2025 Will Be the Year of Memory, Not GPUs

Author: Chris Wood

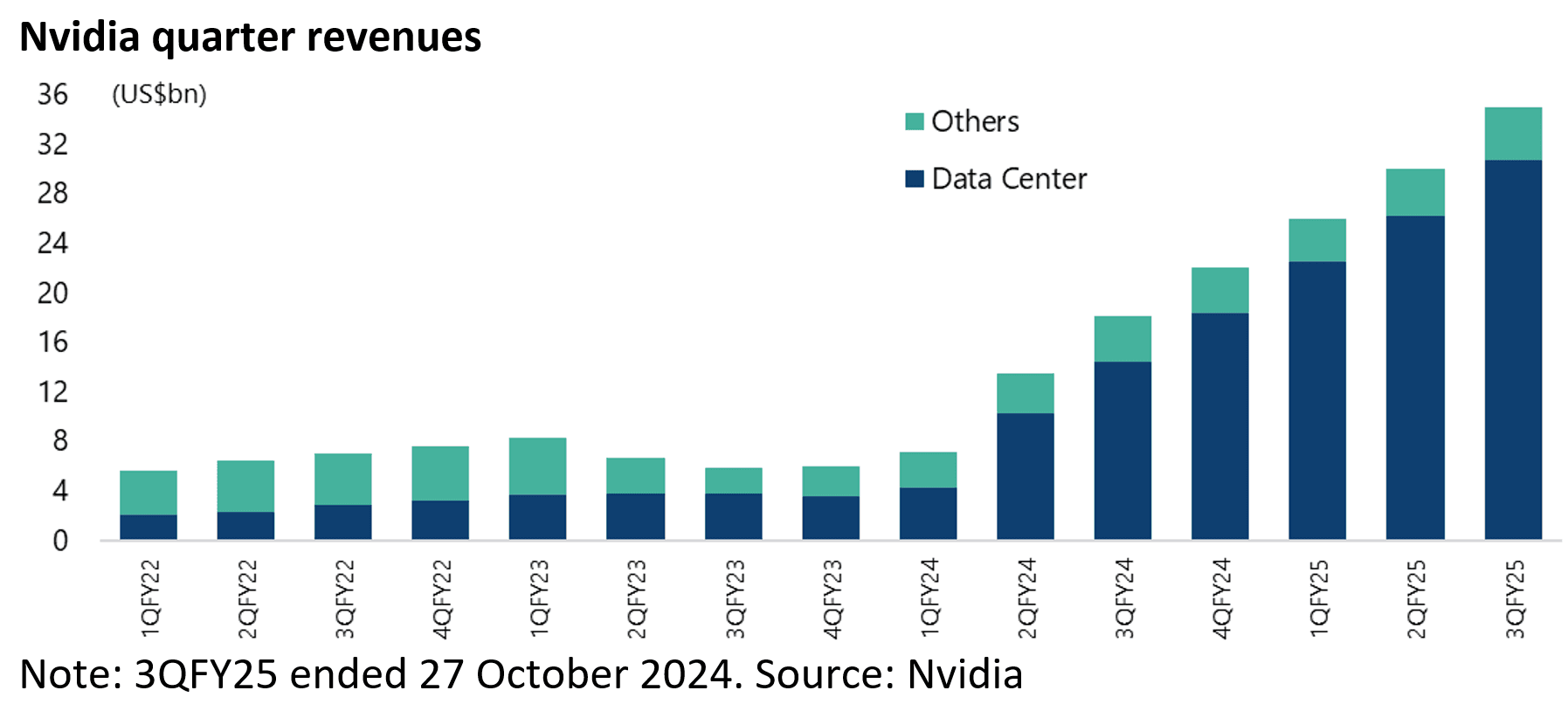

To state the obvious, the AI story has been the key driver of the US stock market since the thematic was crystalized by the announcement of the Microsoft investment in ChatGPT-maker OpenAI in January 2023; since then the market capitalisation of Nvidia has risen from US$472bn to US$3.29tn.

