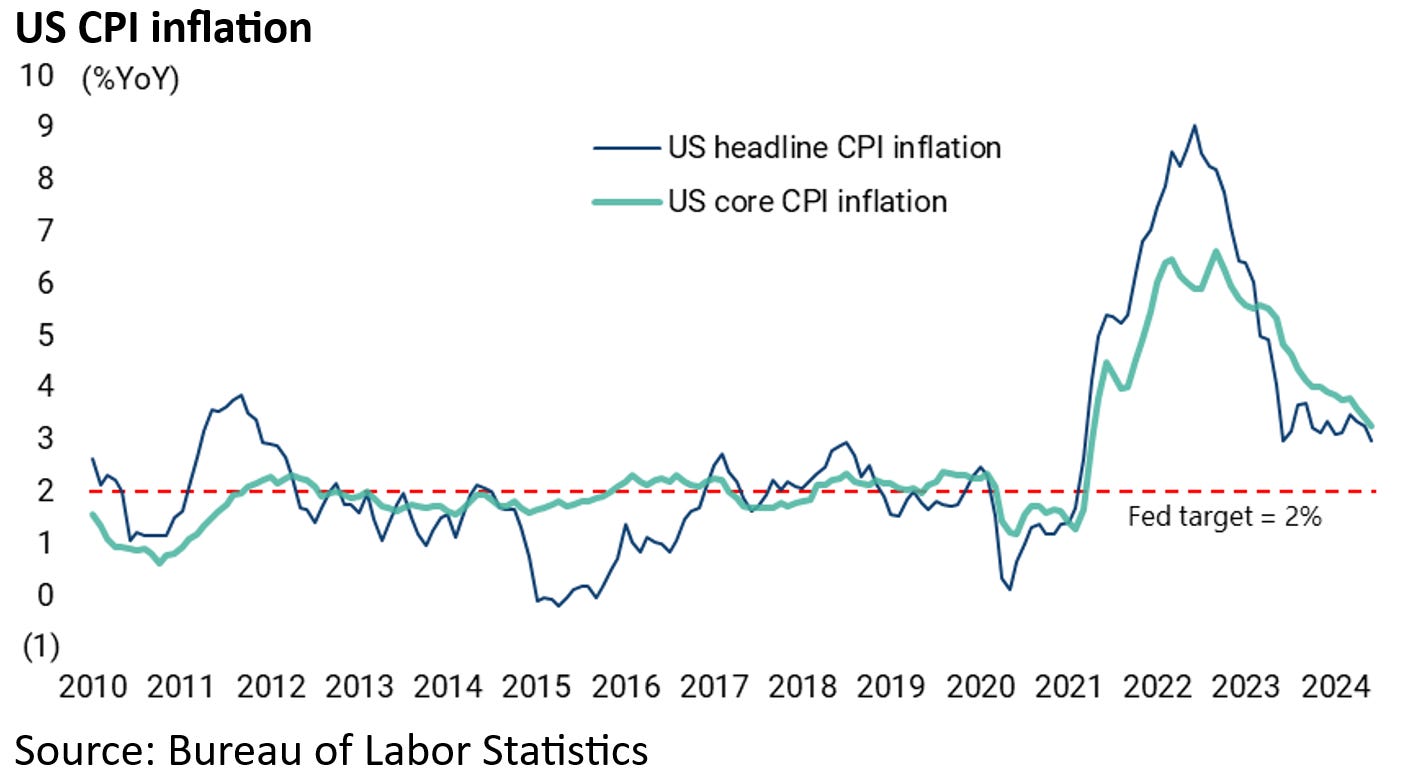

Inflation is Falling but Sticky

Meanwhile, on the inflation front, the June CPI data came out again below expectations.

Headline CPI was down 0.1% MoM and up 3.0% YoY in June, down from a flat MoM and 3.3% YoY rise in May.

This compares with consensus expectations of a positive 0.1% MoM and 3.1% YoY.

This is the first MoM decline in headline CPI since May 2020.

Meanwhile, core CPI rose by 0.1% MoM and 3.3% YoY in June, down from 0.2% MoM and 3.4% YoY in May and below consensus expectations of 0.2% MoM and 3.4% YoY.

Still, services sector inflation remains relatively sticky.

Core services CPI inflation slowed from 5.3% YoY in May to 5.1% YoY in June, while the so-called “supercore” inflation, measured as core services CPI excluding housing, slowed from 4.8% YoY in May to 4.7% YoY in June.

If the data has become more encouraging from the Fed’s standpoint, the net result is that money markets are now expecting 68bp of Fed rate cuts this year, beginning with a cut in September.

The base case here remains that the Fed will still prioritise employment over inflation on any material weakening of the labour market.

This still suggests a fudging of the 2% inflation, which means inflation is likely to end higher in the 3-4% range on a longer-term basis.

An Interesting Alternative Data Set to Measure Inflation

Staying on the inflation issue, this writer was recently made aware while travelling in the American heartland of an interesting alternative data set for measuring inflation in America.

That is the so-called Chapwood Index (chapwoodindex.com).

The index seeks to measure accurate cost-of-living increases experienced by Americans by reporting the unadjusted actual cost and price fluctuations of the top 150 items on which people spend their after-tax income in the 50 largest cities.

The index is updated and released twice a year.