Quarterly revenues have risen from US$6bn to US$35bn.

This writer was in Taiwan recently and there is no doubt from local soundings that the AI capex-driven arms race to build machine learning capacity is expected to continue throughout 2025.

While the hyperscalers are spending a lot of money on such capex, an estimated US$200bn this year, the view in Taipei is that they have to keep investing or otherwise risk being left behind.

Meanwhile, the DPP government in Taiwan, traditionally an anti-nuclear power political party, is in the process of doing a U-turn on nuclear power given the surging power requirements of TSMC in the AI era.

All this is positive for TSMC which has a more than 90% market share in advanced semiconductors given the practical problems being experienced by both Intel and Samsung Electronics in their foundry businesses in terms of execution or the lack of it.

Indeed, these two companies delaying orders for chipmaking equipment was the main reason behind semiconductor equipment manufacturing company ASML’s shockingly negative earnings report earlier this quarter.

This means TSMC remains well positioned though there are some concerns in Taiwan prompted by comments made by Donald Trump in a Joe Rogan Experience podcast on 25 October where the now President-elect criticised the Biden administration’s CHIPS and Science Act and said that tariffs should be imposed on chips from Taiwan.

On this point, TSMC is due to receive US$6.6bn in grants from the US Commerce Department for building its first American fab in Phoenix, Arizona.

It is now operational with volumes expected to ramp up next year.

TSMC’s current plan is to build two more fabs in America and a total of three in Japan, of which one is now up and running in Kumamoto, Kyushu.

Together with a planned fab in Dresden, Germany, which broke ground in August, the aim is that 15-20% of TSMC’s production will be overseas by 2030.

Still the difference between the US fabs and the Japan and European ones are that the latter are joint ventures where the costs are shared.

Whereas in America there is no joint venture partner but subsidies are offered.

This is why any changes in the CHIPS Act by a Trump administration, or even an outright abolition of it, could change the calculus for TSMC.

Still, the fact that TSMC has already agreed to move production to America should help defuse criticism from a Trump administration since this is one of Trump’s major points of focus.

There is also the practical matter that no other company has the ability to operate at scale in the most advanced node, currently 3-nanometer (3nm) with 2nm process nodes due to be launched in 2025.

Meanwhile, the estimate is that AI accounts for about 20% of TSMC revenues and is currently the company’s only high growth area.

The rest of the tech hardware universe, be it personal computers, smartphones or general-purpose processors, is expected to grow by 5% at most in the coming year due to a continuing fundamental lack of replacement demand.

2025 Could be the Year of Memory, Not GPUs

Meanwhile, the AI story has very much returned to its original driver, namely the demand for Nvidia’s High-Bandwidth Memory (HBM) based chips to drive machine learning capacity in AI data centres.

Whereas the excitement a year ago about so-called Edge AI, in terms of AI being embedded in consumer devices, has cooled somewhat.

There is a general sense that this will take longer to develop and that the first achievements of AI, in terms of productivity gains delivered by the technology, will be in the corporate space.

Still, one interesting nugget is that the word in Taiwan is that the ultimate AI device for consumers is unlikely to be a PC or a smartphone but rather a pair of glasses.

On this point, Meta has already introduced one prototype in September but it is very much at the very beginning with the weight 100 grams, heavier than the apparently required 80 grams.

Anyway, this is supposedly what everybody is now working on.

Taiwan Owned Production Rapidly Leaving China

Meanwhile, Taiwanese companies are moving production from mainland China to Southeast Asia at an accelerating pace, as can be seen in the chart below.

Indeed, Taiwan companies invested more in Southeast Asia than in China in 2023 for the first time since 1992.

Taiwan’s outward investment to mainland China declined from US$5.05bn in 2022 to US$3.04bn in 2023 and US$3.42bn in the first 10 months of 2024.

By contrast, outbound investment to Asean rose from US$4.73bn in 2022 to US$5.23bn in 2023 and US$7.97bn in January-October 2024.