The index shows, unsurprisingly, that the true cost of living increase is far greater than the official CPI data indicates.

For example, the latest data shows that the true cost of living increase in 2023 in the 50 cities ranged from 7.8% to 13.6%, though down from a peak of 11.3%-18.8% reached in 2H21-1H22.

The above helps explain why inflation remains a real issue in the upcoming presidential election which is due to be held on 5 November.

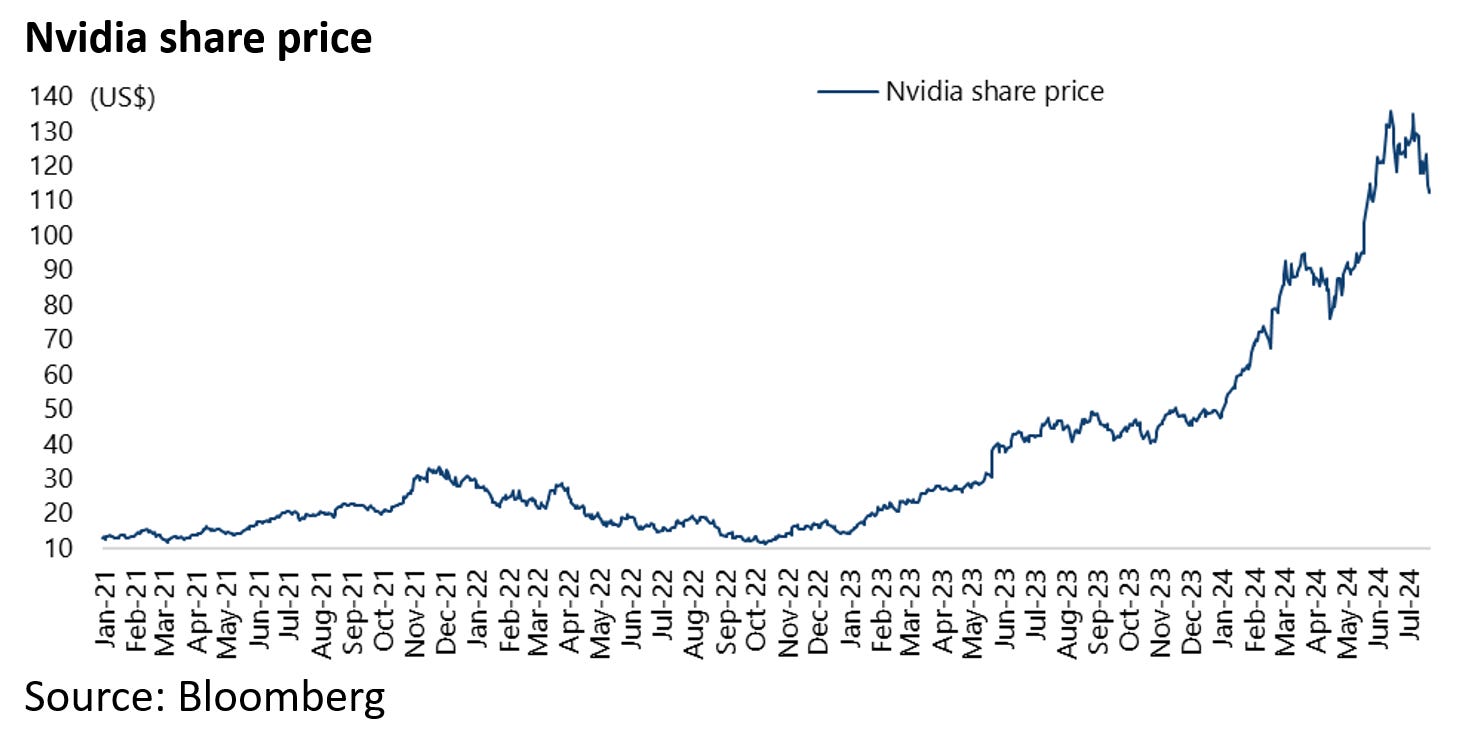

Betting Against Nvidia is Never a Good Idea

Back to the markets, it remains the case, while violent corrections can happen at any time and the company’s share price is down 20% from its 2024 high, that Nvidia is still making most of the profits out of the current arms race to build AI infrastructure.

Nvidia’s gross profit margins last quarter were reported at an enormous 78.4%, up from 64.6% a year ago.

True, there is much market focus on how long Nvidia can maintain its lead.

Still, it is not as if Nvidia is standing still, having unveiled its new next-generation Rubin AI chip platform at the Taiwan tech expo COMPUTEX in early June, which will be rolled out in 2026.

As a tech investor pointed out to this writer recently, questioning Nvidia’s leadership in this space is like asking who is going to overturn Microsoft’s operating system.

In this respect, it is worth highlighting again that Nvidia’s arguably unassailable position is based on its proprietary CUDA software as well as hardware.

It remains the case that Microsoft’s purchase of OpenAI was the most important development in world stock markets last year since it gave the world’s biggest sector in the world’s biggest market, namely the US tech sector, a new story.

The result has been a race to ramp up machine learning capacity and a race to introduce AI features on devices, a phenomenon known as “edge AI”, resulting in hopes of a smart phone replacement cycle.

Whether all this investment will prove monetizable remains completely unclear to this writer.

But the AI investment cycle is undoubtedly happening with Nvidia, so far the main beneficiary.