If Donald Trump has been focused in his public comments on Taiwan on TSMC and defence spending – he has called for Taiwan to increase its defense spending from the current 2.5% of GDP to 10% of GDP! – he has ignored what has long been to this writer the most legitimate criticism of Taiwan in the global context.

That is its long track record as the supreme mercantilist in Asia where its currency has remained remarkably cheap relative to the scale of its current account surplus.

Thus, Taiwan’s real effective exchange rate has declined by 27% since the start of 1994 while its annualised current account surplus was running at 14.4% of GDP in 3Q24.

This reflects the highly conservative central bank’s longstanding desire to protect traditional industries such as textiles as opposed to the likes of a TSMC.

That is reflected in the relative cheapness of goods and services in Taiwan, if not in the real estate where the wealth generated by the tech sector has had a noticeable impact.

Still if Taiwan is cheap, TSMC is finding its fabs in Japan even more cost effective with engineers costing less than in Taiwan thanks to the weak yen.

China is Acquiring NVDA GPUs One Way or Another

Returning to the subject of America’s continuing attempts to control China’s access to advanced semiconductors, the word in Taipei is that China has been accumulating Nvidia’s chips through the secondhand market.

The estimate in Taiwan is that 350,000 Nvidia HBM-based chips have been smuggled to China this year which is about 10% of Nvidia’s estimated HBM-based GPU production of 3.5-3.8m.

If this is not the ideal way to get the technology from Beijing’s perspective, it is certainly better than nothing.

Meanwhile, TSMC is now having, like a bank, to do KYC on its customers.

Thus, it recently suspended shipment to a China-based chip designer after a chip it made for the company was found on a Huawei artificial intelligence (AI) processor (see Taipei Times article: “TSMC suspends orders to Sophgo”, 28 October 2024).

Opening for a Populist Candidate in Japan

Meanwhile if the yen is cheap, the failure of Japan’s LDP and its longstanding coalition partner Komeito to secure a parliamentary majority in the election held on 27 October is the latest sign that ordinary Japanese people are not happy with the consequences of years of highly unorthodox Japanese monetary policy and related asset price inflation while their US dollar purchasing power has collapsed.

Indeed, this writer would go so far as to say that the situation is ripe for a populist to exploit even though there is no sign as yet of a populist emerging.

Rather the Japanese voters have voted against the government as opposed to any specific opposition party or policy agenda.

Still the reality is that the main beneficiary of ultra easy monetary policy in Japan since the launch of Abenomics in late 2012 has been owners of Japanese equities, most particularly those who also hedged the currency, and owners of hard assets like property.

The chart below shows the big rise in Tokyo apartment prices since late 2012.

If that is the upside, many years of quanto easing has not been so good for ordinary Japanese people, particularly those who do not own properties or equities – foreign ownership of Japanese stocks has risen from 4% to 32% since the bursting of the Bubble in 1990.

Indeed, the Japanese have seen their dollar purchasing power collapse.

Japan’s GDP per capita has declined from US$49,175 to US$33,899 since Haruhiko Kuroda’s appointment as BoJ Governor in March 2013.

Still the cost of Japanese labour, as a result, remains incredibly competitive in US dollar terms.

Average monthly scheduled earnings for full-time employees have declined from US$3,934 in January 2012 to US$2,242 in October 2024.

Japan Will Likely See a CAPEX Boom Due to Cheap Labor

If this is the case, it explains why Japan is much more likely to have a capex cycle, based on production being relocated back to Japan, than it is to have a consumption boom.

Indeed, the only consumption boom is in tourism where inbound tourist flows continue to surge while fewer and fewer Japanese can afford to go offshore, a situation which is again likely to fuel grievances that could be exploited by populist rhetoric.

Visitor arrivals have risen by 52% YoY to 30.2m in the first 10 month of this year.

By contrast, Japanese resident departures have totaled only 10.6m in the first 10 months of 2024, remaining 36% below the pre-Covid level of 16.7m in the first 10 months of 2019.